Fourth Quarter Update 2021

VANCOUVER, British Columbia, Jan. 19, 2022 (GLOBE NEWSWIRE) -- Macarthur Minerals Limited (TSXV: MMS) (ASX: MIO) (OTCQB: MMSDF) (the Company or Macarthur) is pleased to update shareholders on activities during the fourth quarter of 2021. Q4 2021 was very active in which the Company continued to focus on the delivery of the Feasibility Study for its high-grade magnetite Lake Giles Iron Project in Western Australia. The heavy lifting undertaken in Q4 2021 now sets Macarthur up for an exciting start to 2022.

2021 Fourth Quarter Highlights

Key highlights during the fourth quarter of 2021 included announcements on the following:

Highlights

|

Key Areas of Focus for the 2022 Calendar Year

Macarthur’s primary areas of focus during 2022 will include the following:

- Lake Giles Iron Project

- Feasibility Study: Finalising the Mineral Reserves Statement for the Lake Giles Iron Project in February and release of the Feasibility Study within 45 days after delivery of the Mineral Reserves Statement.

- Project Financing: Advancing project financing for the development of the Lake Giles Iron Project post-delivery of the Feasibility Study.

- Project Schedule: Advancing environmental approvals, contracts and pre-development deliverables to ensure that achievement of first iron ore shipment remains on track with the project schedule defined by the Feasibility Study.

- Feasibility Study: Finalising the Mineral Reserves Statement for the Lake Giles Iron Project in February and release of the Feasibility Study within 45 days after delivery of the Mineral Reserves Statement.

- Ularring Hematite Project

- Undertaking a programme of work to ensure that required approvals, mine planning and transport solutions are in place to enable a short run-up to commencement of DSO mining operations at the Snark and Drabble Downs deposits, subject to the iron ore price environment supporting the commencement of commercial DSO mining operations.

- Undertaking a programme of work to ensure that required approvals, mine planning and transport solutions are in place to enable a short run-up to commencement of DSO mining operations at the Snark and Drabble Downs deposits, subject to the iron ore price environment supporting the commencement of commercial DSO mining operations.

2022 Calendar Year Goals (In Detail)

Macarthur remains well placed to deliver on its 2022 goals. A more detailed summary of these goals is set out below:

- Lake Giles Iron Project:

- The Feasibility Study for the Lake Giles Iron Project is now in its final stages and is on track for delivery in accordance with the timetable released to the market on 16 December 2021 (see announcement here). The combined technical capabilities and experience of Stantec, Orelogy and Macarthur’s highly experienced owners’ team will ensure the delivery of the Feasibility Study on time and within budget.

- A large amount of work was undertaken by Macarthur and its study consultants in 2021 to advance the technical aspects of the Feasibility Study. The work undertaken included detailed metallurgical test work, analysis of power requirements, process engineering design and non-process engineering design.

- Process and non-process engineering design has achieved 100% design completion with work now focusing on cost estimation. Additionally, the Company completed a geotechnical drilling programme during Q3 and Q4 2021, which provided critical inputs for the second phase of mine planning. The mine planning work is nearing completion with a Mineral Reserve Statement targeting release to the market in February.

- The final Feasibility Study Report (NI43-101 Technical Report) will be released to the market within 45 days of the delivery of the Mineral Reserve Statement.

- Following delivery of the Feasibility Study, the Company will progress engagement with project financiers, and the balance of 2022 will be focused on project optimisation, securing project financing, identifying strategic partners and advancing the required approvals, contracts and pre-development deliverables to ensure that achievement of the first iron ore shipment remains on track with the project schedule defined by the Feasibility Study.

- The Feasibility Study for the Lake Giles Iron Project is now in its final stages and is on track for delivery in accordance with the timetable released to the market on 16 December 2021 (see announcement here). The combined technical capabilities and experience of Stantec, Orelogy and Macarthur’s highly experienced owners’ team will ensure the delivery of the Feasibility Study on time and within budget.

- Ularring Hematite:

- The Company continues to examine options for an early production opportunity for its Ularring Hematite Project at Lake Giles, subject to a return to a supportive iron ore pricing environment for Macarthur’s DSO product.

- Near-term access to Western Australian ports remained elusive during 2021 as a consequence of increased export demand. Access to road and rail transport (and an increase in overall associated transport costs during the heated commodities hike) was also a limiting factor. However, the Company is confident that these limitations will ease coming into 2022 and 2023.

- To ensure that the Company is well positioned to take advantage of market opportunities, Macarthur will leverage previous studies undertaken on the Ularring Hematite Project that outlined an opportunity for DSO and will continue to advance preparations to achieve an accelerated export opportunity. This will include:

- Advancing project approvals and finalising mine planning requirements for the Snark and Drabble Downs deposits over the course of 2022; and

- Continuing the Company’s strategy to develop the lowest cost, end to end transport logistics solution that can sustain DSO mining operations at Ularring.

- Advancing project approvals and finalising mine planning requirements for the Snark and Drabble Downs deposits over the course of 2022; and

- The Company continues to examine options for an early production opportunity for its Ularring Hematite Project at Lake Giles, subject to a return to a supportive iron ore pricing environment for Macarthur’s DSO product.

- Additional Goals in 2022

The Company’s core focus is the advancement of its Lake Giles Iron Project, however it will also focus on a series of complementary goals during 2022. These include:

- Strategic Partnerships: Formalising strategic partnerships for the key development and infrastructure requirements needed to commercialise the Lake Giles Iron Project remains a key focus for the Company this year and in the lead up to delivery of the Feasibility Study. Macarthur signed a Cooperation Agreement with diversified Singaporean-based conglomerate Jin Sung International Pte Ltd on 15 June 2021 and is in active discussions with a number of other global corporates that have the potential to add capital and technical capabilities to the project.

- Project Financing: With the assistance of its financial advisers, the Company continues to advance terms for financing the development of the Company’s high grade magnetite project at Lake Giles to ensure a smooth pathway to the closing of finance post-delivery of a successful Feasibility Study. The development of the financial model as part of the Feasibility Study will assist this pathway. The Company, together with its financial advisers and its study consultants have been working with FTI Consulting to ensure that this model is robust and sophisticated with built in sensitivities to ensure that it can provide adaptive outputs that will satisfy the requirements of conservative due diligence enquiries.

- Nevada Lithium Assets: The Company continues to examine the potential for strategic partnership(s) that can advance a programme of works to realise an improved value proposition for the Company’s 100% owned lithium brine claims in the Nevada region of the USA. Macarthur holds 210 mining claims in Nevada, covering an area of 7 square miles (18 km2) located in Railroad Valley, in Nye County, Nevada, USA. The claims are located approximately 180 miles (300 km) North of Las Vegas, Nevada, and 330 miles (531 km) south east of Tesla’s Gigafactory.

- Graduation on to main board of TSX: The Company maintains its aspiration to migrate from the TSXV onto the main board of the TSX during the course of 2022.

- Strategic Partnerships: Formalising strategic partnerships for the key development and infrastructure requirements needed to commercialise the Lake Giles Iron Project remains a key focus for the Company this year and in the lead up to delivery of the Feasibility Study. Macarthur signed a Cooperation Agreement with diversified Singaporean-based conglomerate Jin Sung International Pte Ltd on 15 June 2021 and is in active discussions with a number of other global corporates that have the potential to add capital and technical capabilities to the project.

Iron Ore Market Overview – a recent review and the current position

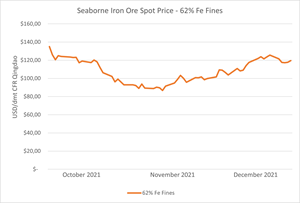

Iron ore prices are driven by demand from China, and over the course of Q4 2021, the views of analysts on the iron ore price outlook for the immediate term have been mixed. However, the sudden bearish views that emerged in Q3 and Q4 2021 seem to have turned equally as quickly.

During Q3 2021, some analysts were predicting sluggish demand would keep prices constrained in the near to medium term and push prices below $US100 a tonne during Q4 2021, however by around mid-December, it became clear that the anticipated collapse in demand during Q4 had not occurred. Whilst demand has been weaker, some analysts consider that China’s plans to ease property curbs and pump further stimulus into its economy could result in increased demand for iron ore.

As at 12 January 2022, the price for 62% iron ore fines CFR Qingdao was USD 131.50/dmt, which is still well above pre-covid levels and up from USD 115.76/dmt as at 1 October 2021. After hitting a low of USD 86.70/dmt on 9 November 2021, the price recovery to January 2022 for 62% fines represents a 51.67% increase in just 2 months. (Source: Custeel).

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/dfb388a0-09b4-4e9e-8ec5-d2b54e23182c

Raw data source: Custeel.net

The continued recovery into mid -January 2022 is an extension to the surge that occurred in the first few days of 2022 after heavy rains appeared to signal a potential disruption to Brazilian supply. At the same time, (on the demand side), traders appear to be observing the spread of the omicron variant in China, specifically within the northern port city of Tianjin. An anticipated easing of steel production controls in China after the Winter Olympics in Beijing next month may have also helped underpin iron ore prices in recent weeks.

Iron Ore Pricing Overview

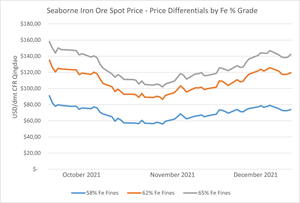

Price differentials between low and high-grade ores have traditionally ebbed and flowed with mill profitability and coking coal prices. However, with China now taking a longer-term and far stricter stance on the environmental impacts of steel production, and with its willingness to impose production curbs on mills, the global iron ore market is arguably entering a phase where a structural trend away from low-grade ores is now developing. Healthy mill profit margins, high cooking coal prices, and seasonal anti-pollution restrictions are creating both a profit incentive, as well as cost and compliance concerns – and the convergence of these factors appears to be motivating steel mills to moderate their consumption of low-grade ores. There is no starker example of this than the forced supply response that occurred in Q3 and Q4 of 2021, with a number of lower grade producers being adversely impacted by the price shift.

As at 12 January 2022, 65% iron ore fines CFR Qingdao, were selling for USD 161.20/dmt, representing a 22.5% premium over the 62% price, and a 93.05% premium to 58% Fe fines CFR Qingdao, demonstrating the widening premium gap for high grade ore. (Source: Custeel).

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/8f7abadc-9a92-45e8-b723-23e6f6192ec6

Raw data source: Custeel.net

On average, approximately two tonnes of carbon dioxide (CO₂) are emitted for every tonne of steel produced. This accounts for roughly 7% of global greenhouse gas emissions. The trend towards higher grade ores demonstrates a change in demand preferences aimed at factoring in the global shift towards decarbonisation. Macarthur’s strategy to meet and help lead the future growth in demand for high grade ore is the right strategy moving into the third decade of this century which will be defined by how industries respond to the challenges of meeting net zero targets.

As outlined by Macarthur in its second quarter update in 2021, the premium for steel products may arguably result in increased direct investment by the rest of the world (excluding China) of new steel production capacity that has the eventual function of replacing older bast furnace steel technology needed by the mid-2030s to meet the strict C02 emissions standards announced in the Paris Accord and by Japan and the USA in 2020.

Completing the journey to net zero emissions in steel production has been demonstrated as technically possible by the use of high-grade magnetite and scrap steel in electric arc furnaces with ‘green hydrogen’ as the reductant. The first green steel production was achieved in Sweden in 2021, with the the only output from that process being H2O.

With Macarthur’s high grade 1.3 billion tonne magnetite resource, it aims to take advantage of the coming structural shift in global iron ore market and help lead Australia’s contribution to a cleaner steel future.

Share Price

Both ASX and TSXV continue to demonstrate reasonably synchronised share price trading patterns for MIO and MMS. Although Macarthur’s share price has pulled back over the fourth quarter, this is not an anomaly that is specific to Macarthur, as it reflects the broader patterns and impacts felt across the entire iron ore industry following the pull-back in global prices during Quarter 3 of 2021. Encouragingly, iron ore prices are still above pre-Covid levels, demonstrating the resilience of a sector that supplies a critical global resource necessary for many facets of human endeavour and advancement.

A summary of MIO/MMS trading activity from October to December 2021 is shown below:

https://www.globenewswire.com/NewsRoom/AttachmentNg/fc57d1c5-4be2-4628-8854-60caedb8a065

Andrew Bruton, Chief Executive Officer of Macarthur Minerals commented:

“The fourth quarter of 2021 was a very active period for the Company as it moves into the final stage of delivery for its Feasibility Study in early 2022.

The fundamental value driver for the Company is its massive 1.3 billion tonne high grade magnetite mineral resources, and Macarthur’s flagship project at Lake Giles will provide significant upside potential for shareholders not only in the near term, but for many decades to come.

The Company has committed to delivering the Mineral Reserves Statement and the final Feasibility Study outputs for the Lake Giles Iron Project to the market in accordance with the timeframes announced in December and has big plans to accelerate into 2022 with a clear strategy to finance the project and bring it out of the ground.

For Macarthur shareholders, the most important takeaway as we enter 2022 is that the structural shift in the global iron ore market towards high-grade iron ore (and magnetite in particular) is well and truly ‘on’. Global policy changes and the realisation amongst producers of lower grade ore that they are vulnerable to pricing movements have already resulted in very visible shifts in the strategic positioning of the Company’s competitors over the last two months.

The market will eventually catch up when it digests the broader significance of those strategic pivots, and when it realises that the value of iron ore companies moving further into the current decade must now be inherently linked to: (1) product grade; and (2) the new normal of net zero.

As the most technically advanced magnetite project in the Yilgarn region of Western Australia at present, and with a high grade, low impurity magnetite product that can contribute to the global shift towards net zero emissions, Macarthur is ideally positioned to take advantage of this shift and help lead Australia’s contribution to a cleaner steel future.

2022 will be an exciting year for the Company as it focuses on core fundamentals and project delivery. I look forward to sharing the Company’s progress with you.”

On behalf of the Board of Directors, Mr Cameron McCall, Chairman

| For more information please contact: | |

| Joe Phillips | |

| Managing Director | |

| +61 7 3221 1796 | |

| communications@macarthurminerals.com | |

| Investor Relations – Australia | Investor Relations - Canada |

| Advisir | Investor Cubed |

| Sarah Lenard, Partner | Neil Simon, CEO |

| sarah.lenard@advisir.com.au | +1 647 258 3310 |

| info@investor3.ca | |

No new information

To the extent that this announcement contains references to prior exploration results and Mineral Resource estimates, which have been cross referenced to previous market announcements (including supporting JORC reporting tables) made by the Company, unless explicitly stated, no new information is contained in accordance with Table 1 checklist in the JORC Code. The Company confirms that it is not aware of any new information or data that materially affects the information included in the relevant market announcements and, in the case of Mineral Resources that all assumptions and technical parameters underpinning the estimates in the relevant market announcement continue to apply and have not materially changed.

Company profile

Macarthur is an iron ore development, gold and lithium exploration company that is focused on bringing to production its Western Australia iron ore projects. The Lake Giles Iron Project mineral resources include the Ularring hematite resource (approved for development) comprising Indicated resources of 54.5 million tonnes at 47.2% Fe and Inferred resources of 26 million tonnes at 45.4% Fe; and the Lake Giles magnetite resource of 53.9 million tonnes (Measured), 218.7 million tonnes (Indicated) and 997 million tonnes (Inferred). The JORC reporting tables and Competent Person statement for the magnetite and hematite mineral resources have previously been disclosed in ASX market announcements dated 12 August 2020 and 5 December 2019. Macarthur has (~23.97 square kilometre tenement area) gold, lithium and copper exploration interests in Pilbara region of Western Australia. In addition, Macarthur has lithium brine Claims in the emerging Railroad Valley region in Nevada, USA.

This news release is not for distribution to United States services or for dissemination in the United States

Caution Regarding Forward Looking Statements

Certain of the statements made and information contained in this press release may constitute forward-looking information and forward-looking statements (collectively, “forward-looking statements”) within the meaning of applicable securities laws. All statements herein, other than statements of historical fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future, including but not limited to statements regarding expected completion of the Feasibility Study; conversion of Mineral Resources to Mineral Reserves or the eventual mining of the Project, are forward-looking statements. The forward-looking statements in this press release reflect the current expectations, assumptions or beliefs of the Company based upon information currently available to the Company. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and no assurance can be given that these expectations will prove to be correct as actual results or developments may differ materially from those projected in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include but are not limited to: unforeseen technology changes that results in a reduction in iron or magnetite demand or substitution by other metals or materials; the discovery of new large low cost deposits of iron magnetite; the general level of global economic activity; failure to complete the FS; inability to demonstrate economic viability of Mineral Resources; and failure to obtain mining approvals. Readers are cautioned not to place undue reliance on forward-looking statements due to the inherent uncertainty thereof. Such statements relate to future events and expectations and, as such, involve known and unknown risks and uncertainties. The forward-looking statements contained in this press release are made as of the date of this press release and except as may otherwise be required pursuant to applicable laws, the Company does not assume any obligation to update or revise these forward-looking statements, whether as a result of new information, future events or otherwise.

![]()

Seaborne Iron Ore Spot Price - 62% Fe Fines

Raw data source: Custeel.net

Seaborne Iron Ore Spot Price - Price Differentials by Fe % Grade

Raw data source: Custeel.net

A summary of MIO/MMS trading activity from October to December 2021