Generation Mining Delivers Updated Feasibility Study for Canada's Next Critical Mineral Mine - the Marathon Palladium-Copper Project

Generation Mining Limited (TSX: GENM; OTCQB: GENMF) (“Gen Mining” or the “Company”) is pleased to announce positive results on the updated Feasibility Study (“2023 FS” or the “Feasibility Study”) for the Marathon Palladium-Copper Project (the “Project”) located near the Town of Marathon in Northwestern Ontario. The 2023 FS presents an optimized design for the Project with improved clarity on anticipated capital and operating costs in the current inflationary environment. The 2023 FS outlines the operation of an open pit mine and process plant over a mine life of 12.5 years and replaces the Company’s March 2021 Feasibility Study (the “2021 FS”).

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20230330005863/en/

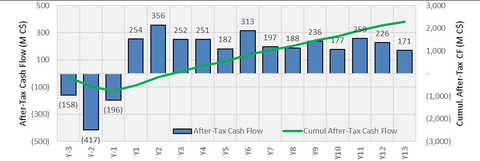

Project Cash Flow (After-Tax) (Graphic: Business Wire)

All dollar amounts are in Canadian dollars unless otherwise stated. All references to Mlbs are to millions of pounds and Moz are to millions of ounces and koz are to thousands of ounces.

Highlights:

- Robust economics1: An after-tax Net Present Value (“NPV”) at a 6% discount rate of $1.16 billion and Internal Rate of Return (“IRR”) of 25.8% based on a long-term price of US$1,800/oz for palladium and US$3.70/lb for copper

- Quick payback period on Initial Capital2,3: 2.3 years

- Initial Capital: $1,112 million ($898 million net of equipment financing and pre-commercial production revenue), an increase of 25% from the 2021 FS

- Low Operating Costs and attractive AISC: Life of mine (“LOM”) average operating costs of US$709/PdEq oz and all-in sustaining costs (“AISC”) of US$813/PdEq oz 3 . Operating costs have increased 14% compared with the 2021 FS.

- Increased Mineral Reserve Estimate: an increase of 8.5% in Mineral Reserves tonnages and a decreased open pit strip ratio

- Optimized operation: increased process plant throughput and improved metallurgical recoveries over LOM

- Average annual payable metals: 166 koz palladium, 41 Mlbs copper, 38 koz platinum, 12 koz gold and 248 koz silver

- LOM payable metals: 2.1 Moz palladium, 517 Mlbs copper, 485 koz platinum, 158 koz gold and 3.2 Moz silver

- Strong cash flows in first three years of production following commercial production: $851 million of free cash flow 3 , 580 koz of payable palladium and 132 Mlbs of payable copper

- Jobs: Creation of over 800 jobs during construction jobs and over 400 direct permanent jobs during operations

Jamie Levy, President and CEO of the Company, commented, “This updated Feasibility Study underscores just how robust the Marathon Project is, even in the current inflationary environment. This, combined with strong demand for critical minerals, makes the rationale for the Project becoming Canada’s next critical minerals mine more compelling than ever before. With the receipt of our Environmental Assessment approvals and our recently announced indicative offtake term sheets, we are advancing to arrange Project financing and working hard to obtain the permits necessary to start construction. The Project promises to be a near-term sustainable, environmentally sensitive, low-cost producer of critical metals that Canada and the rest of the world desperately need. On a copper equivalent basis, the Marathon Project, once in production, is expected to be one of the lowest CO2 equivalent intensity mines in the world. The metals we plan to produce will not only support emissions controls and the transition to a greener economy in Ontario and Canada, but they will also support job creation and economic prosperity for local, regional, and national stakeholders, in particular the First Nation community of Biigtigong Nishnaabeg and the Town of Marathon.”

Following the 2021 Feasibility Study, the Company undertook considerable work to optimize and de-risk the Project, including:

- Detailed engineering on the process plant, Tailing Storage Facility (“TSF”), and site infrastructure designs.

- Additional metallurgical test program to optimize the flowsheet and plant design and improve confidence in metallurgical recoveries. Results allowed the Company to remove the PGM-Scavenger circuit from the process plant design and lower the process plant unit-operating costs.

- Geotechnical investigations completed in areas of key infrastructure location and confirmed the locations chosen in the construction design.

- Additional diamond drilling of 18,995 m within the Marathon Deposit targeting key areas within the open pit Mineral Reserves in the first three years of planned production, and areas within and proximal to the overall Mineral Resources.

- Agreement finalized with Hycroft Mining Holding Corporation (“Hycroft”) for the purchase of an unused, surplus SAG mill and an unused, surplus ball mill4, which together with ancillary equipment allows the Company to increase throughput by 10% in the second full year of production.

- Community Benefits Agreement (“CBA”) signed and ratified with the Biigtigong Nishnaabeg (“BN”), on November 12, 2022.

- Federal and Provincial Environmental Assessment approvals received on November 30, 2022.

- Initiated the process of obtaining various federal and provincial permits and approvals required to construct and operate the project.

Drew Anwyll, P.Eng, Chief Operating Officer, said, “Our team has been working hard to develop the Marathon Project and has successfully optimized and improved confidence in the designs of the process plant, the open pits and the necessary infrastructure for the Project. Detailed design will advance, and we will continue to de-risk the Project in anticipation of finalizing the Project financing and receiving approval of the required permits to commence construction later in 2023.”

Upcoming Webinar:

For more information on the updated Feasibility Study please join Jamie Levy, President, Chief Executive Officer and Director, Kerry Knoll, Chairman and Director, and Drew Anwyll, Chief Operating Officer for a live event on Monday, April 3, 2023 at 10 am ET / 7 am PT. An opportunity to ask questions will follow the presentation. Click here to register: https://my.6ix.com/n9qfF5Nz

The Feasibility Study was prepared by the Company and G Mining Services Inc. (“GMS”), along with contributions from Wood Canada Limited, Knight Piésold Ltd., P&E Mining Consultants Inc. (“P&E”), and JDS Energy and Mining, Inc., and with support from LQ Consulting and Management Inc. and Haggarty Technical Services. The effective date of the Feasibility Study is December 31, 2022.

KEY RESULTS AND ASSUMPTIONS IN UPDATED FEASIBILITY STUDY

Key results and assumptions for the updated Feasibility Study are summarized below.

|

Units |

2023 FS |

2021 FS |

Production Data |

|||

Mine Life (operating) |

years |

12.5 |

12.8 |

Average Process Plant Throughput |

tpd |

27,700 |

25,200 |

Average Process Plant Throughput |

Mt/year |

10.1 |

9.2 |

Average Mining Rate |

tpd |

115,000 |

110,000 |

Average Mining Rate |

Mt/year |

42 |

40 |

Total Ore Mined |

Mt |

127 |

118 |

Strip Ratio |

waste:ore |

2.63 |

2.80 |

Palladium (payable) |

k oz |

2,122 |

1,905 |

Copper (payable) |

M lbs |

517 |

467 |

Platinum (payable) |

k oz |

485 |

537 |

Gold (payable) |

k oz |

158 |

151 |

Silver (payable) |

k oz |

3,156 |

2,823 |

LOM Palladium Equivalent Payable |

PdEq. koz |

3,613 |

3,195 |

Average Annual Palladium – Payable Metal |

k oz |

166 |

149 |

Average Annual Copper – Payable Metal |

M lbs |

41 |

36 |

Average Annual Platinum – Payable Metal |

k oz |

38 |

41 |

Average Annual Gold – Payable Metal |

k oz |

12 |

12 |

Average Annual Silver – Payable Metal |

k oz |

248 |

220 |

Operating Costs (Average LOM) |

|||

Mininga |

$/t mined |

3.25 |

2.53 |

Mining |

$/t milled |

11.45 |

9.23 |

Processing |

$/t milled |

8.70 |

9.08 |

G&Ab |

$/t milled |

2.67 |

2.48 |

Transport & Refining Charges |

$/t milled |

4.13 |

2.80 |

Royalty |

$/t milled |

0.09 |

0.04 |

Total Operating Cost |

$/t milled |

27.04 |

23.63 |

LOM Average Operating Costs |

US$/oz PdEq |

709 |

687 |

LOM Average AISCc |

US$/oz PdEq |

813 |

809 |

Capital Costs |

|||

Initial Capital |

$M |

1,112 |

888 |

Less: |

|

|

|

Pre-commercial production revenue |

$M |

($156) |

($171) |

Leased equipment, net of lease payments during construction |

$M |

($58) |

($53) |

Initial Capital (Adjusted) |

$M |

898 |

665 |

LOM Sustaining Capital |

$M |

424 |

423 |

Closure Costs |

$M |

72 |

66 |

Financial Evaluation |

|||

Pre-Tax Cash Flow (undiscounted) |

$M |

3,387 |

3,004 |

Pre-Tax NPV6% |

$M |

1,798 |

1,636 |

Pre-Tax IRR |

% |

31.9 |

38.6 |

Payback |

years |

2.0 |

1.9 |

Net Cash Flow (undiscounted) |

$M |

2,285 |

2,060 |

After-Tax NPV6% |

$M |

1,164 |

1,068 |

After-Tax IRR |

% |

25.8 |

29.7 |

Payback |

years |

2.3 |

2.3 |

Key Assumptionsd |

|||

Palladium Price |

US$/oz |

$1,800 |

$1,725 |

Copper Price |

US$/lb |

$3.70 |

$3.20 |

Platinum Price |

US$/oz |

$1,000 |

$1,000 |

Gold Price |

US$/oz |

$1,800 |

$1,400 |

Silver Price |

US$/oz |

$22.50 |

$20.00 |

Foreign Exchange (“FX”) |

C$:US$ |

1.35 |

1.28 |

Diesel Price |

$/litre |

1.17 |

0.77 |

Electricity |

$/kWhr |

0.07 |

0.08 |

Notes: a Including capitalized maintenance parts. b Includes estimated costs associated with certain commitments to and agreements with Indigenous communities. c AISC is calculated without the impact of the Precious Metal Purchase Agreement with Wheaton Precious Metals Corp. (“WPM PMPA”). d Metal Price Assumptions are based on the lesser of the three-year trailing average and the spot price on December 31, 2022, rounded to nearest interval. |

|||

LOM Metal Production |

Recovered Metal |

Payable Metal |

Revenue %a |

Palladium |

2,266 koz |

2,122 koz |

58 |

Copper |

548 Mlbs |

517 Mlbs |

29 |

Platinum |

607 koz |

485 koz |

7 |

Gold |

204 koz |

158 koz |

4 |

Silver |

4,529 koz |

3,156 koz |

1 |

Notes: a Excludes the impact of the WPM PMPA on gold and platinum revenues. |

|||

Mining

The Company will mine using conventional open pit, truck and shovel operating methods. Three open pits will be mined over the 12.5-year operating mine life, with an additional two years of pre-production mining to be undertaken where waste material is being mined for construction and ore stockpiling ahead of process plant commissioning. The mining equipment fleet is to be owner-operated and will include outsourcing of certain support activities such as explosives manufacturing and blasting. Production drilling and mining operations will take place on a 10 m bench height. The primary loading equipment will consist of 660 tonne hydraulic face shovels (29 m3 bucket size) and large front-end wheel loader (19 m3 bucket size). The loading fleet is matched with a fleet of 246 tonne haulage trucks. A fleet of 90 and 45 tonne excavators will be used to excavate the limited volume of overburden material and will also be allocated to mining the narrow-thickness ore zones, mainly associated with the W-Horizon in the South Pit, to mitigate additional dilution.

Peak mining production will be 43 Mt per year (118,000 tonnes per day (“t/d”)). Total material moved over the LOM is expected to be 460 Mt of which 128 Mt is ore.

The Marathon Deposit is well defined and characterized by ore outcropping on surface, with wide and moderately dipping mineralized zones.

The open pit operation includes a waste rock dump immediately to the east of the open pits and an ore stockpile (peak capacity of approximately 10 Mt) to the west of the pits, proximal to the crusher location.

Processing

The 2023 FS outlines the process plant throughput starting at 9.2 Mt per year (25,200 t/d) and increasing to 10.1 Mt per year (27,700 t/d) following the completion of the powerline upgrade scheduled year two of operations. The increase in process plant throughput is possible with the inclusion of the Hycroft mills in the plant design. The process plant will produce a copper-palladium concentrate (“Cu-PGM concentrate”).

The process plant flowsheet includes a conventional comminution circuit consisting of a SAG mill, followed by a ball mill (an “SAB” circuit). With the added capacity of the Hycroft mills, the pebble crusher (included in the 2021 FS) is no longer required. The flotation portion of the process plant includes rougher flotation, concentrate regrind and three stages of cleaning.

The process plant metallurgical recovery (at the average head grade) is estimated at an average of 88.0% palladium, 93.5% copper, 75.3% platinum, 71.5% gold and 66.4% silver. The phase 3 metallurgical test program demonstrated the PGM-Scavenger circuit outlined in the 2021 FS is no longer required.

The flotation circuit design was revised to replace the Direct Flotation Reactors previously included in the 2021 FS with conventional open tank cells for the roughers followed by Woodgrove Staged Flotation Reactors™ for the cleaning circuit. Concentrate thickening, concentrate filtering, tailings thickening, water management and a TSF complete the flowsheet.

Site Infrastructure

The existing regional infrastructure in the area of the Project is well established and will allow for the efficient logistics associated with Project execution and operations, including the movement of the Cu-PGM concentrate to a third-party off-site smelter.

All site infrastructure facilities, including the roads and access, process plant buildings, workshops, warehouse, administrative buildings, water treatment plants, explosives plant, communication systems, power and power transmission line required for the Project during construction and operation have been considered in the Project design. Off-site infrastructure (including transload concentrate facility, assay lab and accommodation units) required to support the operation have also been included.

The TSF design includes downstream constructed embankments using run-of-mine waste rockfill with embankments founded directly on bedrock. The majority of the TSF area consists of exposed bedrock with a thin intermittent layer of sand and gravel. The upstream face of the embankments includes an HDPE Geomembrane to minimize seepage. The construction methodology includes bulk material placement with the mining fleet. Associated with the TSF are separate water management facilities which will ensure the protection of the environment.

Between 2007 and 2022, there have been 10 geotechnical site investigation (“SI”) programs completed. The SI programs have focused on TSF foundation conditions and location of key site infrastructure, including the most recent drilling which focused on the process plant site, crusher, mine rock storage area and water management structures foundations. The recent and historical SI programs along with the 2021 detailed LiDAR™ topography and imagery survey have resulted in a good understanding of the geotechnical conditions for the Project.

Capital and Operating Cost Summary

The Initial Capital cost considers a construction timeframe of approximately 24 months followed by commissioning and ramp-up to commercial production5 over a period of approximately six months. During the pre-commercial production, the costs and revenue associated with operations will be capitalized and are included in the capital costs.

Construction Indirect costs and General and Owner’s costs are related to the expenses other than direct equipment purchases and direct construction costs.

Sustaining Capital items include future equipment purchases and replacements for the mining fleet and other site support equipment, the progressive build of the TSF over the LOM, and on and off-site infrastructure development to support the growth and contribute to operational improvements following initial construction.

The current capital cost estimate for the initial construction and the sustaining capital required during the LOM are shown in the table below. As noted above, this estimate represents a 25% ($224 million) increase to the initial construction capex reported in the 2021 FS. Within this increased capital cost, approximately 19% ($43 million) is due to scope changes, 71% ($160 million) is due to cost escalation and 10% ($22 million) with increased contingency.

Capital Costsa |

Initial ($M) |

Sustaining ($M) |

Total ($M) |

Mining and Surface Equipment |

117 |

130 |

247 |

Process Plant |

345 |

3 |

348 |

Infrastructure |

72 |

94 |

166 |

TSF, Water Management and Earthworks |

95 |

198 |

293 |

General and Owner’s Costs |

31 |

- |

31 |

Construction Indirects |

197 |

- |

197 |

Pre-production, Start-up and Commissioning |

159 |

- |

159 |

Contingencyb |

97 |

- |

97 |

Sub-Total |

1,112 |

424 |

1,537 |

Equipment Financing adjustment |

(58) |

- |

(58) |

Pre-Production Revenue |

(156) |

- |

(156) |

Total Capital (adjusted) |

898 |

424 |

1,322 |

Notes: a Sums in the table may not total due to rounding. b Contingency included at project sub-category basis and totals approximately 9.5%. |

|||

Operating Costs and AISC (LOM) |

$ M |

US$/oz PdEq |

Mining |

1,432 |

300 |

Process Plant |

1,087 |

228 |

General & Administration |

334 |

70 |

Concentrate Transport Costs |

230 |

48 |

Treatment & Refining Charges |

286 |

60 |

Royalties |

12 |

2 |

Total Operating Cost |

3,381 |

709 |

Closure & Reclamation |

72 |

15 |

Sustaining Capital |

424 |

89 |

All-in Sustaining Cost (AISC) |

3,878 |

813 |

Economic Analysis

The economic analysis is carried out in real terms (i.e., without inflation factors) in Q4 2022 Canadian Dollars without any project financing but inclusive of the WPM PMPA, and anticipated financing of mobile equipment and closure bonding.

To provide a better understanding of the economic impact of the WPM PMPA to the overall economics of the Project, the economic analysis is shown below including the economic impact of the WPM PMPA (as required under the National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and excluding the economic impact of the WPM PMPA.

The economic analysis does not take into account any potential economic benefits which the Marathon Project may qualify for under the new 30% investment tax credit on machinery and equipment acquired to extract and process critical minerals which was announced by the Government of Canada in its March 28, 2023 Federal Budget.

ECONOMIC ANALYSIS |

UNITS |

INCLUDING WPM PMPA |

EXCLUDING WPM PMPA |

Pre-tax Undiscounted Cash Flow |

$M |

3,387 |

3,780 |

Pre-tax NPV (6%) |

$M |

1,798 |

1,979 |

Pre-tax IRR |

% |

31.9 |

29.8 |

Pre-tax Payback |

years |

2.0 |

2.3 |

After-tax Undiscounted Cash Flow |

$M |

2,285 |

2,562 |

After-tax NPV (6%) |

$M |

1,164 |

1,285 |

After-tax IRR |

% |

25.8 |

24.2 |

After-tax Payback |

years |

2.3 |

2.5 |

Sensitivities

The Project has significant leverage to palladium and copper prices. The after-tax valuation sensitivities for the key metrics are shown below.

Palladium Price US$/oz |

1,400 |

1,600 |

1,700 |

1,800 |

1,900 |

2,000 |

2,200 |

NPV6% ($M) |

696 |

930 |

1,047 |

1,164 |

1,282 |

1,400 |

1,634 |

Payback (yrs) |

3.3 |

2.9 |

2.5 |

2.3 |

2.2 |

2.0 |

1.9 |

IRR (%) |

18.5 |

22.3 |

24.0 |

25.8 |

27.5 |

29.1 |

32.3 |

Copper Price US$/lb |

2.50 |

3.00 |

3.50 |

3.70 |

3.90 |

4.50 |

5.00 |

NPV6% ($M) |

836 |

972 |

1,109 |

1,164 |

1,219 |

1,386 |

1,522 |

Payback (yrs) |

3.0 |

2.6 |

2.4 |

2.3 |

2.2 |

2.0 |

1.9 |

IRR (%) |

21.1 |

23.1 |

25.0 |

25.8 |

26.5 |

28.7 |

30.4 |

After-Tax Results |

OPEX Sensitivity |

||||

+30% |

+15% |

0% |

-15% |

-30% |

|

NPV 6% ($M) |

1,031 |

1,085 |

1,164 |

1,274 |

1,411 |

Payback (yrs) |

2.7 |

2.5 |

2.3 |

2.1 |

2.0 |

IRR (%) |

23.4 |

24.4 |

25.8 |

27.4 |

29.2 |

After-Tax Results |

CAPEX Sensitivity |

||||

+30% |

+15% |

0% |

-15% |

-30% |

|

NPV 6% ($M) |

932 |

1,048 |

1,164 |

1,281 |

1,397 |

Payback (yrs) |

3.3 |

3.0 |

2.3 |

1.9 |

1.3 |

IRR (%) |

18.4 |

21.6 |

25.8 |

31.6 |

40.1 |

Discount Rate Sensitivity (%) |

NPV (After-Tax) ($M) |

|

Foreign Exchange Rate C$:US$ |

NPV (After-Tax) ($M) |

0 |

2,285 |

1.25 |

928 |

|

5 |

1,303 |

1.30 |

1,046 |

|

6 |

1,164 |

1.35 |

1,164 |

|

8 |

925 |

1.40 |

1,284 |

|

10 |

731 |

1.45 |

1,403 |

Fuel Price Sensitivity (C$/litre) |

NPV (After-Tax) ($M) |

|

Power Price Sensitivity ($/kWhr) |

NPV (After-Tax) ($M) |

0.90 |

1,197 |

0.05 |

1,207 |

|

1.00 |

1,185 |

0.06 |

1,186 |

|

1.10 |

1,173 |

0.07 |

1,164 |

|

1.17 |

1,164 |

0.08 |

1,143 |

|

1.30 |

1,148 |

0.09 |

1,121 |

|

1.40 |

1,136 |

0.10 |

1,100 |

Mineral Resources

The Mineral Resource Estimate below is for the combined Marathon, Geordie and Sally deposits. The Mineral Resource Estimates for Geordie and Sally were prepared by P&E. The Mineral Resource Estimate for Marathon was prepared by Gen Mining and reviewed by P&E.

Pit Constrained Combined Mineral Resource Estimate a-jfor the Marathon, Geordie and Sally Deposits (Effective date December 31, 2022)

Mineral

Classification |

Tonnes |

Pd |

Cu |

Pt |

Au |

Ag |

|||||

k |

g/t |

koz |

% |

M lbs |

g/t |

koz |

g/t |

koz |

g/t |

koz |

|

Marathon Deposit |

|||||||||||

Measured |

158,682 |

0.60 |

3,077 |

0.20 |

712 |

0.19 |

995 |

0.07 |

359 |

1.75 |

8,939 |

Indicated |

29,905 |

0.43 |

412 |

0.19 |

124 |

0.14 |

136 |

0.06 |

59 |

1.64 |

1,575 |

Meas. + Ind. |

188,587 |

0.58 |

3,489 |

0.20 |

836 |

0.19 |

1131 |

0.07 |

418 |

1.73 |

10,514 |

Inferred |

1,662 |

0.37 |

20 |

0.16 |

6 |

0.14 |

7 |

0.07 |

4 |

1.25 |

67 |

Geordie Deposit |

|||||||||||

Indicated |

17,268 |

0.56 |

312 |

0.35 |

133 |

0.04 |

20 |

0.05 |

25 |

2.4 |

1,351 |

Inferred |

12,899 |

0.51 |

212 |

0.28 |

80 |

0.03 |

12 |

0.03 |

14 |

2.4 |

982 |

Sally Deposit |

|||||||||||

Indicated |

24,801 |

0.35 |

278 |

0.17 |

93 |

0.2 |

160 |

0.07 |

56 |

0.7 |

567 |

Inferred |

14,019 |

0.28 |

124 |

0.19 |

57 |

0.15 |

70 |

0.05 |

24 |

0.6 |

280 |

Total Project |

|||||||||||

Measured |

158,682 |

0.60 |

3,077 |

0.20 |

712 |

0.19 |

995 |

0.07 |

359 |

1.75 |

8,939 |

Indicated |

71,974 |

0.43 |

1,002 |

0.22 |

350 |

0.14 |

316 |

0.06 |

140 |

1.5 |

3,493 |

Meas. + Ind. |

230,656 |

0.55 |

4,079 |

0.21 |

1,062 |

0.18 |

1,311 |

0.07 |

499 |

1.67 |

12,432 |

Inferred |

28,580 |

0.39 |

356 |

0.23 |

143 |

0.1 |

89 |

0.04 |

42 |

1.45 |

1,329 |

Notes:

|

|||||||||||

Mineral Reserves

The Mineral Reserve estimate for the Project includes only the Marathon Deposit. The Mineral Reserve Estimate was prepared by GMS.

Marathon Project Open Pit Mineral Reserve Estimatesa-i

(Effective Date of December 31, 2022)

Mineral Reserves |

Tonnes |

Pd |

Cu |

Pt |

Au |

Ag |

|||||

kt |

g/t |

koz |

% |

M lb |

g/t |

koz |

g/t |

koz |

g/t |

koz |

|

Proven |

114,798 |

0.65 |

2,382 |

0.21 |

530 |

0.20 |

744 |

0.07 |

259 |

1.68 |

6,191 |

Probable |

12,863 |

0.47 |

193 |

0.20 |

55 |

0.15 |

61 |

0.06 |

26 |

1.53 |

635 |

P & P |

127,662 |

0.63 |

2,575 |

0.21 |

586 |

0.20 |

806 |

0.07 |

285 |

1.66 |

6,825 |

Note:

|

|||||||||||

Community, Environment and Permitting

The Environmental Assessment for the Project was approved on November 30, 2022 in accordance with the Canadian Environmental Assessment Act and Ontario’s Environmental Assessment Act through a Joint Review Panel pursuant to the Canada-Ontario Agreement on Environmental Assessment Cooperation (2004).

As of the effective date of this Feasibility Study, the Project is in the process of obtaining various federal, provincial and municipal permits, approvals and licenses required to construct and operate the Project.

A total of 16 Indigenous groups were identified by the Crown (Canada and Ontario) as having a potential interest in the Project. Of the 16 Indigenous groups, seven groups indicated that they were interested in participating in the consultation processes related to the Project. The seven groups are Biigtigong Nishnaabeg First Nation, Pays Plat First Nation, Michipicoten First Nation, Ginoogaming First Nation, Superior North Shore Métis – MNO, Jackfish Métis – Ontario Coalition of Indigenous Peoples and Red Sky Métis Independent Nation.

The Project is situated within the geographic territory of the Robinson Superior Treaty area. It is also within lands claimed by BN as its asserted exclusive Aboriginal Title territory. In November 2022, a CBA was signed and ratified between BN and the Company for the development and operation of the Project.

Qualified Persons

The news release has been reviewed and approved by Drew Anwyll, P.Eng., M.Eng., Chief Operating Officer and Mauro Bassotti, P.Geo, Vice President of Geology both of the Company, and Qualified Persons as defined by Canadian Securities Administrators National Instrument 43-101 Standards of Disclosure for Mineral Projects. The independent Qualified Persons mentioned below have reviewed and approved their respective technical information contained in this news release.

The Technical Report was prepared through the collaboration of the following consulting firms and Qualified Persons:

Consultant Company |

Primary Area of Responsibility |

Qualified Persons |

G Mining Services Inc. |

Overall integration, Mineral Reserve Estimate, mining methods, concentrate logistics, economic analysis, operating costs pertaining to mining and G&A |

Carl Michaud, P.Eng Alexandre Dorval, P.Eng |

JDS Energy and Mining, Inc. |

Infrastructure, and power capital cost estimates, and project execution plan and schedule |

Jean-Francois Maille, P.Eng. |

Wood Canada Limited |

Recovery methods, processing plant capital and operating cost |

Ben Bissonnette, P.Eng. Joe Paventi, P.Eng. Sumit Nair, P.Eng. |

Knight Piésold Ltd. |

Tailings Storage Facility, water balance, geotechnical studies (mine rock storage piles, open pit and local infrastructure and foundations) |

Craig N. Hall, P.Eng. |

P&E Mining Consultants, Inc. |

Property description and location, accessibility, history, geological setting and mineralization, deposit types, exploration, drilling, sample preparation and security, data verification, and Mineral Resource Estimates and adjacent properties |

Eugene J. Puritch, P.Eng., FEC, CET Jarita Barry, P.Geo. Fred H. Brown, P.Geo. David Burga, P.Geo. William Stone, PhD, P.Geo. |

NI 43-101 Technical Report

Gen Mining plans to file the Feasibility Study as an NI 43-101 Technical Report on March 31, 2023. Readers are encouraged to read the Technical Report in its entirety, including all qualifications, assumptions and exclusions that relate to the details summarized in this news release. The Technical Report is intended to be read as a whole, and sections should not be read or relied upon out of context.

About the Company

Gen Mining’s focus is the development of the Marathon Project, a large undeveloped palladium-copper deposit in Northwestern Ontario. The Marathon Property covers a land package of approximately 22,000 hectares, or 220 square kilometers. Gen Mining owns a 100% interest in the Marathon Project and once constructed, it is expected to have a low carbon footprint.

Non-IFRS Financial Measures

The Company has included certain non-IFRS financial measures in this news release such as initial capital cost, cash operating costs and AISC per palladium equivalent ounce (“PdEq”), unit operating costs, and Free Cash Flow, which are not measures recognized under IFRS and do not have a standardized meaning prescribed by IFRS. For the reconciliation of cash costs and AISC, on both a per tonne and PdEq basis, please see the table set forth in the Capital and Operating Cost Summary above. Non-IFRS measures do not have any standardized meaning prescribed under IFRS, and therefore, they may not be comparable to similar measures employed by other companies. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. These measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers.

- Initial Capital includes all costs incurred from the Effective Date (excluding historical sunk costs) until the point where commercial production is achieved, including expenses related to engineering, equipment purchase and installation, process plant and mine infrastructure construction, and any other costs associated with putting the Project into operations.

- Initial Capital (Adjusted) includes all costs mentioned above in addition to adjustments for pre-commercial production revenue and equipment financing (net of payments, interest and fees incurred prior to commercial production).

- Operating Costs include mining, processing, general and administrative and other, concentrate transportation costs, treatment and refining charges, and royalties. Costs related to the Wheaton PMPA are excluded.

- AISC include Operating Costs, closure, and reclamation and sustaining capital. For the full reconciliation of cash costs and AISC, please see the Capital and Operating Cost Summary set out above.

- LOM Average AISC includes LOM AISC divided by LOM PdEq.

- LOM Average Operating Cost includes LOM Operating Costs divided by LOM PdEq.

- Free Cash Flow includes total revenue less Operating Costs, working capital adjustments, equipment financing, initial capital, sustaining capital and closure costs

- Palladium Equivalent ounces uses the formula PdEq oz = Pd oz +(Cu lb x 3.7 US$/lb + Pt oz x US$1000/oz + Au oz x US$1800/oz + Ag oz x US$22.5/oz) / US$1800 Pd/oz. The grades used are the average grades of the respective metals over the LOM.

Information Concerning Estimates of Mineral Reserves and Resources

The Mineral Reserve and Mineral Resource estimates in this press release have been disclosed in accordance with NI 43-101, which differs from the requirements of the U.S. Securities and Exchange Commission (the “SEC”), and information with respect to mineralization and Mineral Reserves and Mineral Resources contained herein may not be comparable to similar information disclosed by U.S. companies.

The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements under the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). These amendments became effective February 25, 2019 (the “SEC Modernization Rules”) with compliance required for the first fiscal year beginning on or after January 1, 2021. Under the SEC Modernization Rules, the historical property disclosure requirements for mining registrants included in Industry Guide 7 under the U.S. Securities Act of 1933, as amended, will be rescinded and replaced with disclosure requirements in subpart 1300 of SEC Regulation S-K. As a result of the adoption of the SEC Modernization Rules, the SEC now recognizes estimates of “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources.” In addition, the SEC has amended its definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” to be “substantially similar” to the corresponding standards under NI 43-101. While the SEC will now recognize “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources”, U.S. investors should not assume that any part or all of the mineralization in these categories will ever be converted into a higher category of Mineral Resources or into Mineral Reserves. Mineralization described using these terms has a greater amount of uncertainty as to its existence and feasibility than mineralization that has been characterized as reserves. Accordingly, U.S. investors are cautioned not to assume that any Measured Mineral Resources, Indicated Mineral Resources, or Inferred Mineral Resources that the Company reports are or will be economically or legally mineable. Further, “Inferred Mineral Resources” have a greater amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, U.S. investors are also cautioned not to assume that all or any part of the “Inferred Mineral Resources” exist. There is no assurance that any Mineral Reserves or Mineral Resources that the Company may report as “Proven Mineral Reserves”, “Probable Mineral Reserves”, “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources” under NI 43-101 would be the same had the Company prepared the Reserve or Resource Estimates under the standards adopted under the SEC Modernization Rules.

Mineral Resources are not Mineral Reserves, and do not have demonstrated economic viability, but do have reasonable prospects for economic extraction. Measured and Indicated Mineral Resources are sufficiently well defined to allow geological and grade continuity to be reasonably assumed and permit the application of technical and economic parameters in assessing the economic viability of the Mineral Resource. Inferred Mineral Resources are estimated on limited information not sufficient to verify geological and grade continuity or to allow technical and economic parameters to be applied. Inferred Mineral Resources are too speculative geologically to have economic considerations applied to them to enable them to be categorized as Mineral Reserves. There is no certainty that Mineral Resources of any classification can be upgraded to Mineral Reserves through continued exploration.

The Company’s Mineral Reserve and Mineral Resource figures are estimates and the Company can provide no assurances that the indicated levels of mineral will be produced or that the Company will receive the price assumed in determining its Mineral Reserves. Such estimates are expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. While the Company believes that these Mineral Reserve and Mineral Resource Estimates are well established and the best estimates of the Company’s management, by their nature Mineral Reserve and Mineral Resource Estimates are imprecise and depend, to a certain extent, upon analysis of drilling results and statistical inferences which may ultimately prove unreliable. If the Company’s Mineral Reserve or Mineral Reserve Estimates are inaccurate or are reduced in the future, this could have an adverse impact on the Company’s future cash flows, earnings, results or operations and financial condition.

The Company estimates the future mine life of the Marathon Project. The Company can give no assurance that its mine life estimate will be achieved. Failure to achieve this estimate could have an adverse impact on the Company’s future cash flows, earnings, results of operations and financial condition.

Forward-Looking Information

This news release contains certain forward-looking information and forward-looking statements, as defined in applicable securities laws (collectively referred to herein as "forward-looking statements"). Forward-looking statements reflect current expectations or beliefs regarding future events or the Company’s future performance. All statements other than statements of historical fact are forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "continues", "forecasts", "Projects", "predicts", "intends", "anticipates", "targets" or "believes", or variations of, or the negatives of, such words and phrases or state that certain actions, events or results "may", "could", "would", "should", "might" or "will" be taken, occur or be achieved, including statements related to mineral resource and reserve estimates, proposed mine production plans, projected mining and process recovery rates (including mining dilution), estimates related closure costs and requirements, metal price and other economic assumptions (including currency exchange rates), projected capital and operating costs, and AISC, economic analysis estimates (including cash flow forecasts, IRRs and NPVs) and mine life.

Although the Company believes that the expectations expressed in such statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the statements. There are certain factors that could cause actual results to differ materially from those in the forward-looking information. These include the timing for a construction decision; the progress of development at the Marathon Project, including progress of project expenditures and contracting processes, the Company's plans and expectations with respect to liquidity management, continued availability of capital and financing, the future price of palladium and other commodities, permitting timelines, exchange rates and currency fluctuations, increases in costs, requirements for additional capital, and the Company's decisions with respect to capital allocation, and the impact of COVID-19, inflation, global supply chain disruptions and the war in Ukraine on the Company, the project schedule for the Marathon Project, key inputs, staffing and contractors, commodity price volatility, continued availability of capital and financing, uncertainties involved in interpreting geological data, environmental compliance and changes in environmental legislation and regulation, the Company’s relationships with First Nations communities, exploration successes, and general economic, market or business conditions, as well as those risk factors set out in the Company’s annual information form for the year ended December 31, 2022, and in the continuous disclosure documents filed by the Company on SEDAR at www.sedar.com. Readers are cautioned that the foregoing list of factors is not exhaustive of the factors that may affect forward-looking statements. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements in this news release speak only as of the date of this news release or as of the date or dates specified in such statements.

Forward-looking statements are based on a number of assumptions which may prove to be incorrect, including, but not limited to, assumptions relating to: the availability of financing for the Company’s operations; operating and capital costs; results of operations; the mine development and production schedule and related costs; the supply and demand for, and the level and volatility of commodity prices; timing of the receipt of regulatory and governmental approvals for development Projects and other operations; the accuracy of Mineral Reserve and Mineral Resource Estimates, production estimates and capital and operating cost estimates; and general business and economic conditions.

Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking information. For more information on the Company, investors are encouraged to review the Company’s public filings on SEDAR at www.sedar.com. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

______________________________

1 Unless otherwise noted, the economic analysis includes the impacts of the WPM PMPA on the project cash flows.

2 The initial capital cost excludes the receipt of any deposits delivered under the WPM PMPA. However, such despots are included in the economic analysis used to determine expected cash flows, which are used to calculate NPVs, IRRs and Payback Period.

3 Refer to “Non-IFRS Measures” section.

4 See News Release from 8 August 2022. This Agreement was subsequently amended to include the purchase of the main transformer and substation equipment for the process plant

5 30-days achieving 60% of the plant initial nameplate throughput capacity (25,200 tpd)

View source version on businesswire.com: https://www.businesswire.com/news/home/20230330005863/en/