Newcrest Mining Limited - Red Chris Block Cave PFS Confirms Tier 1 Potential

- Confirms Red Chris potential to become a world class, long life mine

- Estimated 17% IRR and C$2.3 billion NPV over an initial 31 year mine life1,2,3

- Projected average 316kozpa gold and 80ktpa copper production from Macro Block 1 in FY29-341,2

- Impressive Block Cave Life-of-Mine All-In Sustaining Cost of -C$180/oz1,2,4

- Initial Ore Reserve estimate of 8.1Moz Au and 2.2Mt Cu5

- Further optimisation underway to assess opportunities proximate to the mining area, incl. East Ridge

- MB1 Feasibility Study expected to be completed in the second half of FY236

Melbourne, Australia--(Newsfile Corp. - October 11, 2021) - Newcrest Mining Limited (ASX: NCM) (TSX: NCM) (PNGX: NCM) is pleased to announce that the Newcrest Board has endorsed the Red Chris Block Cave Pre-Feasibility Study (the Study) and approved its progression to the Feasibility Stage.

The Study confirms Newcrest's original investment thesis of unlocking the underground portion of this Tier 1 deposit by leveraging Newcrest's industry-leading block caving expertise and developing the asset to become a mainstay of Newcrest's portfolio for decades to come.

The Study is the first technical report issued by Newcrest on Red Chris since its acquisition of a 70% interest and operatorship in August 2019. Newcrest intends to release a National Instrument 43-101 (NI 43-101) technical report on Red Chris within 45 days of this release.

Newcrest Managing Director and Chief Executive Officer, Sandeep Biswas, said "The Red Chris Block Cave Pre-Feasibility Study confirms Red Chris's potential to be a long life, low cost mine capable of producing a total of 5.3Moz of gold and 1.7Mt of copper at very attractive cash margins. The study highlights the quality of the deposit with a C$2.3 billion NPV and 17% IRR, but we believe captures only part of the longer term opportunity at Red Chris."

"Since acquiring our 70% interest in Red Chris in August 2019 we have been focused on unlocking its future potential, which we have always believed to be significant, and which is confirmed by the Study. To date, we have had considerable exploration success at Red Chris, including our exciting East Ridge discovery and the existence of multiple high grade pods in the East Zone, both of which are outside the scope of this Study. East Ridge is a new zone of higher grade mineralisation located outside the initial Mineral Resource estimate, with intercepts to date highlighting the potential for resource growth over time. We are currently evaluating 'early mining' options for the high grade pods in the East Zone with the aim of generating additional cash flows prior to the completion of block cave construction."

"Red Chris is already in a Tier 1 mining jurisdiction. We believe that we can transform the asset into a Tier 1 operation through the application of our proven industry-leading block caving technologies and, in doing so, provide attractive financial returns to shareholders as well as multi-generational employment and other opportunities in Tahltan territory and in British Columbia" said Mr Biswas.

Summary of Findings (in 100% terms)1,2,4

- Substantial low-cost gold and copper production growth in a Tier 1 jurisdiction:

- Total ore production of 406Mt producing 4.9Moz of gold and 1.5Mt of copper

- Average annual gold production of 158koz and copper production of 48.5kt over Life of Mine (LOM)

- Average annual gold production of 316koz and copper production of 80kt from Macro Block 1 (MB1) in FY29-34

- "Negative cost" gold production from the Red Chris Block Cave after accounting for copper credits, with an Average All-In Sustaining Cost (AISC) of C$-180/oz (US$-144/oz)

- Attractive investment returns:

- Estimated total capital expenditure of C$2.6 billion (US$2.1 billion)7 for the development of Macro Blocks (MB)1, 2 and 3, as well as process plant and infrastructure

- Internal Rate of Return (IRR)of 17% (real, after tax)

- ~31 year mine life at an average annual mill throughput rate of 12.8Mtpa

- Payback of 3.2 years8

- Net Present Value (NPV) of C$2.3 billion (US$1.8 billion)3

- Initial Ore Reserve estimate for Red Chris of 480Mt @ 0.52g/t Au and 0.45% Cu for 8.1Moz Au and 2.2Mt Cu5

- Considerable exploration success delivered to date, with the discovery of East Ridge and a new zone of higher grade mineralisation south west of the Main Zone, neither of which are included in the initial Mineral Resource and Ore Reserve estimates:

- High grade intercepts from East Ridge continue to expand the known mineralisation, supporting the potential for further Mineral Resource growth and additional mining fronts

- Pipeline of early stage targets within the surrounding exploration tenements

The Study builds on Newcrest's experience and success with block cave developments in Australia, with the block cave mining method particularly well suited to the porphyry deposits found at Red Chris and throughout the Golden Triangle region of British Columbia.

The Study underpins an initial Ore Reserve estimate of 8.1Moz Au and 2.2Mt Cu5. The Study and ongoing drilling results indicate significant orebody optionality which will be further tested during the Feasibility Stage. Parallel studies to assess further upside are underway to consider the 'early mining' of high grade pods located in the East Zone with the aim of generating additional cashflows prior to the completion of block cave construction, and accommodating the potential development of the new East Ridge discovery and further resource upside. Newcrest's experience at Cadia shows that orebodies of this type are unique and carry significant embedded optionality, providing opportunities for further value creation for shareholders over the mine life.

The availability of hydro-generated grid power combined with the efficient, low cost, block cave mining method is expected to reduce the project's carbon footprint compared to other mining methods.

The next major project milestone will be the Red Chris Block Cave Feasibility Study for the implementation of the first of three Macro mining Blocks, MB1, which is expected to be completed in the second half of FY236.

Table of Key Study Findings[9]

| Study Outcomes | ||||

| Area | Measure | Unit | Block Cave1,2 | LOM[10] |

| Production | Average ore milled / throughput (max) | Mtpa | 13.6 | 13.6 |

| LOM | Years | 31 | 36 | |

| Ore Mined: Ore Mined - Open Pit Ore Mined - Stockpile Ore Mined - Block Cave | Mt | 406 406 | 480 63 11 406 | |

| Average gold grade | g/t | 0.56 | 0.53 | |

| Average copper grade | % | 0.46 | 0.45 | |

| Gold produced | Moz | 4.9 | 5.3 | |

| Copper produced | Mt | 1.5 | 1.7 | |

| Average annual gold production | koz | 158 | 148 | |

| Average annual copper production | kt | 48.5 | 48.6 | |

| Capital | Project capital7 | C$m (real) | 2,632 | 2,758 |

| Operating | AISC | C$/oz sold | (180) | (60) |

| Economic assumptions | Gold price | US$/oz | 1,500 | 1,500 |

| Copper price | US$/lb | 3.30 | 3.30 | |

| CAD:USD exchange rate | 0.80 | 0.80 | ||

| Financials | NPV3 | C$m (real) | 2,283 | |

| IRR | % (real) | 17 | ||

| Payback period8 | Years | 3.2 | ||

| Free cash flow generation (post tax) | C$m (real) | 5,030 | ||

An indicative summary of key expected milestones is summarised as follows6:

| Red Chris Block Cave - Key Project Milestones | Date |

| Gating Feasibility Study to Execution | 2H FY23 |

| First Ore | 2H FY26 |

| First Production of Gold/Copper | FY27 |

Potential Exploration Upside

The Red Chris porphyry corridor has the potential to host multiple porphyry deposits as demonstrated by Newcrest's recent exploration success, including:

- Extending the known porphyry corridor 800m east of the Mineral Resource estimate

- Discovery of East Ridge, which contains the best drill results to date outside of the East Zone. East Ridge has the potential to increase the resource base and provide additional mining fronts

- A new higher grade zone has been discovered south west of the Main Zone that potentially could provide further mining optionality

- In addition, the Project contains a pipeline of early stage exploration targets within the surrounding exploration tenements and the nearby GJ property

Refer to the section titled "Potential Exploration Growth" on Page 14 for a summary of drill results.

Red Chris Block Cave Feasibility Study

The Red Chris Block Cave Feasibility Study for the implementation of MB1 is expected to be completed in the first half of CY236, with the study scope to include:

- Further optimisation of mill throughput rates, including for different resource growth scenarios

- Detailed block cave footprint design and scheduling focused on access infrastructure and MB1

- Material handling system detailed design, including crusher, conveyor, and associated project infrastructure to support the LOM

- Processing plant optimisation and detailed design at a Feasibility Study level

- Design of the MB1 Tailings Impoundment Area (TIA) to Feasibility Study level and refinement of the TIA design for MB2 and MB3

- Refinement and calibration of water balance and water quality models to enable better decision-making capabilities for the Project, and to mitigate impacts to the receiving environment

- Enhancing water resource stewardship through optimisation of processes to minimise consumption and maximise reuse

- Prioritised detailed design of the Operational Accommodation Complex to allow for early implementation

- Design of the surface infrastructure to Feasibility Study level of detail

- Further analysis and inclusion of next generation mining systems, including Single Pass Cave Establishment (SPCE) and the use of electric power to offset diesel in the mining process

- Finalisation of the contracting and procurement strategy for the Execution stage

- Consolidation of all costs and schedules into a Feasibility Study financial estimate

Project Description1

Newcrest is the operator of the Red Chris Mine (the Mine), which is owned 70% by Newcrest and 30% by Imperial Metals Corporation through an unincorporated joint venture. The Mine is currently an open pit operation that produces approximately 10 to 11Mt of ore per annum.

Newcrest completed an internal Concept Study in CY20 that identified the potential to transition to block cave underground mining and informed the need for an Early Works Program focusing on the construction of an Exploration Decline.

The Study commenced in June 2020 and has recommended transitioning the existing open pit to an underground mine using the block cave mining method. From the Exploration Decline, the Access Decline will be developed to provide personnel and material access to the mining blocks. A conveyor within an independent decline, fed by a jaw-gyratory crusher, would provide ore handling facilities as well as a second egress.

Three macro mining blocks (MB1, 2 and 3) would be mined sequentially using Load Haul Dump machines directly into the underground crusher in MB1 and MB2, while a truck loop would be added in time to haul ore from MB3 to the crusher in MB1. While the mine has been costed using a diesel fleet, the designs also allow for the electrification of the mining fleet as well as the use of automated equipment. Further studies on these applications are being progressed as part of the Feasibility Study.

The Study includes upgrades to the existing processing plant to treat underground ore at a throughput rate of 13.6Mtpa which would require an additional coarse ore stockpile, new SAG mill, additional rougher flotation capacity using StackCell technology, an upgraded regrind circuit, a new cleaner scalping Jameson Cell, and duplication of existing concentrate thickening and filtration equipment.

The Study also investigated an Upside Case to 15Mtpa which would require SAG mill configurations to allow increased throughput at a coarser grind. HydroFloat coarse particle flotation technology will be installed on the rougher tailings to maintain copper and gold recovery as the grind is coarsened.

Two key considerations of the Study have been the handling of tailings produced from mining as well as water stewardship. Studies to accommodate tailings storage have confirmed that tailings from MB1 can be accommodated within the already permitted TIA. For MB2 and MB3 a design has been undertaken to further raise the north and south TIA dams using centreline raises, replace reclaim dams and construct the northeast dam. This would provide an ultimate capacity of 550Mt tailings. Plans for the management of the tailings dam volume which will minimise the need for additional makeup water have also been developed.

Infrastructure to support the underground mine would include an Operational Accommodation Complex and services such as roads, water, sewage and communications. Power would be supplied through the existing transmission line with expansions to on-site facilities.

The Tahltan Nation is the First Nation on whose Territory the Red Chris Mine is situated. Newcrest has developed a strong working relationship with the Tahltan Nation and operates under an Impact, Benefit Co-Management Agreement (IBCA) with the Tahltan Nation. The Agreement includes provisions for royalties, education, training, employment, and contracting opportunities as well as how the two parties will work together on social, environmental and cultural heritage matters.

A range of engagement and consultation occurs regularly with Tahltan Central Government, Tahltan leadership, local communities and the larger Nation. Recently, engagement has been focused on upcoming permitting processes and related assessments.

Newcrest has identified a pathway to obtain the required regulatory approvals for the Project and is actively engaged with the Tahltan Central Government and government agencies in relation to the approvals required to enable execution of the Project in a phased manner.

This underground mine is envisioned to start production from MB1 in FY27 and have a mine life of approximately 30 years providing employment, revenue and other opportunities to Tahltan, British Columbia and Canada6.

Newcrest's initial Mineral Resource estimate was released in March 2021 and was used to support the Study. The Study has defined an initial Probable Ore Reserve of 480Mt @ 0.52 g/t gold and 0.45% copper for 8.1Moz contained gold and 2.2Mt contained copper, including an Open Pit Probable Ore Reserve of 75Mt @ 0.36 g/t gold and 0.42% copper for 0.86Moz contained gold and 0.31Mt contained copper, and an Underground Probable Ore Reserve of 410Mt @ 0.55 g/t gold and 0.45% copper for 7.2Moz contained gold and 1.8Mt contained copper5.

Indicative Production Profile1,10

The Study has defined an indicative consolidated profile utilising the most recent LOM Open Pit production profile for the ongoing Open Pit. The forecasted tonnage profile transitions from a predominantly Open Pit feed in FY26 to an exclusively underground mill feed in FY30 when the Project is envisioned to reach nameplate capacity of 13.6Mtpa. Existing lower grade stockpile material shall be used to supplement mill feed during the transition and to mitigate risk.

Figure 1 Indicative mill feed & grade profile

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_003full.jpg

Figure 2 Indicative gold, copper and gold equivalent production profile10,11

To view an enhanced version of Figure 2, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_004full.jpg

The Study also considered a production rate scenario of 15Mtpa which provides an option to increase the production rate of the block cave above the rate detailed in this document. This option will be further explored and refined during the Feasibility Study.

Underground Mine Development and Sequence1

The Red Chris underground resource extends to a depth of 1,200m below the surface with economic mineralisation typically being low grade and vertical in nature. Given the depth and nature of the mineralisation, the extraction of the resource is best suited to a bulk underground mining method. Block cave mining was selected due to its low operating cost, productivity and suitability to the geometry and conditions of the resource.

The underground mine will be accessed via both an access decline and a conveyor decline. The construction of the Exploration Decline is currently in progress which is expected to provide exploration information for the near mine area as well as provide the opportunity to collect more geological and geotechnical information for the planned caves. Mine access is expected to be completed in FY246.

The mine will consist of three adjoining Macro Blocks (MB1, MB2 & MB3, seen in Figure 4) each mined with a block cave strategy. The extraction level for all macro blocks will be at ~500mRL (~1,000m below surface) and the macro blocks are based on the El Teniente layout with 32m by 20m drawbell spacing. The ore mined during caving of MB1 and MB2 will be moved to a central, 5-tipple crusher with large underground loaders. The crusher is located at the northeast corner of the footprint to facilitate mining of MB1 and MB2. Ore mined during caving of MB3 will be loaded onto 40t trucks and hauled to the crusher. The crusher will then feed the inclined conveyor that will bring the ore to the surface coarse ore stockpile. The sequence of the extraction will be the numerical order of the three macro blocks. This sequence is based on grade and geotechnical considerations. First production from MB1 is expected in FY27 and production is expected to be completed in FY576.

The underground mine ventilation network will consist of three surface connecting raises and the two declines. The conveyor decline, access decline and VR1 (5.5m diameter) will be intakes and VR2 (5.5m diameter) and VR3 (4.5m diameter) will be exhaust. The ventilation network is a pull system that has the fans located on the exhaust raises. The system will have heaters on the intakes to maintain the underground air temperature above freezing. The system was designed to be expanded based on air flow demand, which peaks at approximately 700 m3/s during peak demand.

The mine design also includes the following infrastructure:

- Primary ventilation network including fans, doors and barricades

- Underground workshop, offices, refuge stations

- Dewatering facilities to handle snow melt and spring freshet with a maximum inflow of 1,500m3/h (1 in 50 year event) after the cave reaches the surface

- Utility and fire water distribution

- Electrical power supply and distribution

- Diesel fuel supply and distribution

- Concrete supply and distribution

| Area | Start Construction | First Production6 | Ore (Mt)2 |

| Exploration Decline | In Progress | - | - |

| Access & Conveyor Decline | FY23 | - | - |

| MB1 | FY24 | FY27 | 156 |

| MB2 | FY36 | FY36 | 76 |

| MB3 | FY40 | FY41 | 173 |

| Production Complete | FY57 | - | - |

Figure 3 Mine design looking south

To view an enhanced version of Figure 3, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_005full.jpg

Figure 4 Top view showing the location of MB1, MB2 and MB3 in relation to other infrastructure

To view an enhanced version of Figure 4, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_006full.jpg

Indicative Mine Production Profile1,10

| Year | Ore Source | Total Material Movement (Mt) | Plant Feed (Mt) | Average Gold Grade (g/t) | Average Copper Grade (%) | |

| FY22 - 26 | Open Pit, Stockpile | ~222 | ~54 | 0.42 | 0.48 | |

| FY27 - 29 | Stockpile, MB1 | ~45 | ~39 | 0.66 | 0.48 | |

| FY30 - 35 | MB1 | ~82 | ~82 | 0.94 | 0.68 | |

| FY36 - 39 | MB1, MB2 | ~59 | ~54 | 0.45 | 0.45 | |

| FY40 - 41 | MB1, MB2, MB3 | ~28 | ~27 | 0.34 | 0.35 | |

| FY42 - 48 | MB2, MB3 | ~100 | ~95 | 0.38 | 0.34 | |

| FY49 - 57 | MB3 | ~120 | ~120 | 0.46 | 0.39 | |

Estimated project capital expenditure profile1,4,7,9

| FY22 | FY23 | FY24 | FY25 | FY26 | FY27 | FY28 | FY29 | FY30+ | Total | |

| MB1 Capital Expenditure (C$m) | 76 | 354 | 417 | 515 | 338 | 152 | 40 | - | - | 1,893 |

| MB2 Capital Expenditure (C$m) | - | - | - | - | - | - | - | - | 240 | 240 |

| MB3 Capital Expenditure (C$m) | - | - | - | - | - | - | - | - | 499 | 499 |

| Total Project Capital Expenditure (C$m) | 76 | 354 | 417 | 515 | 338 | 152 | 40 | - | 739 | 2,632 |

| Total Project Capital Expenditure (US$m) | 61 | 283 | 334 | 412 | 271 | 122 | 32 | - | 591 | 2,106 |

Metal Price and Exchange Rate Sensitivity Analysis1,2,4,9

The actual IRR of the Project will vary according to the copper and gold prices realised. Base case assumptions for the Study were a gold price of US$1,500/oz, copper price of US$3.30/lb, and a CAD:USD exchange rate of 0.80.

The table below outlines how the estimated Central Case Project IRR of 17% varies using different price assumptions:

| Scenario | Assumption | IRR |

| Gold price (US$/oz) | 1,200 | 15% |

| 1,800 | 19% | |

| Copper price (US$/lb) | 2.60 | 15% |

| 4.00 | 20% | |

| CAD:USD | 0.77 | 18% |

| 0.83 | 17% |

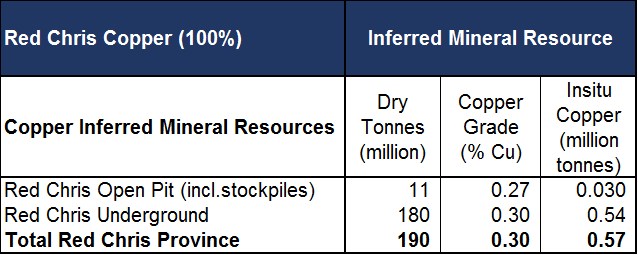

Red Chris Mineral Resource12

The Red Chris Mineral Resource has been updated for mining depletion to 30 June 2021 from that reported in the release titled "Newcrest announces its initial Mineral Resource estimate for Red Chris" dated 31 March 2021. All other assumptions remain unchanged. A summary of material assumptions is included in Appendix 1 JORC Table 1. Mineral Resources are reported inclusive of Ore Reserves. Mineral Resources that are not Ore Reserves do not have demonstrated economic viability.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_007full.jpg

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_008full.jpg

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_009full.jpg

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_010full.jpg

Red Chris Ore Reserve13

A summary of material assumptions is provided below and included in Appendix 1 JORC Table 1. There are no material differences between the definitions of Probable Ore Reserves under the 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves and the equivalent definitions in the JORC Code.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_011full.jpg

Material Assumptions for Ore Reserves

Red Chris is an operating open pit mining both the East and Main Zone resources. The underground reserves are based on transitioning from open pit to underground mining of the East Zone resource at depth. The Ore Reserves are supported by the Study. The Project is progressing to the Feasibility Stage. If required any adjustments to the Ore Reserves statements will be made at the completion of the Feasibility Study.

Ore Reserve Classification

The Probable Ore Reserve is based on Indicated Mineral Resources and diluting material. Diluting material is either low grade Indicated Mineral Resource or material carrying no grade. No Measured Mineral Resources are stated for this deposit. The resource classification is based on an assessment of geological confidence as a function of geological and mineralisation continuity.

Mining Method

Various mining methods have been considered for the extraction of the East Zone resources. Based on the depth, size, grade and existing site production rate block caving has been deemed the most appropriate mining method by the Study and supported via independent reviews. Ongoing data collection and geotechnical and mining studies will provide ongoing design parameters for the Project.

Ore Processing

Processing of the Red Chris Underground ore stream will be through the Red Chris Concentrator, which will be upgraded to accommodate a combination of larger throughput, increased hardness and higher gold and copper head grades. The upgraded plant will utilise grinding and flotation to produce a copper-gold concentrate using similar unit operations to the current plant. A parallel single-stage SAG (SSAG) grinding circuit will be installed, with a dedicated coarse ore stockpile. Underground ore will be divided between the existing grinding circuit and the new SSAG circuit at a ratio of approximately 60:40. The combined throughput of the upgraded plant will be 13.6 Mtpa. Additional rougher and cleaner flotation capacity, a new regrind circuit, and expanded concentrate dewatering equipment and concentrate load-out facility are also included in the plant upgrade. The application of coarse particle flotation has also been considered for moderate future throughput expansion, and the selection of a SSAG enables further expansion through addition of a ball mill in the future.

Metallurgical testwork, plant design and capital and operating cost estimation were completed to Pre-Feasibility level of accuracy.

Metallurgical testing on a range of underground samples provided data to size the single-stage SAG mill and estimate copper and gold recoveries attributable to underground ore. The anticipated recoveries for underground ore are

81 to 86% for copper and 60 to 75% for gold across the life of the project. Test samples focused mostly on the first 15 years of underground production but included some material from the remainder of the anticipated mine life. The mineralogy of underground samples was found to be more favourable for gold recovery than for current Red Chris open pit operations. Underground ore mineralogy was shown to have some upside for producing high copper concentrate grades due to the presence of enriched copper minerals such as bornite in certain zones in the orebody.

Cut-Off Grade

The Red Chris Ore Reserve employs a value-based cut-off determined from the Net Smelter Return (NSR) value equal to the site operating cost derived from the Study. The NSR calculation takes into account Ore Reserve revenue factors, metallurgical recovery assumptions, transport costs, refining charges, and royalty charges. The site operating costs include mining cost, processing cost, relevant site general & administration costs and relevant sustaining capital costs. This results in shut off values for each block as follows: MB1 = C$22.00/t Milled, MB2 and MB3 C$22.80/t Milled.

Estimation Methodology

Capital cost estimation for the project has been based on a blend of material take-offs and factored quantities with semi-detailed unit costs targeting a Class 4 Capital Cost per Association for the Advancement of Cost Engineering International (AACEI) guidelines and an accuracy range ± 25%.

The Operating Cost estimate has been compiled to an accuracy of +/-25%.

Contingency has been calculated and applied to the Capital Cost estimate. No contingency has been applied to the Operating Cost estimate.

All inputs are in Canadian Dollars.

Material Modifying Factors

All development has mining factors for dilution and mining recovery applied to accurately represent the expected mined tonnes. PCBC™ software is used for cave production scheduling and estimation of grade for material drawn from the block caves. The resource estimate includes internal dilution, and external dilution is included as part of the draw model, with no mining recovery factors applied to the Ore Reserve estimate. Red Chris has no block cave operational data supporting the assumptions within the PCBC™. The parameters are based on deposits and operations of similar properties providing confidence in the applicability. These parameters have been independently reviewed and found to be suitable to support the Ore Reserves.

Other Modifying Factors

Management of water resources was a primary focus of the Study and involved the creation of a water balance model for Study decision-making and to support environmental studies. The results of the water balance indicate that the demands for water for the Block Cave Project, which result from the increase in production rates over current practice, can be achieved by applying water management processes, largely aimed at improving reclaim and recycling of water.

The permitting plan proposes a staged approach to permitting, appropriate to the long-term nature of the Project. The Energy, Mines & Low Carbon Innovation, Environmental Assessment Office and Tahltan Central Government through its representatives have been consulted by Newcrest on the permit applications submitted by Newcrest to date. Newcrest will continue to engage and consult with the Tahltan Central Government and government agencies on the development of the permitting plan and applications for the Project. The timing of obtaining the authorisations remains a risk to the Project and is being actively managed through engagement with the relevant parties. The permitting process has been informed by engagement of independent experts in British Columbian permitting. Obtaining permits to extract the reserves using the block cave mining method has sufficient confidence to support the reserves statement.

The known legal, political, environmental or other risks that could materially affect the potential development of the mineral resources or ore reserves are identified in Sections 3 and 4 of Appendix 1.

Potential Exploration Growth

East Ridge is a new discovery located 300m to the east of East Zone and is located outside of Newcrest's initial Mineral Resource estimate. Drilling to date has demonstrated continuity of the East Ridge zone (>1g/t AuEq[14]) over dimensions of 400m high, 400m long and 125m wide, with the higher grade (>2g/t AuEq14) over 300m high, 300m long and 100m wide. Mineralisation is open to the east and at depth and extends the eastern dimensions of the porphyry corridor. Drilling to define the extent of the East Ridge mineralisation is ongoing and has the potential to deliver additional resource growth over time. Significant intercepts include15:

- RC705

- 254m @ 1.0g/t Au & 1.1% Cu from 718m

- including 182m @ 1.3g/t Au & 1.3% Cu from 764m

- including 80m @ 1.6g/t Au & 1.4% Cu from 852m

- RC688:

- 344m @ 0.70g/t Au & 0.75% Cu from 776m

- including 170m @ 1.1g/t Au & 1.1% Cu from 892m

- including 78m @ 1.1g/t Au & 1.3% Cu from 894m

- RC700:

- 366m @ 1.1g/t Au & 0.93% Cu from 738m

- including 226m @ 1.6g/t Au & 1.3% Cu from 774m

- including 146m @ 2.1g/t Au & 1.6% Cu from 780m

- RC678:

- 198m @ 0.89g/t Au & 0.83% Cu from 800m

- including 104m @ 1.5g/t Au & 1.3% Cu from 884m

- including 76m @ 1.8g/t Au & 1.5% Cu from 908m

Figure 5 Oblique schematic section view of the Red Chris porphyry corridor showing gold distribution. 0.5 g/t Au, 1g/t Au,1g/t AuEq and 2g/t AuEq shell projections generated from the LeapfrogTM model14.

To view an enhanced version of Figure 5, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_012full.jpg

Step out drilling at East Ridge has highlighted the potential to extend the porphyry corridor to the east of Newcrest's present drilling, with RC701 drilled 700m east of East Ridge returning 206m @ 0.2g/t Au & 0.49% Cu from 1,816m. This intercept is one of the deepest on the property with no drilling between this hole and East Ridge. Follow up drilling is planned to assess this area for additional higher grade zones.

Figure 6 Schematic plan view map of the Red Chris porphyry corridor spanning East Ridge, East Zone, Main Zone and Gully Zone showing drill hole locations (Newcrest & Imperial) and significant Newcrest intercepts15. 0.5 g/t Au,1 g/t Au, 1 g/t AuEq and 2g/t AuEq shell projections generated from a LeapfrogTM model14.

To view an enhanced version of Figure 6, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_013full.jpg

At the Main Zone, drilling has confirmed the potential for further higher grade mineralisation which could support additional mining fronts, beneath and to the south west of the open pit. The mineralisation is located within the Mineral Resource estimate. Drilling to define the extent and continuity of this higher grade mineralisation is ongoing. Significant Results include15:

- RC666:

- 194m @ 0.62g/t Au & 0.46% Cu from 476m

- including 76m @ 1.2g/t Au & 0.75% Cu from 592m

- including 62m @ 1.4g/t Au & 0.78% Cu from 604m

- RC679:

- 456m @ 0.37g/t Au & 0.42% Cu from 418m

- including 98m @ 0.71g/t Au & 1.0% Cu from 440m

- RC683:

- 300m @ 0.41g/t Au & 0.51% Cu from 260m

- including 114m @ 0.67g/t Au & 0.85% Cu from 390m

- including 22m @ 1.1g/t Au & 1.4% Cu from 464m

Figure 7 Long section view map of the Red Chris porphyry corridor showing drill hole locations and gold distribution.

To view an enhanced version of Figure 7, please visit:

https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_014full.jpg

Further drilling is also planned to assess the Gully Zone for additional higher grade zones in the western extents of the porphyry corridor, while regionally exploration will focus on identifying new porphyry centres within the wider tenement areas.

Appendix 1

JORC Table 1 - Red Chris (70% Newcrest)

Section 1: Sampling Techniques and Data

| Criteria | Commentary |

| Sampling techniques | All samples are obtained from core drilling. Diamond core sizes range from PQ, HQ, NQ, and BQ for some older shallow drilling. PQ, HQ and NQ diameter diamond core was drilled on a 3m, or 6m runs. Core was cut using either a manual or automatic core-cutter and half core sampled at either 2m or 2.5m intervals. Some older shallow drilling was sampled at 10 foot intervals from manually split core. All historical sampling used in the Mineral Resource estimate is considered to have been collected by acceptable practices. |

| Drilling techniques | All drilling undertaken at Red Chris is diamond core ranging in diameter configuration from PQ3, HQ3, NQ2, and BQ2. Shallow areas of older BQ core size have now been mined, with all deeper drilling undertaken by Imperial Metals or Newcrest. Newcrest core from inclined drill holes are oriented on 3m or 6m runs using an electronic core orientation tool (Reflex ACTIII). At the end of each run, the bottom of hole position is marked by the driller, which is later transferred to the whole drill core run length with a bottom of hole reference line. Historical core from inclined drill holes and vertical drill holes were not oriented. |

| Drill sample recovery | Core recovery is systematically recorded from the commencement of coring to end of hole, by reconciling against driller's depth blocks in each core tray with data recorded in the database. Drillers depth blocks provided the depth, interval of core recovered, and interval of core drilled. Core recoveries were typically 100%, with isolated zones of lower recovery. |

| Logging | Geological logging recorded qualitative descriptions of lithology, alteration, mineralisation, veining, and structure for all core drilled. Geotechnical measurements were recorded including Rock Quality Designation (RQD) fracture frequency, solid core recovery and qualitative rock strength measurements. Magnetic susceptibility measurements were recorded every metre by Newcrest and Imperial Metals. All geological and geotechnical logging was conducted at the Red Chris site. Digital data logging is now captured, validated, and stored in an acQuire database. Imperial Metals logging data was recorded into a Lagger database and has been transferred into acQuire. All historical logging data was transferred into acQuire. All drill cores were photographed, prior to cutting and/or sampling the core. The logging is of sufficient quality to support the Mineral Resource estimate. |

| Sub-sampling techniques and sample preparation | Sampling, sample preparation and quality control protocols are considered appropriate for the material being sampled. Core was cut or split and sampled at the Red Chris site core processing facility that was established by each of the various operators. Half core samples were collected in either plastic or poly-ore bags together with pre-numbered sample tags and grouped in plastic bags and strapped for dispatch to the laboratory. Sample weights typically varied from 5 to 10kg. Sample sizes are considered appropriate for the style of mineralisation. Drill core samples were freighted by road to the various laboratories used by each of the operators via secure transport. Chain of Custody management was achieved through solid boxing of samples with tamper proof tags. Sample preparation for Newcrest samples was conducted at the independent ISO 9001 certified and ISO 17025 accredited Bureau Veritas Commodities Canada Ltd Laboratory, Vancouver (Bureau Veritas). Samples were dried at 650C, and crushed to 95% passing 4.75 mm, and the split to obtain up to 1kg sub-sample, which was pulverised (using LM2) to produce a pulped product with the minimum standard of 95% passing 106μm. Duplicate samples were collected from crush and pulp samples at a rate of 1:20. Duplicate results show an acceptable level of variability for the material sampled and style of mineralisation. Periodic size checks (1:20) for crush and pulp samples and sample weights are provided by the laboratory and recorded in the acQuire database. Sample preparation for historical samples was conducted by various independent preparation labs in Smithers. Samples were dried, crushed to 4-5 mm, and then split to obtain a sub-sample, which was pulverised in a ring pulveriser to produce a pulped product with the minimum standard of either 85% passing 75μm or 95% passing 105μm. The sample pulps were then dispatched to the parent laboratories in Vancouver for analysis. |

| Quality of assay data and laboratory tests | Assaying of Newcrest drill core samples was conducted at Bureau Veritas. All samples were assayed for 59 elements using a 4-acid digestion followed by ICP-ES/ICP-MS determination (method MA250). Gold analyses were determined by 50g fire assay with ICP-ES finish (method FA350). Carbon and Sulphur were determined by Leco (method TC000) and mercury using aqua regia digestion followed by ICP-ES/MS determination (method AQ200). Assaying of historical drill core samples was conducted at various independent ISO 9001 certified laboratories in Vancouver. All samples were assayed for gold via fire assay fusion by ICP-ES on 30g samples. All samples were analysed for copper by ICP-ES or AAS with an aqua regia digestion. Additional analysis was undertaken by Imperial Metals with pulps analysed via ICP-MS with an aqua regia digestion for a 36 element suite. Sampling and assaying quality control procedures consisted of inclusion of certified reference material (CRMs), coarse residue and pulp duplicates with each batch (at least 1:20). Assays of quality control samples were compared with reference samples and verified as acceptable prior to use of data from analysed batches. Laboratory quality control data, including laboratory standards, blanks, duplicates, repeats and grind size results are currently captured in acQuire database and assessed for accuracy and precision for recent data. Imperial Metals quality control data has been imported into acQuire, whilst historical quality control data was reviewed from numerous technical reports. Samples have been periodically resubmitted to the primary laboratory and sent to a secondary laboratory. Analysis of the available quality control sample assay results indicates that an acceptable level of accuracy and precision has been achieved and the database contains no analytical data that has been numerically manipulated. The assaying techniques and quality control protocols used are considered appropriate for the data to be used for estimation of Mineral Resources. |

| Verification of sampling and assaying | Sampling intervals defined by the geologist are electronically assigned sample identification numbers prior to core cutting. Corresponding sample numbers matching pre-labelled sample tags are assigned to each interval. All sampling and assay information are currently stored in a secure acQuire database with restricted access. Currently electronically generated sample submission forms providing the sample identification number accompany each submission to the laboratory. Assay results from the laboratory with corresponding sample identification are loaded directly into the acQuire database. No adjustments are made to assay data, and no twinned holes have been completed. Drilling intersects mineralisation at various angles. Historical sampling and assaying has been verified via the 5 years of production reconciliation from the current open pit operations. There are no currently known drilling, sampling, recovery, or other factors that could materially affect the accuracy or reliability of the data. |

| Location of data points | Newcrest drill collar locations were surveyed using a RTK GPS with GNSS with a stated accuracy of +/- 0.025m. Drill rig alignment was attained using an electronic azimuth aligner (Reflex TN14 GYROCOMPASS). Downhole survey was collected at 9 to 30m intervals of the drill hole using single shot survey (Reflex EZ-SHOT). At the end of hole, all holes have been surveyed using a continuous gyro survey to surface (Reflex EZ-GYRO). Historical drill collar locations were surveyed using either total station instrument tied into established property grid control, a survey quality GPS, or a handheld Garmin GPS with accuracy of +/- 3m. Downhole survey was collected at 9m intervals of the drill hole using various single shot Reflex survey methods. Topographic control is established from PhotoSat topographic data and derived digital elevation model. The topography is generally low relief to flat, with an average elevation of 1500 m, with several deep creek gullies. All collar coordinates are provided in the North American Datum (NAD83 Zone 9). |

| Data spacing and distribution | Drill hole spacing varies through the deposit, with the overall drill hole spacing ranging from 50 x 50m within the East Zone up to 100 x 200m in the Gully Zone. Both historical and recent Newcrest drilling intersects the mineralisation at various angles. The data spacing and distribution of drill holes is considered sufficient to define both the geological and grade continuity for the porphyry style mineralisation and to support the Mineral Resource estimate. Geological and grade continuity has been demonstrated during the 5 years of production from the current open pit operations. |

| Orientation of data in relation to geological structure | Newcrest drilling is oriented perpendicular to the intrusive complex. The intrusive complex has an east-northeast orientation, with drilling established on a north-northwest orientation. Historical drilling is oriented predominantly north-south along grid or are vertical. Drill holes exploring the extents of the East Ridge, East Zone, Main Zone and Gully Zone mineral system intersected moderately dipping volcanic and sedimentary units cut by sub-vertical intrusive lithologies. Steeply dipping mineralised zones with an east-northeast orientation have been interpreted from historic and Newcrest drill holes. |

| Sample security | Chain of Custody management has been achieved by all operators through solid boxing of samples with tamper proof tags. The current security of samples is controlled by tracking samples from drill rig to database. Drill core was delivered from the drill rig to the Red Chris site core yard every shift. Geological and geotechnical logging, high resolution core photography and cutting of drill core was undertaken at the Red Chris core processing facility. Samples were freighted in sealed bags with security tags by road to the laboratory, and in the custody of Newcrest representatives. Historical samples were freighted by road to the various laboratories used by each of the operators via secure packaging and transport. Sample numbers have been generated from pre-labelled sample tags. All samples are collected in pre-numbered plastic bags. Sample tags are inserted into prenumbered plastic bags together with the sample. Verification of sample numbers and identification is conducted by the laboratory on receipt of samples, and sample receipt advice is currently issued to Newcrest. Details of all sample movement are now recorded in a database table. Dates, Hole ID sample ranges, and the analytical suite requested are recorded with the dispatch of samples to the laboratory analytical services. Any discrepancies logged at the receipt of samples into the laboratory analytical services are validated. |

| Audits or reviews | Internal verification and audit of Newcrest exploration procedures and databases are periodically undertaken. Reviews of assay laboratories are conducted on a regular basis by both project personnel and owner representatives. Historical data has been validated against public domain reports and is currently being digitally recaptured. In the Competent Persons opinion the sample preparation, security, and analytical procedures are consistent with current industry standards and are entirely appropriate and acceptable for the styles of mineralisation identified and is appropriate for use in Mineral Resource estimates. There are no identified drilling, sampling or recovery factors that materially impact the adequacy and reliability of the results of the drilling programmes. |

Section 2: Reporting of Exploration Results

| Criteria | Commentary |

| Mineral tenement and land tenure status | Red Chris comprises 77 mineral tenures including five mining leases and is a joint venture between subsidiaries of Newcrest Mining Limited (70%) and Imperial Metals Corporation (30%). Newcrest Red Chris Mining Limited is the operator of Red Chris. Newcrest Red Chris Mining Limited and the Tahltan Nation (as represented by the Tahltan Central Government, the Tahltan Band and Iskut First Nation) signed an amended and restated IBCA covering Red Chris on 15 August 2019. All obligations with respect to legislative requirements including minimum expenditure are maintained in good standing. |

| Exploration done by other parties | Conwest Exploration Limited, Great Plains Development Co. of Canada, Silver Standard Mines Ltd, Texasgulf Canada Ltd. (formerly Ecstall Mining Limited), American Bullion Minerals Ltd and bcMetals Corporation conducted exploration in the areas between 1956 and 2006. Imperial Metals Corporation acquired the project in 2007 and completed deeper drilling at the East and Main Zones between 2007 and 2012. |

| Geology | The Red Chris Project is located in the Stikine terrane of north-western British Columbia, 80 km south of the town of Dease Lake. Late Triassic sedimentary and volcanic rocks of the Stuhini Group host a series of Late Triassic to Early Jurassic 204−198 Ma diorite to quartz monzonite stocks and dykes. Gold and copper mineralisation at Red Chris consists of vein, disseminated and breccia sulphide typical of porphyry-style mineralisation. Mineralisation is hosted by diorite to quartz monzonite stocks and dykes. The main mineral assemblage contains well developed pyrite-chalcopyrite-bornite sulphide mineral assemblages as vein and breccia infill, and disseminations. The main mineralisation event is associated with biotite and potassium feldspar-magnetite wall rock alteration. |

| Drill hole Information | No new exploration results are reported in this release. A total of 487 drill holes for 287,534 metres drilled have been used to inform the resource estimate. To view an enhanced version of this graphic, please visit: https://orders.newsfilecorp.com/files/7614/99286_d29920b964b02b90_015full.jpg |

| Data aggregation methods | No new exploration results are reported in this release, therefore this section is not relevant. |

| Relationship between mineralisation widths and intercept lengths | No new exploration results are reported in this release, therefore this section is not relevant. |

| Diagrams | As provided above. |

| Balanced reporting | No new exploration results are reported in this release, therefore this section is not relevant. |

| Other substantive exploration data | No new exploration results are reported in this release, therefore this section is not relevant. |

| Further work | Growth drilling is underway within the Main Zone and east of the East Zone including the recent East Ridge discovery. |

Section 3: Estimation and Reporting of Mineral Resources

| Criteria | Commentary |

| Database integrity | Data are stored in a SQL acQuire database. Over 90% of IMC assay data has been electronically loaded into acQuire from the original laboratory assay files, whilst historical assay data prior to IMC has been imported and validated against historical public reports. The Red Chris JV assay and geological data are electronically loaded into acQuire and the database is replicated in Newcrest's centralised database system in Melbourne. Regular reviews of data quality are conducted by site and corporate teams prior to resource estimation. |

| Site visits | The Competent Person for the Mineral Resource estimate is an employee of Newcrest Mining Limited and is based in Melbourne. The Competent Person has remained closely linked with the project and completed multiple site inspections during 2019. The Competent Person has reviewed the open pit mining and processing operations, historical core storage and sampling systems, and has monitored drilling, sampling, sample security, drill logging, and data management and is satisfied with the quality of the measures undertaken. |

| Geological interpretation | The geology model for the Red Chris deposit comprises a cover Bowser Lake Group of siltstone, sandstones and conglomerates, and the Upper Triassic clastic sedimentary and mafic volcanic rocks of the Stuhini Group that was intruded by the late Triassic to early Jurassic Redstock monzonite to quartz monzodiorite intrusions. Broadly three phases of intrusive have been recognised as part of the Redstock that typically hosts the mineralisation and have been used as estimation domains. The confidence in the geological volumes used that were used to define the estimation domains is reflected in the resource classification. |

| Dimension | The mineralised zone defined by the drilling to date occupies an area with dimension around 0.3 km in width x 3.4 km in length and 1.3 km in a vertical extent. Currently three zone of mineralisation have been identified to date that includes the Gully, Main, and East Zones. |

| Estimation and modelling techniques | Geostatistical testing of the copper and gold grade distributions showed that the Redstock domain is highly diffusive in nature and satisfies the bi-gaussianity assumption of the data. Additionally the grade distribution for sulphur, iron, calcium, and magnesium are also diffusive in nature. Therefore, gaussian based estimation is considered appropriate to be implemented for copper, gold, sulphur, iron, calcium, and magnesium within the Redstock domain. All drillhole samples were composited to 12 metre intervals downhole and honouring the domain boundary. In the Redstock domain, Localised Uniform Conditioning of copper, gold, sulphur, iron, calcium, and magnesium are undertaken into a panel size of 80 m x 80 m x 12 m blocks and localised into the selective mining unit (SMU) of 20 m x 20 m x 12 m blocks in a single pass run using a discretisation of 4x4x1, search radii for copper and gold were typically around 300-400 m (major), 400-600 m (intermediate) and 140-150 m (minor). The minimum and maximum number of informing composites were 12 and 16-20 respectively, depending on the domain and variable being estimated. Due to weak to moderate skewed nature of the grade distribution, no grade capping has been applied, however, to make sure that the potential smearing of the outliers grade is reduced, when necessary a grade and distance restriction is applied for some variables. Additionally, Ordinary Kriging (OK) estimation of silver, mercury, antimony, arsenic, and carbon was undertaken within the Redstock domain directly into the SMU blocks respectively. The estimation for other domains including the sediment, volcanic and Bowser domain has utilised OK estimation for copper, gold, sulphur, iron, calcium, magnesium, silver, mercury, antimony, arsenic, and carbon directly into the SMU blocks respectively. Due to the very limited number of carbon data within the Bowser domain a Nearest Neighbour estimation was used. The block model used for interpolation was populated with local rotations for the Redstock domain based on the local orientation of the Redstock mineralisation and the orientation of the main structures. A soft boundary was applied between the Redstock domains, and a hard boundary with all other domains. The model has been validated using visual, statistical, and geostatistical methods, including statistical comparison, metal at risk analysis, swath plots, global change of support comparison, metal at panel and SMU comparison, and visual comparison of the drillholes and the blocks by sections and plan views. A ground truth model (GTM) within the current open pit area has also been estimated utilising the existing copper and gold blasthole data, where the comparison of the GTM and the resource estimate is considered acceptable. |

| Moisture | All tonnages are calculated and reported on a dry tonnes basis. |

| Cut-off parameters | A value algorithm is used to calculate the NSR for each block using revenue and cost assumptions as at December 2020. The NSR calculation takes into account the Mineral Resource revenue factors, metallurgical recovery assumptions, transport costs, refining charges and royalty charges with a gold price of US$1400/oz, copper price of US$3.40/lb, and a CAD:USD exchange rate of 0.80. The cut-off value for reporting within the open pit mining area is based on an NSR value above C$12.2/t that takes into consideration actual processing and general & administration costs. The cut-off value for reporting within the proposed underground mining area is based on an NSR value above C$21.0/t that takes into consideration proposed mining, processing, and general & administration costs based on Studies completed to date. |

| Mining factors or assumptions | Red Chris open pit is a surface bulk mining operation, so SMU mining assumptions are based on the current site parameters that are used in the open pit truck and shovel operation. An open pit optimisation footprint constraint is used, which is based on a maximum undiscounted cashflow at revenue factor 1.0 but with a relative level restriction of 1,112mRL to define the open pit to underground interface at approximately 50 metres below the current life of mine open pit design. For the proposed underground, the geometry, grade, indicative geotechnical properties, and size of the resource suggest an amenability to a mass underground mining method such as block caving based on the defined SMU with no internal selectivity. The underground footprint is based on a contiguous area with NSR value above C$ 21.0/t with a nominal minimum footprint of 160 x 160 m with assumed vertical walls and variable height of draw. These two contiguous footprints for open pit and underground are deemed appropriate to be used for the base of the reasonable prospect of eventual economic extraction test at Red Chris. |

| Metallurgical factors or assumptions | Metallurgical amenability is derived from current operating Red Chris JV plant performance for the open pit areas and additional composite test work samples derived from recent drilling for proposed underground areas. Metallurgical factors for gold and copper have been incorporated into the NSR value algorithm which defines the resource footprint. Domain specific metallurgical recoveries can range on average from 50-61% for Au and 81-83% for Cu. |

| Environmental factors or assumptions | Conventional waste management of potentially acid forming and non-acid forming rock and tailings is currently undertaken at the Red Chris JV operations in accordance with permit requirements. Relevant variables are estimated to determine both acid and neutralising potential to determine waste material types. |

| Bulk Density | All bulk density measurements are carried out in accordance with site standard procedure. Intervals for bulk density determination are selected according to lithology/alteration/mineralisation type to best represent certain intervals as defined by the geologist. Historically, the measurement were undertaken at ACME laboratory using the Archimedes method. Since the Red Chris JV commenced, the measurements are performed on site by geologists or geological assistants as part of the logging process using the Archimedes method. Both historical and recent measurements are generally taken at 100 metre intervals down hole. Bulk density from several thousand measurements has been interpolated using an inverse distance method within the relevant geological domains. |

| Classification | The resource classification is based on drillhole spacing and geological and grade continuity including the assessment of average weighted distance of informing samples and the quality of estimation. Additionally, the mining method, mining selectivity, mining rate and the cut-off value are also taken into consideration. Generally, Indicated Resources are classified within the average weighted distance of informing data less than 100 metres and a slope of regression (SOR) greater than 0.7, while Inferred Resources are classified outside of the Indicated classification, with an average weighted distance less than 175 metres and a SOR greater than 0.4. The Indicated and Inferred Mineral Resource classification appropriately reflects the view of the Competent Person referred to below. |

| Audits or reviews | Derisk Geomining Consultants has conducted an independent review of the Red Chris Mineral Resource estimate and concluded that the estimate has been prepared using accepted industry practice, has been completed in accordance with the JORC Code guidelines, is suitable for preparing a public report documenting the Mineral Resource estimate, and as a basis for developing Ore Reserves. |

| Discussion of relative accuracy/ confidence | For the open pit and underground, Indicated Resources are considered reasonable for the relative uncertainty to be +/- 15% in tonnage, grade and metal (exclusive of each other, i.e., each variable has to satisfy the criteria) for an annual production volume at a 90% confidence level. Geostatistical evaluations indicate that based on the annual processing throughput these criteria are satisfied. Relative uncertainties and confidence level estimates are considered for both copper and gold. For the open pit, detailed monthly mine reconciliations have been maintained since production commenced in 2015. The mine reconciliations confirm that the in situ tonnage, grade and metal variances are well within the Indicated Resource relative uncertainty band. |

Section 4: Estimation and Reporting of Ore Reserves for the Red Chris Block Cave Study

| Criteria | Commentary |

| Mineral Resource Estimate for conversion to Ore Reserves | The Red Chris Project is located in the Stikine terrane of north-western British Columbia, 80 km south of the town of Dease Lake. Gold and copper mineralisation at Red Chris consists of vein, disseminated and breccia sulphide typical of porphyry-style mineralisation. Mineralisation is hosted by diorite to quartz monzonite stocks and dykes. The main mineral assemblage contains well developed pyrite-chalcopyrite-bornite sulphide mineral assemblages as vein and breccia infill, and disseminations. The main mineralisation event is associated with biotite and potassium feldspar-magnetite wall rock alteration. The mineralised zone defined by the drilling to date occupies an area with dimension around 0.3 km in width x 3.4 km in length and 1.3 km in a vertical extent. Currently three zones of mineralisation have been identified to date that includes the Gully, Main, and East Zones. The underground reserves are derived from the East Zone resource directly below the East Zone pit. The Mineral Resource grades were estimated using Localised Uniform Conditioning of 12 m composites within the Redstock domain for six elements: gold, copper, sulphur, iron, calcium, and magnesium. The grades were estimated into a panel size of 80 m x 80 m x 12 m blocks and localised into the selective mining unit of 20 m x 20 m x 12m blocks. The Mineral Resource consists of both Indicated Mineral Resources and Inferred Mineral Resources. Classification is based on an assessment of geological confidence as a function of geological and mineralisation continuity, with reported resources constrained within a 'value' shell representing the limit for a reasonable prospect of eventual economic extraction. The reported Red Chris Mineral Resources are inclusive of Ore Reserves. Mineral Resources that are not Ore Reserves do not have demonstrated economic viability. |

| Site Visits | The Competent Person for the Ore Reserve estimate is an employee of Newcrest Mining Limited based in Melbourne and completed multiple site visits during 2019. |

| Study Status | The Red Chris Block Cave Pre-Feasibility Study completed in 2021 and is the supporting basis for the Red Chris underground Ore Reserve estimate. The Pre-Feasibility Study shows that the mine plan is technically achievable and economically viable taking into consideration all material Modifying Factors. |

| Cut-off Parameters | The Red Chris Ore Reserve employs a value-based cut-off determined from the Net Smelter Return (NSR) value equal to the site operating cost derived from the Pre-feasibility study. The NSR calculation takes into account Ore Reserve revenue factors, metallurgical recovery assumptions, transport costs, refining charges, and royalty charges. The site operating costs include mining cost, processing cost, relevant site general & administration costs and relevant sustaining capital costs. This results in shut off values for each block of; MB1 = C$22.00/t Milled, MB2 and MB3 C$22.80/t Milled. |

| Mining factors or assumptions | Estimation of the Red Chris Ore Reserve involved standard steps of mine optimisation, mine design, production scheduling and financial modelling. Factors and assumptions have been based on Newcrest's block cave operating experience and the Red Chris site conditions determined through geotechnical data collection programmes completed in 2020 and 2021. The basis of the analysis is considered at Pre-Feasibility Study level. Newcrest's block cave operating and construction experience in conjunction with the Pre-Feasibility geotechnical studies provided the direction for key Mine Design Parameters, including:

The resource estimate has been classified as Indicated Mineral Resources and Inferred Mineral Resources. The Ore Reserve estimate is based on Indicated Mineral Resource metal only. Dilution enters the ore stream and is estimated to be approximately 5% tonnes grading 0.1g/t Au and 0.1% Cu. Dilution is defined as material entering the ore stream from beyond the in-situ (No mixing) height of draws that has a value <C$$20.70/t. The Red Chris Block cave project is an underground greenfield mining project and will require the following mine infrastructure that has been included within the cost estimate:

|

| Metallurgical factors or assumptions | The anticipated recoveries for underground ore are 81 to 86% for copper and 60 to 75% for gold across the life of the project. Test samples focused mostly on the first 15 years of underground production but included some material from the remainder of the anticipated mine life. The mineralogy of underground samples was found to be more favourable for gold recovery than for current Red Chris open pit operations. Underground ore mineralogy was shown to have some upside for producing high copper concentrate grades due to the presence of enriched copper minerals such as bornite in certain zones in the orebody. The currently approved TIA has sufficient volume to accommodate tailings generated when mining the remaining open pit and MB1 ore. The PFS design provides increased capacity to the facility to accommodate up to 550 Mt of life-of-mine tailings (including since the start of Red Chris operations in 2015) through centre-line dam raises. |

| Environmental | Studies in the PFS identified potential areas of impact for the proposed Block Cave Project including the wildlife, soil, vegetation, and terrestrial ecosystems due to the limited incremental increase in the footprint of the mine. Potential impacts identified in the PFS were primarily associated with hydrogeology and hydrology surrounding the Block Cave, and to the aquatic receiving environment in the footprint of the proposed TIA expansion. Work will be carried out as part of the Feasibility Study to further develop our understanding of these impacts and potential management strategies. Findings of the water balance model indicate that the demands for water for operation of the Block Cave Project can be met under specific water management conditions aimed at improving reclaim during operations and recycling of water. A conceptual closure plan was developed for the Block Cave Project; this plan currently requires long-term water treatment of pit and block cave water with limited-duration treatment of TIA effluent seepage treatment. Forward works have been developed to address these risks and challenges in the Feasibility Study. |

| Infrastructure | Red Chris is an operating open pit mine producing ~10Mtpa of ore. There are existing facilities that support this operation. With the transition to underground mining and increased processing rate, upgrades to existing site infrastructure are required. The major infrastructure upgrade is the processing facility. The upgrade includes additional coarse ore stockpile, additional rougher flotation capacity, an upgraded regrind circuit, a new cleaner scalping systems, and duplication of existing concentrate thickening and filtration equipment. Other site infrastructure upgrades or inclusions to support the underground project are:

|

| Costs | Capital and operating costs have been determined as part of the Study and support the Ore Reserve. Capital cost estimates are based on multiple market prices across all technical disciplines and include processing upgrade and mine development costs along with associated infrastructure, project establishment and sustaining capital costs. These provisions have been allowed for during the life of the mine based on most recent Pre-Feasibility plan estimates. Contingency has also been factored into the project capital cost estimate consistent with the level of accuracy of the study. The operating cost estimate includes mining, processing, transportation and site general and administration costs. The existing open pit operation provides a strong basis for site general and administration and processing and transportation with the Study assessing these costs and updating them with the revised mining plan. The Ore Reserve cost estimates have been reviewed as part of the study execution, are reviewed annually and are considered to be to a Pre-Feasibility Study level. Transport and refining charges have been developed from first principles consistent with the application and input assumptions for these costs used by the current operation. These included charges for deleterious elements where applicable. Royalties are calculated as 1% NSR royalty payable to Royal Gold. |

| Revenue factors | The financial assessment of the Ore Reserve estimate is based on long term metal prices and exchange rate assumptions of US$1,300/oz for gold, US$$3.00/lb for copper at a CAD:USD exchange rate of 0.80. These Ore Reserve revenue factors are consistent with Newcrest metal price guideline for the December 2020 Ore Reserve reporting. The NSR calculation considers the Ore Reserve revenue factors, metallurgical recovery assumptions, transport costs and refining charges and royalty charges. |

| Market assessment | Newcrest is a price taker. The copper, gold and silver prices are determined by international markets and the sales revenue is based on these prices. These are open markets and subject to price fluctuations. Projected supply and demand for copper and gold suggests strong market interest for concentrate from the Red Chris open pit operation. It is not a constraint in the estimation of the Ore Reserve. Red Chris has sold copper concentrate for its operational life to the world concentrate markets. This will continue, with the expanded tonnage resulting in a broader smelter customer base. The focus of the Marketing team will continue to be the use of its skills, experience, and resources to ensure successful placement of concentrate at maximum prices while mitigating and reducing identified risks. Concentrate volume forecasts were sourced from the Study production schedule. |

| Economic | The Ore Reserve has been evaluated through a financial model. All operating and capital costs as well as Ore Reserve revenue factors stated in this document were included in the financial model. A discount factor of 4.5% real was applied. This process demonstrated the Red Chris Ore Reserve to have a positive NPV. Sensitivities were conducted on the key input parameters including commodity prices, capital and operating costs, ore grade, discount rate, exchange rate and recovery which confirmed the estimate to be robust. The NPV range has not been provided as it is commercially sensitive. |

| Social | The proposed Red Chris Block Cave Project requires an approach that generates support from the Tahltan Nation and leadership as well as the provincial government. This approach includes:

|

| Other | The permitting plan proposes a staged approach to permitting, appropriate to the long-term nature of the Project. The Energy, Mines & Low Carbon Innovation, Environmental Assessment Office, and Tahltan Central Government through its representatives have been consulted by Newcrest on the permit applications submitted by Newcrest to date. Newcrest will continue to engage and consult with the Tahltan Central Government and government agencies on the development of the permitting plan for the Project. Findings of the water balance model indicate that the demands for water for operation of the Block Cave Project can be met under specific water management conditions aimed at improving reclaim during operations and recycling of water. A conceptual closure plan was developed for the Block Cave Project. This plan currently requires long-term water treatment of pit and block cave water with limited-duration treatment of TIA effluent seepage treatment. Forward works have been developed to address these risks and challenges in the Feasibility Study. The currently approved TIA has sufficient volume to accommodate tailings generated when mining the remaining open pit and MB1 ore. The PFS design provides increased capacity to the facility to accommodate up to 550Mt of life-of-mine tailings (including since the start of Red Chris operations in 2015) through centre-line dam raises. Newcrest has identified a pathway to obtain the required regulatory approvals for the Project and is actively engaging with the Tahltan Central Government and government agencies to obtain the regulatory approvals required to enable execution of the Project in a phased manner. |

| Classification | The Probable Ore Reserve is based on Indicated Mineral Resources. No Measured Mineral Resources are stated for this deposit. The resource classification is based on an assessment of geological confidence as a function of geological and mineralisation continuity, with reported resources constrained within a 'value' shell representing the limit for a reasonable prospect of eventual economic extraction. It is the Competent Persons view that the classifications used for the Ore Reserves are appropriate. |

| Audits or reviews | Golder Associates Pty Ltd (Golder) was commissioned to conduct an independent review of the Ore Reserve estimation processes and results. Golder concluded that the Ore Reserve had been prepared using accepted industry practice and is considered suitable and reported in accordance with the JORC Code, 2012 Edition. |

| Discussion of relative accuracy/ confidence | The accuracy of the estimates within this Ore Reserve is mostly determined by the order of accuracy associated with the Mineral Resource model, the geotechnical input and the cost factors used. The Competent Person views the Red Chris Ore Reserve as a reasonable assessment of the global estimate. Some risks and opportunities are associated with the Ore Reserve process due to the underground greenfield nature of the project transitioning from open pit mining. Remaining areas of uncertainty at this stage are associated with:

|

Section 4: Estimation and Reporting of Open Pit and Stockpile Ore Reserves

| Criteria | Commentary |

| Mineral Resource Estimate for conversion to Ore Reserves | A technical description of the Mineral Resource estimate that provided the basis for the Red Chris Open Pit Ore Reserve estimate is presented in the preceding sections. The Red Chris orebody is located in the province of British Columbia, Canada and is 18km southeast of the town of Iskut and 80km south of Dease Lake. The conversion of resource to reserve is driven by modifying factors assigning practical and value drivers to available resource inventories. Pit optimisation, pit design and cut-off grades are the primary tool for the conversion of Measured and Indicated Mineral Resources into Probable Ore Reserves. Inferred Mineral Resources and unclassified material are treated as waste and given zero grade. The Red Chris mine is an operating mine and has recently completed Newcrest life of province plan and updated mine production schedules and pit designs per quarterly forecasts. Ore Reserves are reported on a 100% basis rather than the 70:30 ownership condition between Newcrest Mining Limited (70%) and Imperial Metals Corporation (30%). The nominated and company approved Competent/Qualified Person (QP/CP) for Reserves is Brett C Swanson, BE (Min) MMSAQP #04418QP. The reported Red Chris Mineral Resources are inclusive of Ore Reserves. |

| Site Visits | The Competent Person for the Ore Reserve estimate is an employee of Newcrest Mining Limited and at the time of the Ore Reserve preparation was the Principal Open Pit Mining Engineer (Group). The Competent Person has not visited the Red Chris mine due to COVID-19 restrictions. |

| Study Status | Production at Red Chris commenced in 2012 and it is now a mature and stable operation with well-established mining and processing performance. Inputs for the Ore Reserve estimate have been determined as part of the life of province planning cycle and FY22 Q1 Forecast. The results are also included in the 2021 Pre-Feasibility Study on the potential Red Chris Underground. |

| Cut-off Parameters | Red Chris open pit employs a multi-metal NSR based cut-off considering metallurgical recovery assumptions, transport costs, refining and royalty charges. The site operating costs include processing cost, relevant site general and administration costs and relevant sustaining capital costs. A value algorithm is used to calculate the NSR for each block using revenue and cost assumptions as at June 30th 2021 with a gold price of US$1300/oz, copper price of US$3/lb, and a CAD:USD exchange rate of 0.75. The cut-off value for reporting within the open pit mining area is based on an NSR value above C$16.5/tonne milled. These Ore Reserve revenue factors are consistent with Newcrest metal price guideline for the December 2020 Ore Reserve reporting. |

| Mining factors or assumptions | Estimation of the Red Chris Reserve involved standard steps of pit optimisation, mine design, production scheduling and financial modelling. Factors and assumptions have been determined as part of a prefeasibility level study or are based on operating experience and performance. Current mining activity at Red Chris is via conventional truck and shovel operation, with segregated disposal of non acid generating (NAG) and potentially acid generating (PAG) waste. The current mining activities demonstrate the appropriateness of this mining method as the basis of the Ore Reserve estimate. Mine design parameters are:

The Red Chris Resource Model utilises Localised Uniform Conditioning (LUC) to estimate block metal content. This process allows for ore dilution and recovery to be built into the resource model based on the assumption of the selective mining unit (SMU) as the block size. The SMU assumption (20m x 20m x 12m) is based on the mining fleet size and is consistent with a high mill throughput/bulk mining strategy. Due to the LUC approach adopted in the resource model no additional mining dilution or recovery factors have been applied to the Ore Reserve estimate. This assumption is supported by the actual reconciliation between resource model and mill performance at Red Chris project to date being within an acceptable uncertainty range for the style of mineralisation under consideration. Adequate tailings and waste storage areas have been defined to support the reported open pit Ore Reserves. |