Kirkland Lake Gold Reports Record Earnings Per Share of $0.84 in Third Quarter 2019, Company Announces 50% Increase in Common Dividend

TORONTO, Nov. 06, 2019 (GLOBE NEWSWIRE) -- Kirkland Lake Gold Ltd. (“Kirkland Lake Gold” or the “Company”) (TSX:KL) (NYSE:KL) (ASX:KLA) today announced the Company’s financial and operating results for the third quarter (“Q3 2019”) and first nine months of 2019 (“YTD 2019”). The Q3 2019 results include record earnings and cash flows driven largely by strong growth in gold production and improved unit costs. The Company’s cash position increased $146.6 million or 31% during Q3 2019, totaling $615.8 million at September 30, 2019. On November 6, 2019 the Company announced a $0.02 per share increase to the quarterly dividend, to $0.06 per share, commencing with the fourth quarter 2019 dividend payment to be paid in January 2020. The Company’s full consolidated financial statements and management discussion & analysis are available on SEDAR at www.sedar.com and on the Company’s website at www.klgold.com. All dollar amounts are in U.S. dollars, unless otherwise noted.

Key highlights of Q3 2019 results include:

- Record net earnings: Net earnings of $176.6 million ($0.84 per basic share) more than triple net earnings of $55.9 million ($0.27 per basic share) in Q3 2018 and 69% higher than $104.2 million ($0.50 per basic share) the previous quarter; adjusted net earnings in Q3 2019 were the same as net earnings and increased 188% from $61.4 million ($0.29 per basic share) in Q3 2018 and 67% from $105.5 million ($0.50 per basic share) in Q2 2019.

- Revenue grows 71%: Revenue totaled $381.4 million, 71% increase from $222.7 million in Q3 2018 and 36% higher than $281.3 million the previous quarter;

- Significant growth in EBITDA1,2: EBITDA of $296.4 million, 148% higher than $119.6 million in Q3 2018 and 60% increase from $185.8 million in Q2 2019

- Operating cash flow increases 145%: Net cash provided by operating activities of $316.8 million, 145% growth from $129.3 million in Q3 2018 and 76% higher than $179.7 million the previous quarter

- Record free cash flow1: Free cash flow of $181.3 million, more than triple the Q3 2018 and Q2 2019 levels of $53.1 million and $54.4 million, respectively, with substantial growth in free cash flow being achieved at the same time that capital expenditures increased in support of advancing key growth projects

- Growth projects ramp up: Growth capital expenditures1 totaled $50.2 million in Q3 2019 (excluding capitalized exploration), including $33.8 million at Macassa and $11.3 million at Fosterville; full-face sinking at Macassa #4 shaft project commenced in August 2019 and was advanced more than 600 feet by November 6, 2019

- Continued focus on exploration: Exploration and evaluation expenditures in Q3 2019 totaled $43.6 million ($5.9 million expensed and $37.7 million capitalized), with $32.4 million relating to ongoing advanced exploration work in the Northern Territory.

- Continued strong operating results

º Production of 248,400 ounces, 38% increase from 180,155 ounces in Q3 2018 and 16% higher than 214,593 ounces the previous quarter

º Production costs of $73.7 million compared to $64.9 million in Q3 2018 and $66.2 million in Q2 2019

º Operating cash costs per ounce sold1 averaged $287, 18% improvement from $351 in Q3 2018 and 8% better than $312 in Q2 2019

º AISC per ounce sold1 averaged $562, 13% better than $645 in Q3 2018 and 12% improvement from $638 the previous quarter. - Cash at September 30, 2019 totaled $615.8 million, 31% increase from $469.4 million at June 30, 2019 and 85% higher than $332.2 million at December 31, 2018.

Key highlights of YTD 2019 results include:

- Record nine-month financial results

º Net earnings of $390.9 million ($1.86 per basic share), 134% increase from $167.4 million ($0.79 per basic share) for first nine months of 2018 (“YTD 2018”)

º Adjusted net earnings of $394.2 million ($1.88 per basic share), 122% higher than $177.6 million ($0.84 per basic share) for YTD 2018

º Net cash provided by operating activities of $672.3 million, 97% growth from $341.5 million for YTD 2018

º Free cash flow totaling $330.2 million, double the YTD 2018 level of $163.1 million

º Revenue of $967.6 million, 52% growth from $635.6 million for YTD 2018

º EBITDA of $683.8 million, 99% increase from $343.9 million for YTD 2018. - Strong YTD 2019 operating results

º Production of 694,873 ounces, 41% increase from 492,484 ounces for YTD 2018

º Operating cash cost per ounce sold of $296, 25% improvement from $397 for the same period in 2018

º AISC per ounce sold of $584, 21% better than $738 for YTD 2018. - Strong focus on shareholder returns in YTD 2019

º Common share price increased 67% for YTD 2019 to C$59.35 per share (on TSX) at September 30, 2019 from C$35.60 per share at December 31, 2018 (C$59.92 per share at November 5, 2019)

º Quarterly dividend increased to $0.04/share (from C$0.04/share) for second quarter 2019 dividend, paid on July 12, 2019 to shareholders of record on June 28, 2019; change to paying dividend in US dollars increases value of dividend by approximately 30%; Q3 2019 dividend of $0.04 per share paid on October 11, 2019 to shareholders of record on September 30, 2019

º Additional dividend increase of $0.02 per share or 50%, to $0.06 per share, commencing with Q4 2019 dividend payment to be paid in January 2020 to shareholders of record as of December 31, 2019.

__________

1. See “Non-IFRS Measures” later in this press release and in the MD&A for the three and nine months ended September 30, 2019.

2. Refers to Earnings before Interest, Taxes, Depreciation, and Amortization.

Tony Makuch, President and Chief Executive Officer of Kirkland Lake Gold, commented: “Q3 2019 was our best quarter to date driven by exceptional results at Fosterville and a solid quarter of performance at Macassa. At Fosterville, production increased by almost 70,000 ounces from Q3 2018 largely reflecting a 75% improvement in the average grade, to 41.8 g/t. Grades of this level are rarely seen in our industry and resulted from the ramp up in production of the high-grade Swan Zone. We mined our first Swan stope during last year’s third quarter, which contributed about 7,500 ounces of production. We have ramped up production since then and, in Q3 2019, mined 11 Swan Zone stopes, which contributed about 94% of the 158,327 ounces produced for the quarter. Substantially higher grades resulted in further improvement in unit costs which, combined with rising gold prices, led to significant margin expansion at Fosterville during the quarter. Turning to Macassa, the mine had a strong quarter in Q3 2019 with tonnes processed increasing 18% and the average grade improving to 23.3 g/t from 21.5 g/t in Q2 2019. We expect Fosterville and Macassa to finish 2019 with strong fourth quarters, which will position both mines to easily achieve their full-year 2019 production guidance of 570,000 – 610,000 ounces and 240,000 – 250,000 ounces, respectively. At the Holt Complex, we have lowered our production guidance for full-year 2019 based on results to date and are now assessing a future strategy for this operation.

“Turning to our growth programs, full-face sinking at the Macassa #4 shaft project commenced during August, with the shaft now having advanced to a depth of over 600 feet. Work is progressing well, with the project remaining on track for phase one completion during the second quarter of 2022. At Fosterville, our key growth projects are either complete or nearing completion. Our new water treatment plant was commissioned during the third quarter and is now in operation. Construction of our new paste fill plant is largely finished with commissioning to be completed by the end of the year. Work related to our new ventilation system is continuing and should be completed around year end, with commissioning to follow in early 2020. In the Northern Territory, advanced exploration work continues to accelerate, with initial processing of Lantern Deposit material at the Union Reefs Mill commencing in October. We continue to work towards a potential restart of operations in the Northern Territory as early as the beginning of next year.”

REVIEW OF FINANCIAL PERFORMANCE

Table 1. Financial Highlights

| (in thousands of dollars, except per share amounts) | Three Months Ended September 30, 2019 | Three Months Ended September 30, 2018 | Nine Months Ended September 30, 2019 | Nine Months Ended September 30, 2018 | ||||||||

| Revenue | $ | 381,430 | $ | 222,701 | $ | 967,609 | $ | 635,591 | ||||

| Production costs | 73,664 | 64,851 | 209,865 | 202,828 | ||||||||

| Earnings before income taxes | 254,119 | 82,977 | 566,140 | 244,974 | ||||||||

| Net earnings | $ | 176,604 | $ | 55,885 | $ | 390,945 | $ | 167,408 | ||||

| Basic earnings per share | $ | 0.84 | $ | 0.27 | $ | 1.86 | $ | 0.79 | ||||

| Diluted earnings per share | $ | 0.83 | $ | 0.26 | $ | 1.85 | $ | 0.79 | ||||

| Cash flow from operating activities | $ | 316,753 | $ | 129,297 | $ | 672,290 | $ | 341,507 | ||||

| Cash investment on mine development and PPE | $ | 135,449 | $ | 76,190 | $ | 342,104 | $ | 175,878 | ||||

Table 2. Operating Highlights

| Three Months Ended September 30, 2019 | Three Months Ended September 30, 2018 | Nine Months Ended September 30, 2019 | Nine Months Ended September 30, 2018 | |||||||||||||

| Tonnes milled | 419,787 | 435,600 | 1,208,106 | 1,259,142 | ||||||||||||

| Grade (g/t Au) | 18.8 | 13.3 | 18.3 | 12.6 | ||||||||||||

| Recovery (%) | 97.9 | % | 96.9 | % | 98.0 | % | 96.5 | % | ||||||||

| Gold produced (oz) | 248,400 | 180,155 | 694,873 | 492,484 | ||||||||||||

| Gold Sold (oz) | 256,276 | 184,517 | 701,296 | 496,585 | ||||||||||||

| Average realized price ($/oz sold)(1) | $ | 1,482 | $ | 1,204 | $ | 1,375 | $ | 1,275 | ||||||||

| Operating cash costs per ounce ($/oz sold)(1) | $ | 287 | $ | 351 | $ | 296 | $ | 397 | ||||||||

| AISC ($/oz sold)(1) | $ | 562 | $ | 645 | $ | 584 | $ | 738 | ||||||||

| Adjusted net earnings(1) | $ | 176,621 | $ | 61,421 | $ | 394,289 | $ | 177,552 | ||||||||

| Adjusted net earnings per share(1) | $ | 0.84 | $ | 0.29 | $ | 1.88 | $ | 0.84 | ||||||||

- Non-IFRS – the definition and reconciliation of these Non-IFRS measures are included in the Company’s MD&A for the three and nine months ended September 30, 2019.

Table 3. Review of Financial Performance

| (in thousands except per share amounts) | Three Months Ended September 30, 2019 | Three Months Ended September 30, 2018 | Nine Months Ended September 30, 2019 | Nine Months Ended September 30, 2018 | ||||||||

| Revenue | $ | 381,430 | $ | 222,701 | $ | 967,609 | $ | 635,591 | ||||

| Production costs | (73,664 | ) | (64,851 | ) | (209,865 | ) | (202,828 | ) | ||||

| Royalty expense | (10,430 | ) | (6,600 | ) | (25,430 | ) | (18,835 | ) | ||||

| Depletion and depreciation | (41,692 | ) | (35,968 | ) | (116,056 | ) | (96,400 | ) | ||||

| Earnings from mine operations | 255,644 | 115,282 | 616,258 | 317,528 | ||||||||

| Expenses | ||||||||||||

| General and administrative(1) | (10,559 | ) | (6,021 | ) | (34,789 | ) | (22,249 | ) | ||||

| Exploration and evaluation | (5,897 | ) | (20,341 | ) | (24,133 | ) | (52,807 | ) | ||||

| Care and maintenance | (541 | ) | (416 | ) | (952 | ) | (1,455 | ) | ||||

| Earnings from operations | 238,647 | 88,504 | 556,384 | 241,017 | ||||||||

| Finance and other items | ||||||||||||

| Other income (loss), net | 13,850 | (5,759 | ) | 6,349 | 3,895 | |||||||

| Finance income | 2,198 | 914 | 4,993 | 2,575 | ||||||||

| Finance costs | (576 | ) | (682 | ) | (1,586 | ) | (2,513 | ) | ||||

| Earnings before taxes | 254,119 | 82,977 | 566,140 | 244,974 | ||||||||

| Current income tax expense | (50,946 | ) | (8,001 | ) | (127,158 | ) | (23,673 | ) | ||||

| Deferred tax expense | (26,569 | ) | (19,091 | ) | (48,037 | ) | (53,893 | ) | ||||

| Net earnings | $ | 176,604 | $ | 55,885 | $ | 390,945 | $ | 167,408 | ||||

| Basic earnings per share | $ | 0.84 | $ | 0.27 | $ | 1.86 | $ | 0.79 | ||||

| Diluted earnings per share | $ | 0.83 | $ | 0.26 | $ | 1.85 | $ | 0.79 | ||||

- General and administrative expense for Q3 2019 include general and administrative expenses of $7.9 million ($5.6 million in Q3 2018 and $9.8 million in Q2 2019) and share based payment expense of $2.7 million ($0.5 million in Q3 2018 and $2.4 million in Q2 2019).

Revenue

Revenue in Q3 2019 totaled $381.4 million, an increase of $158.7 million or 71% from $222.7 million in Q3 2018. Of the increase in revenue, $86 million related to a 71,759 ounce or 39% increase in total gold sales, to 256,276 ounces. The primary factors driving the increase in sales were higher grades and increased mill throughput at Fosterville, where gold sales grew by 70,364 ounces or 73%, to 166,903 ounces. The realized gold price in Q3 2019 averaged $1,482 per ounce, a 23% improvement from $1,204 per ounce for the same period in 2018. The higher gold price had an $71 million favourable impact on the change in revenue versus Q3 2018.

Q3 2019 revenue increased $100.1 million or 36% from $281.3 million the previous quarter, with $58 million related to a 44,185 ounce or 21% increase in gold sales from Q3 2019 from 212,091 ounces the previous quarter. Gold sales increased quarter over quarter at all three mining operations, with Fosterville’s gold sales growing 33,422 ounces or 25% reflecting increased production levels. Gold sales at Macassa of 62,583 ounces were 7,573 ounces or 14% higher, while gold sales from the Holt Complex increased 3,190 ounces or 14% quarter over quarter, to 26,790 ounces. Contributing $42 million to the increase in revenue was a higher average realized gold price, which increased 12% to $1,482 per ounce from $1,320 per ounce in Q2 2019.

Revenue in YTD 2019 totaled $967.6 million, an increase of $332.0 million or 52% from $635.6 million in YTD 2018. The increase in revenue from YTD 2018 reflected a 41% increase in gold sales, to 701,296 ounces, which had a $261 million favourable impact on revenue compared to YTD 2018. The average realized gold price in YTD 2019 was $1,375 per ounce, an 8% increase from $1,275 per ounce for YTD 2018. The change in the gold price increased revenue by $70 million for YTD 2019 compared to the first nine months of 2018. The strong growth in gold sales was driven by Fosterville, where gold sales rose 85% to 432,432 ounces. Gold sales at Macassa increased 9%, to 184,898 ounces due to a higher average grade, which more than offset lower tonnes processed. Gold sales at Holt Complex for YTD 2019 totaled 83,966 ounces versus 93,255 ounces for the same period in 2018.

Click to view Revenue charts: https://www.globenewswire.com/NewsRoom/AttachmentNg/053f3e51-061e-4929-a474-3051c6c9dbf1

Earnings from Mine Operations

Earnings from mine operations in Q3 2019 totaled $255.6 million, an increase of 122% from $115.3 million in Q3 2018. The increase mainly reflected higher levels of revenue versus the same period in 2018. Production costs in Q3 2019 totaled $73.7 million compared to $64.9 million in Q3 2018, with the increase largely related to the resumption of operations at the Holloway Mine in Q1 2019. Depletion and depreciation costs totaled $41.7 million, which compared to $36.0 million in Q3 2018, as the impact of higher production volumes in Q3 2019 more than offset a reduction in depletion and depreciation expense on a per ounce produced basis driven by a larger depletion and depreciation base. Royalty expense in Q3 2019 totaled $10.4 million versus $6.6 million in Q2 2018, mainly reflecting the significant growth in gold sales versus Q3 2018.

Q3 2019 earnings from mine operations of $255.6 million compared to earnings from mine operations of $175.3 million the previous quarter, with the increase reflecting higher levels of revenue in Q3 2019. Production costs, depletion and depreciation costs and royalty expense were all higher in Q3 2019 compared to the previous quarter, mainly reflecting higher production and sales volumes.

For YTD 2019, earnings from mine operations totaled $616.3 million, an increase of 94% from $317.5 million for YTD 2018. The year-over-year increase mainly resulted from strong revenue growth. Production costs totaled $209.9 million compared to $202.8 million for YTD 2018. Depletion and depreciation costs increased to $116.1 million from $96.4 million for YTD 2018, while royalty expense totaled $25.4 million versus $18.8 million for YTD 2018, with higher sales volumes accounting for the increase.

Unit Cost Performance (See Non-IFRS measures)

Click to view Op. Cash Costs and Gold Sales charts: https://www.globenewswire.com/NewsRoom/AttachmentNg/56b8e893-62a9-4f22-aa38-e6f44bfb2c3a

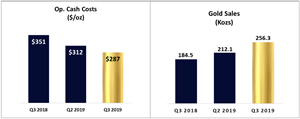

Operating cash costs per ounce sold averaged $287, a $64 or 18% improvement from $351 in Q3 2018 and 8% better than $312 the previous quarter. Compared to Q3 2018, the improvement largely reflected increased sales volumes resulting from a 41% increase in the Company's average grade, to 18.8 g/t from 13.3 g/t for the same period, with average grades at Fosterville and Macassa increasing 63% and 21%, respectively. The improvement from the previous quarter was mainly due to higher gold sales driven by both improved grades and increased mill throughput at Fosterville and Macassa. The average grade of 18.8 g/t in Q3 2019 compared to an average grade of 18.4 g/t the previous quarter with the impact of higher grades at Fosterville and Macassa being partially offset by significantly higher tonnes processed at lower average grades at the Holt Complex.

Operating cash costs per ounce sold for YTD 2019 improved 8% year over year, to $296 for YTD 2019 versus $397 for YTD 2018. The increase resulted from the favourable impact on sales of a 45% increase in the average grade (18.3 g/t versus 12.6 g/t in YTD 2018), which more than offset the higher operating cash costs in Q3 2019, $207.3 million versus $197.2 million the previous quarter. Increases of 74% and 23%, respectively, in the average grades at Fosterville and Macassa drove the increase in the consolidated average grade in Q3 2019.

Click to view AISC Q3 2019 charts: https://www.globenewswire.com/NewsRoom/AttachmentNg/6d7943ab-0993-417b-a47d-9ced3f5237dd

AISC per ounce sold in Q3 2019 averaged $562, $83 or 13% better than Q3 2018, with lower operating cash costs per ounce sold largely accounting for the improvement. In addition, while sustaining capital expenditures increased to $48.3 million in Q3 2019 from $41.4 million in Q3 2018, they improved on a per ounce sold basis, to $188 per ounce sold in Q3 2019 from $224 per ounce sold for the same period in 2018 reflecting the favourable impact of higher sales volumes. Partially offsetting the favorable impact of lower operating costs and sustaining capital expenditures per ounce sold were higher royalty, share-based compensation and general and administrative expenses. Compared to the previous quarter, AISC per ounce sold of $562 in Q3 2019 improved 12% from $638 in Q2 2019, reflecting improved operating cash costs per ounce sold as well as lower sustaining capital expenditures on a quarter-over-quarter basis. Sustaining capital expenditures in Q3 2019 of $48.3 million or $188 per ounce sold compared to sustaining capital expenditures of $49.8 million or $235 per ounce sold the previous quarter.

Click to view AISC YTD chart: https://www.globenewswire.com/NewsRoom/AttachmentNg/9d4fafa1-3430-42b1-880c-07584679f140

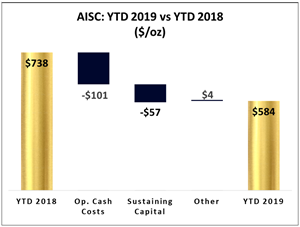

For YTD 2019, AISC per ounce sold averaged $584, 21% better than $738 for YTD 2018, largely reflecting the favourable impact of higher average grades on production and sales levels for YTD 2019 versus the same period in 2018. In addition to the $101 or 25% improvement in operating cash costs per ounce, the change in AISC also reflected a $57 per ounce or 22% reduction in sustaining capital expenditures per ounce sold for YTD 2019, to $200 per ounce from $257 per ounce for YTD 2018.

Additional Expenses

Corporate G&A expense (excluding share-based payments expense and transaction costs) totaled $7.9 million compared to $5.6 million in Q3 2018 and $9.8 million the previous quarter. The increase from Q3 2018 largely related to the expansion of corporate capabilities in both Canada and Australia in support of the Company's continued growth. Share based payment expense in Q3 2019 totaled $2.7 million versus $0.5 million for the same period in 2018 and $2.4 million the previous quarter. The increase in share-based payment expense from Q3 2018 largely related to share-price appreciation, resulting in greater mark-to-market values for the Company’s outstanding deferred-share units. YTD corporate G&A expense totaled $26.3 million compared to $18.3 million for YTD 2018. Share based payment expense for YTD 2019 totaled $8.5 million versus $3.9 million for YTD 2018.

Exploration and evaluation expenditures (expensed) in Q3 2019 totaled $5.9 million versus $20.3 million in Q3 2018 and $6.2 million the previous quarter. As a result of a review of the Company's drilling programs during Q2 2019, and the extent to which drilling is being completed contiguous to, and for the purpose of extending existing mining areas, a greater proportion of exploration expenditures beginning in Q2 2019 and continuing through Q3 2019 were capitalized compared to previous quarters. YTD 2019 exploration and evaluation expenditures (expensed) totaled $24.1 million versus $52.8 million for YTD 2018.

Other income in Q3 2019 totaled $13.9 million, which compared to other loss of $5.8 million in Q3 2018 and other loss of $5.4 million the previous quarter. Other income in Q3 2019 mainly resulted from a $13.7 million unrealized and realized foreign exchange gain, due mainly to the weakening of the Australian dollar against the US dollar during Q3 2019. Other loss in Q3 2018 resulted from a $6.4 million mark-to-market loss on fair valuing the Company’s warrant investments, partially offset by a $0.6 million unrealized and realized foreign exchange gain. Other loss in Q2 2019 reflected a $4.5 million unrealized and realized foreign exchange loss, largely reflecting the strengthening of the Canadian dollar relative to the US and Australian dollars during Q2 2019, as well as a $0.9 million mark-to-market loss on fair valuing warrants. For YTD 2019, other income totaled $6.3 million as an unrealized and realized foreign exchange gain of $7.1 million was only partially offset by a $0.9 million mark-to-market loss related to fair valuing of the Company’s warrant investments. For YTD 2018, other income totaled $3.9 million, as an unrealized and realized foreign exchange gain of $11.0 million was only partially offset by a $7.3 million market-to-market loss on the fair valuing of warrants.

Finance costs in Q3 2019 totaled $0.6 million, mainly reflecting interest expense on financial leases and other loans. Finance costs totaled $0.7 million in Q3 2018 and $0.3 million the previous quarter. YTD 2019 finance costs totaled $1.6 million versus $2.5 million for YTD 2018.

Finance income, mainly related to interest income on bank deposits, totaled $2.2 million in Q3 2019 versus $0.9 million for the same period in 2018 and $1.4 million the previous quarter. YTD 2019 finance income totaled $5.0 million compared to $2.6 million for YTD 2018, with the increase reflecting higher cash balances during the first nine months of 2019 versus the same period in 2018.

Income tax expense in Q3 2019 included current income tax expense of $50.9 million and deferred income tax expense of $26.6 million. In Q3 2018, current income tax expense totaled $8.0 million, with deferred income tax expense totaling $19.1 million with the high level of deferred income tax expense resulting from the utilization of $24.6 million of deferred tax assets in respect of loss carry-forwards during Q3 2018 to reduce current income tax expense. Q2 2019 included current income tax expense of $35.3 million and deferred income tax expense of $12.9 million. The Company’s effective tax rate in Q3 2019 was 30.5%, which compared to 32.7% in Q3 2018 and 31.6% in the previous quarter. For YTD 2019, current income tax expense totaled $127.2 million versus $23.7 million for YTD 2018, while deferred income tax expense for YTD 2019 was $48.0 million compared to $53.9 million for the same period in 2018. The higher levels of deferred income tax expense compared to current income tax expense for YTD 2018 resulted from the utilization of $53.3 million of deferred tax assets in respect of loss carry-forwards during the first three quarters of 2018 to reduce current income tax expense. The Company’s effective tax rate for YTD 2019 was 30.9% compared to 31.7% for YTD 2018.

Net earnings in Q3 2019 total $176.6 million or $0.84 per basic share

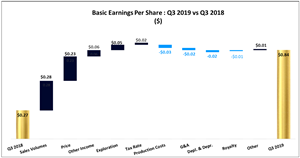

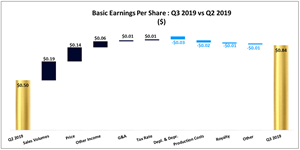

Net earnings in Q3 2019 totaled $176.6 million ($0.84 per basic share) an increase of $120.7 million or 216% from $55.9 million ($0.27 per basic share) in Q3 2018 and $72.4 million or 69% from $104.2 million ($0.50 per basic share) the previous quarter. The increase in net earnings and earnings per share from Q3 2019 largely resulted from a 71% increase in revenue, reflecting both higher volumes and gold prices, lower expensed exploration and evaluation expenditures, the impact of a $13.7 million pre-tax unrealized and realized foreign exchange gain ($9.5 million after income taxes), which was included in other income and a reduction in the effective tax rate. Partially offsetting these factors were higher production costs, increased depletion and depreciation costs, higher corporate G&A expense and increased royalty expense. The increase in net earnings from Q2 2019 reflected the favourable impact of higher gold sales and gold prices on revenue, the contribution of foreign exchange gains to other income, lower corporate G&A and a lower effective tax rate. These factors were partially offset by higher depletion and depreciation expense, production costs and royalty expense.

Click to view Basic Earnings Per Share Q3 2019 vs Q3 2018 chart: https://www.globenewswire.com/NewsRoom/AttachmentNg/72ebc4e9-cccf-4c49-9f26-4dea944dac9c

Click to view Basic Earnings Per Share Q3 2019 vs Q2 2019 chart: https://www.globenewswire.com/NewsRoom/AttachmentNg/d2b931db-b884-4405-8c04-6aae3b7847fb

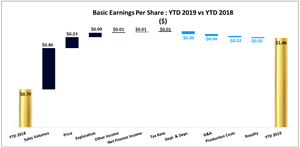

Net earnings for YTD 2019 totaled $390.9 million ($1.86 per basic share), an increase of $223.5 million or 134% from $167.4 million ($0.79 per basic share) in YTD 2018. The increase in net earnings and earnings per share was driven by strong revenue growth and lower exploration and evaluation expense. Partially offsetting these favourable factors were higher depletion and depreciation costs, corporate G&A costs and higher royalty expense resulting from increased sales volumes.

Click to view Basic Earnings Per Share YTD chart: https://www.globenewswire.com/NewsRoom/AttachmentNg/9de9e806-5005-4cb7-b139-22a72cb6a1c5

Adjusted net earnings (Non-IFRS) in Q3 2019 total $176.6 million or $0.84 per basic share

The Company's adjusted net earnings in Q3 2019 totaled $176.6 million ($0.84 per basic share), $115.2 million or 188% higher than $61.4 million ($0.29 per basic share) in Q3 2018 and an increase of $71.1 million or 67% from $105.5 million ($0.50 per basic share) the previous quarter. There was no difference between net earnings and adjusted net earnings in Q3 2019. The difference between net earnings and adjusted net earnings in Q3 2018 mainly reflected the exclusion of a $6.4 million ($5.5 million after income tax) mark-to-market loss on the fair valuing the Company’s warrant investments. The difference between net earnings and adjusted net earnings in Q2 2019 related to the exclusion from adjusted net earnings of a $0.9 million ($0.8 million after income tax) mark-to-market loss on fair valuing the Company’s warrants and $0.8 million ($0.6 million after income tax) of severance costs.

Adjusted net earnings for YTD 2019 totaled $394.3 million ($1.88 per basic share), which compared to $177.6 million ($0.84 per basic share) for YTD 2018. The difference between net earnings and adjusted net earnings for YTD 2019 mainly reflected the exclusion from adjusted net earnings of a $2.3 million ($1.6 million after income tax) loss related to purchase price allocation adjustments on inventories, $1.2 million ($0.9 million after income tax) of severance costs, and $0.9 million ($0.8 million after income tax) of mark-to-market losses on the fair valuing of the Company’s warrants. The difference between adjusted net earnings and net earnings for YTD 2018 reflected the exclusion from adjusted net earnings of a $7.3 million ($6.4 million after income tax) mark-to-market loss on fair valuing the Company’s warrants, as well as the unfavourable impact of $5.4 million ($3.8 million after income tax) of purchase price allocation adjustments on inventories.

FULL-YEAR 2019 GUIDANCE

On December 11, 2018, Kirkland Lake Gold released full-year guidance for 2019 (see News Release dated December 11, 2018). Compared to the Company’s full-year 2018 results, the Company’s 2019 guidance included strong production growth, improved unit costs and a continued strong commitment to exploration and growth. Since December 11, 2018, there are have been two improvements to the Company’s full-year 2019 guidance, the first being included in the Company’s fourth quarter and full-year 2019 financial and operating results, issued on February 21, 2019, and the second being issued on May 7, 2019 as part of the Company's first quarter 2019 results. There were no revisions to guidance as part of the second quarter 2019 financial results, which were released on July 30, 2019. The Company's full-year 2019 guidance as at July 30, 2019, is provided in the table below.

Table 4. 2019 Guidance (as at July 30, 2019)(1)

| ($ millions unless otherwise stated) | Macassa | Holt Complex(2) | Fosterville | Consolidated |

| Gold production (kozs) | 240 - 250 | 140 - 150 | 570 - 610 | 950 - 1,000 |

| Operating cash costs/ounce sold ($/oz) (3) | $400 - $420 | $660 - $680 | $130 - $150 | $285 - $305 |

| AISC/ounce sold ($/oz) (3) | $520 - $560 | |||

| Operating cash costs (3) | $290 - $300 | |||

| Royalty costs | $25 - $30 | |||

| Sustaining and growth capital(3) | $150 - $170 | |||

| Growth capital(3)(4) | $155 - $165 | |||

| Exploration and evaluation(5) | $100 - $120 | |||

| Corporate G&A(6) | $26 - $28 |

- Full-year 2019 guidance as at July 30, 2019

- Production and operating cash cost guidance for the Holt Complex for full-year 2019 includes results for the Holloway mine, which resumed operations during Q1 2019, as one of three mines included in the Holt Complex.

- See the “Non-IFRS Measures” section of the MD&A for the three and nine months ending September 30, 2019. The most comparable IFRS Measure for operating cash costs is production costs, as presented in the Consolidated Statements of Operations and Comprehensive Income, and total additions and construction in progress for sustaining and growth capital. Operating cash costs per ounce and AISC per ounce sold are comparable to production costs on a unit basis. Operating cash costs, operating cash cost per ounce sold and AISC per ounce sold reflect an average US$ to C$ exchange rate of 1.33 and a US$ to A$ exchange rate of 1.41.

- Growth capital expenditure guidance for full-year 2019 excludes $19.8 million of capital expenditures related to the Macassa #4 shaft project, which are being recorded as capital expenditures in 2019, but were paid in cash on an advanced basis in 2018.

- Exploration and evaluation expenditures guidance for full-year 2019 include both expensed and capitalized exploration expenditures. All capitalized expenditures related to the Northern Territory are included in exploration and evaluation expenditures consistent with the advanced exploration program being carried out in the Northern Territory in 2019.

- Includes general and administrative costs and severance payments. Excludes non-cash share-based payment expense.

Effective Q1 2019, the Company combined the Holt, Holloway and Taylor mines into one segment, the Holt Complex, for the purpose of establishing and reporting performance against guidance. As a result, production, costs and expenditures for the Holt, Holloway and Taylor mines, all of which utilize the Holt Mill for processing, have been combined into one segment. Previously, production, costs and expenditures from these mines were reported separately, with processing costs allocated based on the proportion of production coming from each mine in each reporting period.

Table 5. YTD 2019 Results

| ($ millions unless otherwise stated) | Macassa | Holt Complex(2) | Fosterville | Consolidated |

| Gold production (kozs) | 184,918 | 82,483 | 427,472 | 694,873 |

| Operating cash costs/ounce sold ($/oz)(1) | $397 | $948 | $126 | $296 |

| AISC/ounce sold ($/oz)(1) | $584 | |||

| Operating cash costs (1) | $207.3 | |||

| Royalty costs | $25.4 | |||

| Sustaining capital(1) | $140.0 | |||

| Growth capital (excluding capitalized exploration)(1)(3) | $137.1 | |||

| Exploration (including capitalized exploration)(4) | $115.9 | |||

| Corporate G&A expense(5) | $26.3 |

- See the “Non-IFRS Measures” section of the MD&A for the three and nine months ended September 30, 2019. The most comparable IFRS Measure for operating cash costs is production costs, as presented in the Consolidated Statements of Operations and Comprehensive Income, and total additions and construction in progress for sustaining and growth capital. Operating cash costs per ounce and AISC per ounce sold are comparable to production costs on a unit basis. Operating cash costs, operating cash cost per ounce sold and AISC per ounce sold reflect an average US$ to C$ exchange rate of 1.32 and a US$ to A$ exchange rate of 1.43.

- Production, cost and expenditure results in YTD 2019 include results for the Holloway mine, which resumed operations during Q1 2019, as one of three mines included in the Holt Complex.

- Growth capital expenditures exclude $19.8 million of capital expenditures related to the Macassa #4 shaft project, which have been recorded as capital expenditures in YTD 2019, but were paid in cash on an advanced basis in 2018.

- Exploration and evaluation expenditures include both expensed and capitalized exploration expenditures. All capitalized expenditures related to the Northern Territory are being included in exploration and evaluation expenditures consistent with the advanced exploration program being carried out in the Northern Territory in 2019.

- Includes general and administrative costs and severance payments. Excludes non-cash share-based payment expense.

- Gold production for YTD 2019 totaled 694,873 ounces, a 41% increase from YTD 2018 driven by record production at both Fosterville and Macassa. The Company ended the first nine months of 2019 well positioned to achieve its improved full-year 2019 consolidated production guidance of 950,000 - 1,000,000 ounces of gold, with production at both Fosterville and the Holt Complex expected to increase in the fourth quarter from Q3 2019 levels. At Fosterville, production in the final quarter of 2019 is expected to increase from the 158,327 ounces produced in Q3 2019 due to continued improvement in average grades from production in the Swan Zone, with the mine remaining on track to easily achieve full-year 2019 guidance. Production at the Holt Complex is expected to increase in the fourth quarter, with higher levels of production compared to Q3 2019 expected to come from all three mines. Macassa ended YTD 2019 with production of 184,918 ounces, with the mine entering the final quarter of 2019 on track to achieve full-year 2019 guidance of 240,000 - 250,000 ounces.

- Production costs for YTD 2019 totaled $209.9 million. Operating cash costs for the first half of the year totaled $207.3 million, in line with target levels.

- Operating cash costs per ounce sold for YTD 2019 averaged $296, in line with full-year 2019 guidance of $285 - $305. For YTD 2019, both Fosterville and Macassa achieved operating cash costs per ounce sold better than the respective target ranges, in both cases due to higher than planned average grades. At Fosterville, operating cash costs per ounce sold averaged $126 compared to guidance of $130 - $150, while Macassa’s operating cash costs per ounce sold averaged $397 versus a target range of $400 - $420. Operating cash costs per ounce sold at the Holt Complex averaged $948, well above the target range of $660 - $680. While unit costs are expected to improve at the Holt Complex in the fourth quarter, the operation is not expected to achieve the full-year 2019 operating cash cost guidance as at July 30, 2019 (see section entitled “Revisions to Full-Year 2019 Guidance”).

- AISC per ounce sold for YTD 2019 averaged $584, above full-year 2019 guidance of $520 - $560, reflecting higher than planned sustaining capital expenditures at all three of the Company’s operations, mainly related to additional investments for capital development, equipment purchases and infrastructure projects, largely involving enhancements to milling facilities.

- Royalty costs for YTD 2019 totaled $25.4 million compared to full-year 2019 guidance of $25 - $30 million.

- Sustaining capital expenditures for YTD 2019 totaled $140.0 million and was tracking ahead of the existing full-year 2019 guidance of as at July 30, 2019 of $150 - $170 million. The level of sustaining capital expenditures during YTD 2019 reflected higher than planned sustaining capital expenditures at Macassa, Fosterville and the Holt Complex.

- Growth capital expenditures totalled $137.1 million for YTD 2019 (excluding capitalized exploration), which compared to full-year 2019 guidance of $155 - $165 million. Of total growth capital expenditures for YTD 2019, Macassa accounted for $91.1 million, with approximately $57.4 million relating to the #4 shaft project and the remainder largely funding a thickened tails project and the construction of a new tailings impoundment area. Fosterville accounted for $37.1 million of growth capital expenditures for YTD 2019, mainly related to the mine’s three key projects, including the new ventilation system, the paste fill plant and a new water treatment plant.

- Exploration and evaluation expenditures for YTD 2019 totaled $115.9 million (including capitalized exploration), which compared to full-year 2019 guidance of $100 - $120 million. Of total exploration expenditures, approximately $108.4 million were in Australia, including $82.0 million in the Northern Territory and $26.4 million at Fosterville. During Q3 2019, the Company continued to progress with advanced exploration work in the Northern Territory, including increasing underground development and drilling in support of a potential resumption of operations. Subsequent to the end of Q3 2019, the Company commenced test processing of Lantern Deposit material at the Union Reefs mill as part of the advanced exploration program. Drilling at Fosterville focused on underground drilling in the Lower Phoenix and Harrier systems, surface drilling at Robbin’s Hill, as well as exploration work at a number of regional targets. In Canada, exploration expenditures for YTD 2019 totaled $7.5 million and mainly focused on drilling at Macassa as well as regional exploration around the Holt Complex.

- Corporate G&A expense for YTD 2019 totaled $26.3 million compared to full-year 2019 guidance of $26 - $28 million.

REVISIONS TO FULL-YEAR 2019 GUIDANCE

Following completion of Q3 2019, the Company announced on November 6, 2019 a number of revisions to full-year 2019 guidance. The Company consolidated production and operating cash cost per ounce sold guidance for full-year 2019 remain unchanged as continued strong results at Fosterville and Macassa are expected to offset changes in production and operating cash cost per ounce sold guidance at the Holt Complex. Full-year 2019 production guidance at the Holt Complex was revised from 140,000 – 150,000 ounces to 120,000 – 130,000 ounces largely reflecting a slower than planned ramp up at the Holloway mine as well as lower than planned production levels at both Holt Mine and Taylor Mine for YTD 2019. Operating cash cost per ounce sold guidance for the Holt Complex was revised to $920 – $940 from $660 – $680 previously. On October 9, 2019, the Company announced that the future plans for the Holt Complex are currently under review.

The Company’s sustaining capital expenditure guidance has increased to $170 - $190 million from $150 - $170 million, with the increase mainly reflecting additional capital development at both Fosterville and Macassa, including new equipment and infrastructure enhancements. Growth capital expenditure guidance was increased from $155 - $165 million to $175 - $185 million, reflecting higher levels of investment at Macassa, primarily related to the #4 shaft project. At the #4 shaft, the Company has taken over from the general contractor and, as a result, has purchased the sinking plant and related equipment now as opposed to spreading these costs out over the life of the project. The project remains on track for phase 1 completion during the second quarter of 2022 at a capital cost of approximately $240 million. Full-year 2019 guidance for exploration and evaluation expenditures, including capitalized exploration expenditures, was increased to $120 - $140 million from $100 - $120 million, with the increase reflecting an acceleration of the advanced exploration program in the Northern Territory. Subsequent to the end of Q3 2019, the Company commenced test processing at the Union Reefs Mill, with plans to produce over 10,000 ounces before the end of 2019, with proceeds from gold sales to be accounted for as a reduction in capital. Results of this work could lead to a resumption of operations in the Northern Territory as early as the beginning of 2020. Full-year 2019 guidance for royalty costs was revised to $30 - $35 million from $25 - $30 million reflecting higher than planned sales and gold prices over the first nine months of the year. Corporate G&A cost guidance for full-year 2019 was revised to $30 - $35 million from $26 - $28 million previously. The Company’s guidance for full-year 2019 as at November 6, 2019 is provided below.

Table 6. 2019 Guidance (as at November 6, 2019)(1)

| ($ millions unless otherwise stated) | Macassa | Holt Complex(2) | Fosterville | Consolidated |

| Gold production (kozs) | 240 - 250 | 120 - 130 | 570 - 610 | 950 - 1,000 |

| Operating cash costs/ounce sold ($/oz) (3) | $400 - $420 | $920 - $940 | $130 - $150 | $285 - $305 |

| AISC/ounce sold ($/oz) (3) | $520 - $560 | |||

| Operating cash costs (3) | $290 - $300 | |||

| Royalty costs | $30 - $35 | |||

| Sustaining and growth capital(3) | $170 - $190 | |||

| Growth capital(3)(4) | $175 - $185 | |||

| Exploration and evaluation(5) | $120 - $140 | |||

| Corporate G&A(6) | $30 - $35 |

- Full-year 2019 guidance as at November 6, 2019

- Production and operating cash cost guidance for the Holt Complex for full-year 2019 includes results for the Holloway mine, which resumed operations during Q1 2019, as one of three mines included in the Holt Complex.

- See the “Non-IFRS Measures” section of the MD&A for the three and nine months ended September 30, 2019. The most comparable IFRS Measure for operating cash costs is production costs, as presented in the Consolidated Statements of Operations and Comprehensive Income, and total additions and construction in progress for sustaining and growth capital. Operating cash costs per ounce and AISC per ounce sold are comparable to production costs on a unit basis. Operating cash costs, operating cash cost per ounce sold and AISC per ounce sold reflect an average US$ to C$ exchange rate of 1.32 and a US$ to A$ exchange rate of 1.43.

- Growth capital expenditure guidance for full-year 2019 excludes $19.8 million of capital expenditures related to the Macassa #4 shaft project, which are being recorded as capital expenditures in 2019, but were paid in cash on an advanced basis in 2018.

- Exploration and evaluation expenditures guidance for full-year 2019 include both expensed and capitalized exploration expenditures. All capitalized expenditures related to the Northern Territory are included in exploration and evaluation expenditures consistent with the advanced exploration program being carried out in the Northern Territory in 2019.

- Includes general and administrative costs and severance payments. Excludes non-cash share-based payment expense.

Q3 2019 Financial Results and Conference Call Details

A conference call to discuss the Q3 2019 results will be held by senior management on Wednesday, November 6, 2019, at 4:00 pm ET (Thursday, November 7, 2019 at 8:00 am AEDT). Call-in information is provided below. The call will also be webcast and accessible on the Company’s website at www.klgold.com.

| DATE: | WEDNESDAY, NOV. 6, 2019 (ET), THURSDAY, NOV. 7, 2019 (AEDT) |

| CONFERENCE ID: | 2475217 |

| TIME: | 4:00 pm ET (8:00 am AEDT) |

| TOLL-FREE NUMBER: | (833) 241-7254 |

| INTERNATIONAL CALLERS: | (647) 689-4218 |

| AUSTRALIAN TOLL-FREE NUMBER | 1800287011 |

| AUSTRALIAN LOCAL NUMBER | 0283798020 |

Qualified Persons

Natasha Vaz, P.Eng., Vice President, Technical Services is a “qualified person” as defined in National Instrument 43-101 and has reviewed and approved disclosure of the technical information and data in this News Release.

About Kirkland Lake Gold Ltd.

Kirkland Lake Gold Ltd. is a growing gold producer operating in Canada and Australia that produced 723,701 ounces in 2018 and is on track to achieve significant production growth over the next three years, including target production of 950,000 – 1,000,000 ounces in 2019, 930,000 – 1,010,000 ounces in 2020 and 995,000 – 1,055,000 ounces in 2021. The production profile of the Company is anchored by two high-grade, low-cost operations, including the Macassa Mine located in Northern Ontario and the Fosterville Mine located in the state of Victoria, Australia. Kirkland Lake Gold's solid base of quality assets is complemented by district scale exploration potential, supported by a strong financial position with extensive management and operational expertise.

Non-IFRS Measures

The Company has included certain non-IFRS measures in this document, as discussed below. The Company believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the Company. The non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers. Please the Company’s MD&A for the three and nine months ended September 30, 2019 for a reconciliation of non-IFRS measures.

Free Cash Flow

In the gold mining industry, free cash flow is a common performance measure with no standardized meaning. The Company calculates free cash flow by deducting cash capital spending (capital expenditures for the period, net of expenditures paid through finance leases) from net cash provided by operating activities.

The Company discloses free cash flow as it believes the measure provides valuable assistance to investors and analysts in evaluating the Company’s ability to generate cash flow after capital investments and build the cash resources of the Company The most directly comparable measure prepared in accordance with IFRS is net cash provided by operating activities less net cash used in investing activities.

Operating Cash Costs and Operating Cash Costs per Ounce Sold

Operating cash costs and operating cash cost per tonne and per ounce sold are non-IFRS measures. In the gold mining industry, these metrics are common performance measures but do not have any standardized meaning under IFRS. Operating cash costs include mine site operating costs such as mining, processing and administration, but exclude royalty expenses, depreciation and depletion and share based payment expenses and reclamation costs. Operating cash cost per ounce sold is based on ounces sold and is calculated by dividing operating cash costs by volume of gold ounces sold.

The Company discloses operating cash costs and operating cash cost per tonne and per ounce as it believes the measures provide valuable assistance to investors and analysts in evaluating the Company’s operational performance and ability to generate cash flow. The most directly comparable measure prepared in accordance with IFRS is total production expenses. Operating cash costs and operating cash cost per ounce of gold should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS.

Sustaining and Growth Capital

Sustaining capital and growth capital are Non-IFRS measures. Sustaining capital is defined as capital required to maintain current operations at existing levels. Growth capital is defined as capital expenditures for major growth projects or enhancement capital for significant infrastructure improvements at existing operations. Both measurements are used by management to assess the effectiveness of investment programs.

AISC and AISC per Ounce Sold

AISC and AISC per ounce are Non-IFRS measures. These measures are intended to assist readers in evaluating the total costs of producing gold from current operations. While there is no standardized meaning across the industry for this measure, the Company’s definition conforms to the definition of AISC as set out by the World Gold Council in its guidance note dated June 27, 2013.

The Company defines AISC as the sum of operating costs (as defined and calculated above), royalty expenses, sustaining capital, corporate expenses and reclamation cost accretion related to current operations. Corporate expenses include general and administrative expenses, net of transaction related costs, severance expenses for management changes and interest income. AISC excludes growth capital, reclamation cost accretion not related to current operations, interest expense, debt repayment and taxes.

Total cash costs and AISC Reconciliation

The Company has not restated the 2018 AISC comparatives to reflect the impact of IFRS 16, Leases ("IFRS 16") consistent with the modified retrospective approach adopted by the Company for financial statement purposes upon transition to the new leasing standard effective January 1, 2019. If the Company had applied IFRS 16 in the comparative periods, it would not have resulted in a material impact to the 2018 consolidated or site-by-site AISC comparatives.

Average Realized Price per Ounce Sold

In the gold mining industry, average realized price per ounce sold is a common performance measure that does not have any standardized meaning. The most directly comparable measure prepared in accordance with IFRS is revenue from gold sales. Average realized price per ounces sold should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. The measure is intended to assist readers in evaluating the total revenues realized in a period from current operations.

Adjusted Net Earnings and Adjusted Net Earnings per Share

Adjusted net earnings and adjusted net earnings per share are used by management and investors to measure the underlying operating performance of the Company.

Adjusted net earnings is defined as net earnings adjusted to exclude the after-tax impact of specific items that are significant, but not reflective of the underlying operations of the Company, including transaction costs and executive severance payments, purchase price adjustments reflected in inventory and other non-recurring items. Adjusted net earnings per share is calculated using the weighted average number of shares outstanding for adjusted net earnings per share.

Earnings before Interest, Taxes, Depreciation, and Amortization (“EBITDA”)

EBITDA represents net earnings before interest, taxes, depreciation and amortization. EBITDA is an indicator of the Company’s ability to generate liquidity by producing operating cash flow to fund working capital needs, service debt obligations, and fund capital expenditures.

Working Capital

Working capital is a Non-IFRS measure. In the gold mining industry, working capital is a common measure of liquidity, but does not have any standardized meaning.

The most directly comparable measure prepared in accordance with IFRS is current assets and current liabilities. Working capital is calculated by deducting current liabilities from current assets. Working capital should not be considered in isolation or as a substitute from measures prepared in accordance with IFRS. The measure is intended to assist readers in evaluating the Company’s liquidity.

Risks and Uncertainties

The exploration, development and mining of mineral deposits involves significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. Kirkland Lake Gold is subject to several financial and operational risks that could have a significant impact on its cash flows and profitability. The most significant risks and uncertainties faced by the Company include: the price of gold; the uncertainty of production estimates (which assume accuracy of projected grade, recovery rates, and tonnage estimates and may be impacted by unscheduled maintenance, labour and other operating, engineering or technical difficulties with respect to the development of its projects, many of which may not be within the control of the Company), including the ability to extract anticipated tonnes and successfully realizing estimated grades; changes to operating and capital cost assumptions; the inherent risk associated with project development and permitting processes; the uncertainty of the mineral resources and their development into mineral reserves; the replacement of depleted reserves; foreign exchange risks; changes in applicable laws and regulations (including tax legislation); regulatory; tax matters and foreign mining tax regimes, as well as health, safety, environmental and cybersecurity risks. For more extensive discussion on risks and uncertainties refer to the “Risks and Uncertainties” section in the December 31, 2018 Annual Information Form and the Company’s MD&A for the period ended December 31, 2018 filed on SEDAR.

Cautionary Note Regarding Forward-Looking Information

Certain statements in this press release constitute ‘forward looking statements’, including statements regarding the plans, intentions, beliefs and current expectations of the Company with respect to the future business activities and operating performance of the Company. The words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” and similar expressions, as they relate to the Company, are intended to identify such forward-looking statements. Investors are cautioned that forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include, among others, the development of the Company’s properties and the anticipated timing thereof, expected production from, and the further potential of, the Company’s properties, the anticipated timing and commencement of exploration programs on various targets within the Company’s land holdings and the implication of such exploration programs (including but not limited to any potential decisions to proceed to commercial production), the ability to lower costs and gradually increase production, the ability of the Company to successfully achieve business objectives, the ability of the Company to achieve its longer-term outlook and the anticipated timing and results thereof, the performance of the Company’s equity investments and the ability of the Company to realize on its strategic goals with respect to such investments, the effects of unexpected costs, liabilities or delays, the potential benefits and synergies and expectations of other economic, business and or competitive factors, the Company's expectations in connection with the projects and exploration programs being met, the impact of general business and economic conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating gold prices, currency exchange rates (such as the Canadian dollar versus the US dollar), mark-to-market derivative variances, possible variations in ore grade or recovery rates, changes in accounting policies, changes in the Company's corporate mineral resources, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, the possibility of project cost overruns or unanticipated costs and expenses, higher prices for fuel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting time lines, risks related to information technology and cybersecurity, timing and costs associated with the design, procurement and construction of the Company’s various capital projects, including but not limited to the #4 Shaft project at the Macassa Mine, the ventilation, paste plant, transformer and water treatment facility at the Fosterville Mine, the ability to obtain the necessary permits in connection with all of its various capital projects, including but not limited to the the rehabilitation of the Macassa tailings facility and the development of a new tailings facility and the anticipated results associated therewith, the ability to obtain renewals of certain exploration licences in Australia, native and aboriginal heritage issues, risks relating to infrastructure, permitting and licenses, exploration and mining licences, government regulation of the mining industry, risks relating to foreign operations, uncertainty in the estimation and realization of mineral resources and mineral reserves, quality and marketability of mineral product, environmental regulation and reclamation obligations, risks relating to the Northern Territory wet season, risks relating to litigation, risks relating to applicable tax and potential reassessments thereon, risks relating to changes to tax law and regulations and the Company's interpretation thereof, foreign mining tax regimes and the potential impact of any changes to such foreign tax regimes, competition, currency fluctuations, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims, and limitations on insurance, as well as those risk factors discussed or referred to in the AIF of the Company for the year ended December 31, 2018 filed with the securities regulatory authorities in certain provinces of Canada and available at www.sedar.com. Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected. Although the Company has attempted to identify important risks, uncertainties and factors which could cause actual results to differ materially, there may be others that cause results not be as anticipated, estimated or intended. The Company does not intend, and does not assume any obligation, to update these forward-looking statements except as otherwise required by applicable law.

Mineral resources are not mineral reserves, and do not have demonstrated economic viability, but do have reasonable prospects for eventual economic extraction. Measured and indicated resources are sufficiently well defined to allow geological and grade continuity to be reasonably assumed and permit the application of technical and economic parameters in assessing the economic viability of the resource. Inferred resources are estimated on limited information not sufficient to verify geological and grade continuity or to allow technical and economic parameters to be applied. Inferred resources are too speculative geologically to have economic considerations applied to them to enable them to be categorized as mineral reserves. There is no certainty that Measured or Indicated mineral resources can be upgraded to mineral reserves through continued exploration and positive economic assessment.

Cautionary Note to U.S. Investors - Mineral Reserve and Resource Estimates

This press release has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101-Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”)-CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in SEC Industry Guide 7 under the United States Securities Act of 1993, as amended (the “Securities Act”).

Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this Management’s Discussion and Analysis contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

This document uses the terms “Measured”, “Indicated” and “Inferred” Resources. US investors are advised that while such terms are recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize them. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of pre-feasibility, feasibility or other economic studies. U.S. investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves. U.S. investors are also cautioned not to assume that all or any part of an Inferred Mineral Resource exists, or is economically or legally mineable.

FOR FURTHER INFORMATION PLEASE CONTACT

Anthony Makuch, President, Chief Executive Officer & Director

Phone: +1 416-840-7884

E-mail: tmakuch@klgold.com

Mark Utting, Vice-President, Investor Relations

Phone: +1 416-840-7884

E-mail: mutting@klgold.com

![]()

Revenue Q3 and YTD

Revenue Q3 and YTD

Op. Cash Costs and Gold Sales

Op. Cash Costs and Gold Sales

AISC Q3

AISC Q3

AISC YTD

AISC YTD

Basic EPS: Q3 2019 vs Q3 2018

Basic EPS: Q3 2019 vs Q3 2018

Basic EPS: Q3 2019 vs Q2 2019

Basic EPS: Q3 2019 vs Q2 2019

Basic EPS: YTD