Macarthur Minerals Second Quarter Update 2021 Macarthur Holding Firm on its Strategic Focus

VANCOUVER, British Columbia, July 29, 2021 (GLOBE NEWSWIRE) -- Macarthur Minerals Limited (TSXV: MMS) (ASX: MIO) (OTCQB: MMSDF) (the Company or Macarthur) is pleased to update shareholders on activities during the second quarter of 2021. It has been another active quarter in which the Company has been steadily progressing the foundational work required to underpin the delivery of its Feasibility Study for its high-grade magnetite the Lake Giles Iron Project in Western Australia, whilst at the same time continuing to advance the development of early revenue opportunities to take advantage of current strong iron ore prices. Progress on both of those fronts has been very encouraging, and as we enter the second half of 2021, the Company remains optimistic about delivery of both of these key milestones.

Key Areas of Focus for the 2021 Calendar Year

Macarthur’s primary areas of focus during calendar year 2021 include the following:

- Feasibility Study: Advancing the Feasibility Study for the Company’s high grade magnetite Lake Giles Iron Project in Western Australia.

- Repositioning of Pilbara Assets: Repositioning the Company’s non-iron ore Pilbara tenements to ensure an appropriate exploration and development focus can be maintained for lithium, base metals and gold.

- Early hematite production: Pursuing an early export opportunity for the Company’s hematite project at Ularring to take advantage of current high iron ore prices.

Summary of 2021 Second Quarter Highlights

Key highlights during the second quarter of 2021 included announcements on the following:

1. Early Revenue Generation

|

2021 Calendar Year Goals in Detail

Macarthur remains well placed to deliver on its stated 2021 goals. A more detailed summary of recent activities is set out below:

1. Early Revenue Generation:

- Ularring Hematite: The Company continues to advance an early production opportunity for the Ularring Hematite Project at Lake Giles in light of current strong demand and pricing for iron ore. The Company is actively working towards developing the lowest cost, end to end transport logistics solution that will sustain operations. Macarthur has made an application for a miscellaneous license covering 74 hectares adjacent to the Snark deposit, for non-process support infrastructure for the DSO operation. This would include facilities such as vehicle workshops, water storage, offices, fuel supply, stockpiles and product loadout. With mine planning work underway, the Company intends to lodge a mining proposal with the Department of Mines, Industry Regulation and Safety (DMIRS) during Q3-2021. To achieve an accelerated export opportunity, the Company will leverage previous studies undertaken on the Ularring Hematite Project that outlined an opportunity for direct shipping iron ore. The Company intends to make announcements on further progress with this strategy shortly.

- Mine-gate Sale Agreement with GWR: The company has secured a 400,000 tonne rail freight services agreement with Pacific National, with rolling stock expected to mobilize in Q1-2022. In addition, the Company has also entered into a term sheet for a 400,000 tonne DSO mine-gate purchase with GWR Group Limited (ASX: GWR). GWR’s flagship C4 iron ore mine in Wiluna began production earlier in 2021. Under the terms of the mine-gate purchase, MMS will purchase 400,000 tonnes of DSO fines and lump from GWR, with the agreement covering an initial two-year period with a two-year extension option. The MMS-GWR mine-gate purchase deal lines up perfectly with the Pacific National deal. Subject to securing matching port capacity at Esperance, the two deals provide the potential to develop a bridge of cash flow before Ularring comes online, it also provides optionality for physical or virtual blending with future DSO production from Ularring.

2. Feasibility Study for Lake Giles Iron Project:

- Following the onset of the Global Covid-19 pandemic early last year and throughout the balance of 2020, the Company has been steadily progressing the foundational work required to underpin the delivery of the study. Much of that work has focused on necessary background work to advance route to market concepts and delivery mechanisms.

- The Feasibility Study is on track for delivery this year, and with the combined technical capabilities and experience of Stantec’s team lead by Michael Wood and Macarthur’s highly experienced metallurgical consultant Dr Richard Peck and mining engineer Bernard Holtshousen. Stantec’s involvement in key areas will help bring the Feasibility Study in on time and within budget. The Company will continue to release regular updates on the Feasibility Study to ensure the market is kept fully informed on the study’s progress.

3. Repositioning of Non-Iron Ore Pilbara Assets:

- On 24 February 2021, Macarthur announced a repositioning the Company’s 100% owned, 720km² gold, copper, zinc, manganese and lithium exploration tenements in the Pilbara region of Western Australia. Following the announcement of that transaction, the Company completed the technical and valuation work on Macarthur’s Pilbara tenements and on a package of gold tenements in the Leonora region of Western Australia (which are currently under option by the Company with Zanil Pty Ltd).

- The Company is currently working to list a wholly owned subsidiary Macarthur Lithium Pty Ltd (to be renamed Infinity Mining Limited, subject to ASIC approvals) to unlock the value of the Company’s Pilbara assets via a separate listing on the ASX. The Company anticipates that a spin-out of the Pilbara tenements through an ASX listing has the potential to deliver a superior outcome for Macarthur and its shareholders. Earlier this year, reconnaissance exploration was undertaken across all Pilbara tenements to support the independent technical report required for a public listing. In addition, the Company also acquired project wide Advanced Spaceborne Thermal Emission and Reflection Radiometer (ASTER) data that complements existing ground and airborne geophysics for the Hillside project.

- Macarthur has completed its due diligence on the Central Goldfields gold assets and has commissioned an independent valuation. These 10 historic gold leases will form part of the proposed listing. A small drilling program is planned for the Great Northern tenement. Additionally, geological mapping and drill targeting will be undertaken at the historic Barlow’s Gully tenements to better understand the source of the surface gold that has been collected by prospectors across the lease.

Additional Goals in 2021

The Company will also focus on a series of complementary goals. These include:

- Strategic Partnerships: Formalising strategic partnerships for the key development and infrastructure requirements needed to commercialise the Lake Giles Iron Project remains a key focus for the Company this year and in the lead up to completion of the current Feasibility Study for the Company’s flagship magnetite project. Macarthur signed a Cooperation Agreement with diversified Singaporean-based conglomerate Jin Sung International Pte Ltd – 15 June 2021 and is in active discussions with a number of other global corporates that have the potential to add capital and technical capabilities to the project.

- Project Financing: With the active assistance of its financial advisers, the Company continues to advance terms for financing the development of the Company’s high grade magnetite project at Lake Giles to ensure a smooth pathway to the prompt closing of finance post-delivery of a successful Feasibility Study. The development of the financial model as part of the Feasibility Study will assist this pathway. The Company, together with its financial advisers and its study consultants have been working with FTI Consulting to ensure that this model is robust and sophisticated with built in sensitivities to ensure that it can provide adaptive outputs that will satisfy the requirements of conservative due diligence enquiries.

- Nevada Lithium Assets: The Company is actively examining the potential for strategic partnership(s) that can advance a programme of works to realise an improved value proposition for the Company’s 100% owned lithium brine claims in the Nevada region of the USA. Macarthur holds 210 lithium brine mining claims in Nevada, covering an area of 7 square miles (18 km2) located in Railroad Valley, in Nye County, Nevada, USA. The claims are located approximately 180 miles (300 km) North of Las Vegas, Nevada, and 330 miles (531 km) south east of Tesla’s Gigafactory.

- Graduation on to main board of TSX: The Company intends to progress its plans to migrate from the TSXV onto the main board of the TSX during the course of the year.

All of these stated goals have the potential to unlock unrealised value in the Company for the benefit of shareholders.

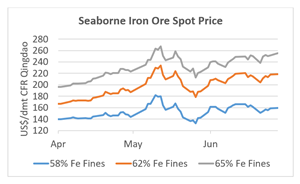

Iron Ore Market Overview

Current iron ore demand is all about China, and recent UBS economics forecasts have China’s GDP growth rate at 8.2% in 2021. UBS economics comments also pointed to this GDP growth being driven by domestic and export-focused production, with exports of finished products estimated to grow at 11-12% over the 2021 year.

Further, the steel industry is observing the collision of market growth and de-carbonisation for steel producers. If global CO2 emissions targets are to be met by 2050, then new capital investment in steel production must consider cleaner processes and ultimately transition away from traditional Blast Furnace process utilising coal as the reductant, towards scrap steel and DRI feed with hydrogen as the reductant.

On the commodity supply side, iron ore producers’ capacity investment decisions are tempered with the memory of, and looks back to, the “hot 2008“ market. At that time, high prices drove substantial capacity investment, only to be met with a sustained market demand slowdown where iron prices reached a low of USD38/Mt. Unlike the pricing for +62% Fe seen in 2008 and during the first 9 months of 2011, current prices do not appear to be tempered by the higher freight rates for cape size vessels that were seen during the 2008-2009 period.

Iron Ore Pricing Overview

UBS Research paper headed “How can China control commodity prices?” provides a commentary on China announced ban on steel export has been designed to put pressure on the demand from iron ore and forms another level of pressure in a continuing trade war with Australia. Impacts are potentially low cost of domestic steel prices in China and increased price of steel products into the rest of the world.

Let us look at history as an indication of the lag market impacts of iron ore prices over three distinct periods namely:

- 2007-2014 – above US$100/ton

- 2016-2020 – below US$80/ton

- 2020-2021 – above US$100/ton to US$227/ton

The pricing cycles (and you can assume the supply side response period) has been longer than one year, for example the first term was for 7 years and the down cycle was four years. In part, the 2007 cycle was sustained due to the economic stimulus by China and the rest of the world (ROW) given the Global Financial Crisis (GFC) in 2008. This last period (2020 to 2021) has been only a year and a new record spot price of US$232/ton was achieved for 62% FE iron delivery to Tianjin.

Chinese stockpile of imported iron ore at Chinese ports declined for four consecutive weeks to 123.95 Mt as of 25 June 2021, the lowest level in eight months (Tradingeconomics.com).

It is also important to take in the ROW response to COVID-19 and the Alex Owen Quantum Advisory “COVID-19 – a new Marshall Plan” article provides a perspective bench-marked to history. Post the second world war the Marshall Plan was introduced to refinance the reconstruction of Western Europe. This Plan, formerly known as the European Recovery Program, comprised US$12 billion in loans to nations across Western Europe with the aim to restart European economics engine. In today’s terms this would equate to US$128 billion.

In 1948 the Marshall Plan represented ~4% of GDP in the USA, but in response to the COVID-19 economic impacts the following fiscal and monetary stimulus responses from major economies include:

- US $3 trillion stimulus now represents in excess of 21% of USA GDP in 2019 (IMF/RBA)

- UK, the Bank of England has committed ~£300 billion of asset purchases and tax cuts representing ~14% of 2019 GDP (IMF/RBA)

- EU committing to €1.4 trillion in stimulus. (IMF/RBA)

This is a unique point in global history where on face value the global economic stimulus being provided to economies during the pandemic has, and continues to create, unprecedent demand for steel products in the form of Infrastructure development and therefore construction steel products. The premium for steel products may arguably result in increased direct investment in the ROW (excluding China) of new steel production capacity that has the eventual function of replacing older bast furnace steel technology needed by the mid-2030s to meet the strict C02 emissions standards announced in the Paris Accord and by Japan and the USA in 2020.

A figure accompanying this announcement is available at: https://www.globenewswire.com/NewsRoom/AttachmentNg/4ff8acaa-1cba-4a89-8409-903e56a4b490

Share Price

Both ASX and TSXV continue to demonstrate reasonably synchronised share price trading patterns for MIO and MMS. Although Macarthur’s share price has pulled back over second quarter, off the high that was reached after the announcement of the MOU with Southern Ports Authority, this may largely be reflective of market expectations regarding announced progress on both the Feasibility Study and anticipation of an announcement of a pathway to early DSO production. Shareholders can be assured that both objectives continue to be the subject of the highest focus by Management during 2021. Recent announcements have demonstrated progress on both fronts, resulting in an uptick of the share price during June and July 2021.

A summary of MIO/MMS trading activity from April to June 2021 is shown below:

A figure accompanying this announcement is available at: https://www.globenewswire.com/NewsRoom/AttachmentNg/83cfd6fb-d6a5-46f6-bdc8-a52798eea0a7

Andrew Bruton, Chief Executive Officer of Macarthur Minerals commented:

“The second quarter of 2021 has been an exceptionally active period for Management as it continues to put in place all of the building blocks for an exciting agenda of value-driving objectives.

Management has been undertaking a huge amount of ‘behind the scenes’ heavy lifting in order to systematically position the Company - not just to take advantage of the current commodity cycle as soon as possible, but to enable the Company to build a profitable and sustainable business over the next 20 years and beyond.

Whilst many shareholders may have expectations that all of this activity should be more visible, there is a logical sequencing to the steps that are being implemented for the sole purpose of ensuring that the Company’s ability to execute upon its strategic objectives is not compromised.

The fundamental value drivers for the Company are its massive 1.3 billion tonne high grade magnetite project, and its ability to target the development of additional early revenue earning hematite resources in the short term. These advantages demonstrate significant upside potential for Macarthur not only in the near term but for many decades to come.

Macarthur has big plans and it intends to accelerate into the second half of 2021. I look forward to providing the market with updates in the coming weeks and months as we move closer to our objective of delivering first revenues.”

On behalf of the Board of Directors, Mr. Cameron McCall, Chairman

For more information please contact:

Joe Phillips

Managing Director

+61 7 3221 1796

communications@macarthurminerals.com

| Investor Relations – Australia | Investor Relations - Canada |

| Advisir | Investor Cubed |

| Sarah Lenard, Partner | Neil Simon, CEO |

| sarah.lenard@advisir.com.au | +1 647 258 3310 |

| info@investor3.ca |

Company profile

Macarthur is an iron ore development, gold and lithium exploration company that is focused on bringing to production its Western Australia iron ore projects. The Lake Giles Iron Project mineral resources include the Ularring hematite resource (approved for development) comprising Indicated resources of 54.5 million tonnes at 47.2% Fe and Inferred resources of 26 million tonnes at 45.4% Fe; and the Lake Giles magnetite resource of 53.9 million tonnes (Measured), 218.7 million tonnes (Indicated) and 997 million tonnes (Inferred). The JORC reporting tables and Competent Person statement for the magnetite and hematite mineral resources have previously been disclosed in ASX market announcements dated 12 August 2020 and 5 December 2019. Macarthur has prominent (~721 square kilometer tenement area) gold, lithium and copper exploration interests in Pilbara region of Western Australia. In addition, Macarthur has lithium brine Claims in the emerging Railroad Valley region in Nevada, USA.

This news release is not for distribution to United States services or for dissemination in the United States

Caution Regarding Forward Looking Statements

Certain of the statements made and information contained in this press release may constitute forward-looking information and forward-looking statements (collectively, “forward-looking statements”) within the meaning of applicable securities laws. All statements herein, other than statements of historical fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future, including but not limited to statements regarding expected completion of the Feasibility Study; conversion of Mineral Resources to Mineral Reserves or the eventual mining of the Project, are forward-looking statements. The forward-looking statements in this press release reflect the current expectations, assumptions or beliefs of the Company based upon information currently available to the Company. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and no assurance can be given that these expectations will prove to be correct as actual results or developments may differ materially from those projected in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include but are not limited to: unforeseen technology changes that results in a reduction in iron or magnetite demand or substitution by other metals or materials; the discovery of new large low cost deposits of iron magnetite; the general level of global economic activity; failure to complete the FS; inability to demonstrate economic viability of Mineral Resources; and failure to obtain mining approvals. Readers are cautioned not to place undue reliance on forward-looking statements due to the inherent uncertainty thereof. Such statements relate to future events and expectations and, as such, involve known and unknown risks and uncertainties. The forward-looking statements contained in this press release are made as of the date of this press release and except as may otherwise be required pursuant to applicable laws, the Company does not assume any obligation to update or revise these forward-looking statements, whether as a result of new information, future events or otherwise.

![]()

Seaborne Iron ore spot price

Seaborne Iron ore spot price

MIO/MMS trading activity from April to June 2021