Plateau Energy Metals Announces Positive Preliminary Economic Assessment for Falchani Lithium Project

- Scalable, long mine life battery grade lithium chemical project in Peru. Production of approximately 63,000 tonnes per annum (“tpa”) average over 33 years of battery-grade lithium carbonate (“Li2CO3”) growing to 85,000 tpa Li2CO3 at steady state throughput of 6.0 million tpa

- After-tax NPV8% $1.55 billion at $12,000/t Li2CO3; after-tax IRR of 19.7%

- Low 2nd quartile operating costs. Benchmark Minerals Intelligence (“BMI”), the leading market data provider for the lithium ion battery industry, rates Falchani Project in the low 2nd quartile of operating costs at $3,958 per tonne Li2CO3

- Green mining initiatives. Development plan incorporates multiple responsible mining methods

TORONTO, Feb. 04, 2020 (GLOBE NEWSWIRE) -- Plateau Energy Metals Inc. (“Plateau” or the "Company") (TSX-V:PLU | OTCQB:PLUUF) is pleased to announce the results from an independent Preliminary Economic Assessment (“PEA”) for the Falchani Lithium Project (“Falchani Project” or “Project”) located on the Macusani Plateau in the Puno District of southeastern Peru. The PEA, prepared in accordance with National Instrument 43-101 (“NI 43-101”) by DRA Global (“DRA”), demonstrates the Falchani Project’s ability to become a large, long life producer of low cost, high quality-low impurity battery grade Li2CO3. Unless otherwise stated, all dollar figures are in United States dollars (“$”) and the economic highlights represent Plateau’s 100% interest in the Falchani Project.

“The battery supply chain is evolving and growing rapidly and as a result, significant amounts of lithium chemical supplies for batteries are required to meet the over $450 billion of capital committed by vehicle manufacturers and battery plants,” stated Alex Holmes, CEO of Plateau. “What we have at Falchani is a project that has the potential to respond as the market grows, with a low impurity battery grade lithium chemical product, a long mine life set to last through cyclical price environments, and importantly, the potential to be one of the greener lithium projects in the future.”

“In two short and fast paced years, the Falchani Project has gone from greenfield discovery through to a near doubling of our maiden resource, with extensive metallurgical test work, trade-off studies and engineering analysis - today is a significant milestone for our company and Peru,” stated Laurence Stefan, President & COO of Plateau. “We are extremely proud of our Peruvian team, who with our collective strengths, are showcasing the Falchani Project as an opportunity for Peru to become a considerable player in the rapidly evolving battery future.”

PEA Mineral Resources

The Base Case considered the entire Mineral Resource estimate for the Falchani and Ocacasa 4 concessions, as described in the 2019 Technical Report. As there have been changes to the mineral tenure circumstances, particularly with respect to the dispute over the ownership of the Ocacasa 4 concession, the split between Falchani and Ocacasa 4 is provided in Table 2 on page 4 for additional clarity. The Alternative Case considered a sub-set of the Mineral Resource estimate described in the 2019 Technical Report, that being the Mineral Resources contained within the Falchani concession only. The Mineral Resource estimates have not been updated to inform the PEA, however, owing to the current mineral tenure dispute, for the Alternative Case, only the Falchani Concession Mineral Resource estimate has been considered.

These mineral tenure circumstances have been considered, and on the basis of the information provided to the QP by Plateau, the QP considers it reasonable to continue to report these estimates as Mineral Resources. Please refer to the Cautionary Note Regarding Concessions at the end of this news release.

Key PEA Base Case Highlights

- Robust economic returns (after-tax):

-- At Base Case of $12,000/t Li2CO3: NPV(8%) = $1.55 billion, IRR = 19.7%, 4.7 year payback (undiscounted)

-- At $10,000/t Li2CO3: NPV(8%) = $0.94 billion, IRR = 15.6%, 5.9 year payback (undiscounted)

-- At BMI price assumption1: NPV(8%) = $1.98 billion, IRR = 23.4%, 3.6 year payback (undiscounted) - Mine life (“LOM”): 33 years

- Low 2nd quartile2 operating cost: $3,958 per tonne Li2CO3 average LOM (no by-products included)

- Li2CO3 production: approximately 63,000 tpa average LOM, over 2 million tonnes LOM

- Three phase approach, designed to achieve after-tax cash flow positive prior to expansion:

-- Phase 1 (year 1-7)3: approximately 22,000 tpa (steady state) battery grade Li2CO3

-- Phase 2 (year 8-12): approximately 45,000 tpa (steady state) battery grade Li2CO3

-- Phase 3 (year 13-33): approximately 85,000 tpa (steady state) battery grade Li2CO3 - Initial capital expenditures: $587 million (including contingency)

1. Per BMI price assumption: $15,675/t Li2CO3 (2025), $16,200/t Li2CO3 (2026), $14,650/t Li2CO3 (2027) and 2028 onwards $13,100/t Li2CO3;

2. Per cost profile of the industry as completed by BMI; 3. Excluding 2-year construction period.

Key Project Attributes

- Scaled approach to development allows the Project to grow with market demand

- Battery grade, low impurity lithium chemical allows complete onsite production, maximizing the Company’s share of the value chain

- Lithium-rich sulfate process step supports flexibility to adapt lithium chemical production for industry demand

- Onsite acid plant provides green power generation and enables low cost reagent access

- Inputs sourced largely in Peru support local development while reducing costs and value-added taxes

- Availability of contract mining reduces CAPEX and provides flexibility during expansion phases

- Major contributor to economic development in Peru of approximately $2.1 billion LOM capital investment and tax and royalty contributions estimated in excess of $5 billion1

- Excellent infrastructure near site to support future Project development and operations

1. Royalties: approximately $760 million, Workers Participation Tax & Pension Fund: approximately $1.25 billion, Income Tax: approximately $3.75 billion

Green Project Initiatives

- Water Efficiency: Use of filtered tailings enables recycling of up to 90% of process water

- Environmental and Personnel Safety: Use of environmentally responsible dry stacking tailings technology

- Clean Energy Generation: Sulfuric acid plant on site produces sufficient clean energy to power entire process plant and provide excess power

- Renewable Energy: Access to hydro power grid available nearby

- Future development work to evaluate opportunities such as:

-- electric mine fleet with excess clean energy storage on site

-- rainwater run off storage and additional water recycling

-- low CO2 transport and logistics for consumables

Future Project Opportunities

The PEA identifies several opportunities which may greatly enhance the economics and include:

- Revenue opportunities: further evaluation of additional revenue streams, not included in the PEA, such as SOP fertilizer (K2SO4), caesium sulfate (Cs2SO4) and rubidium sulfate (Rb2SO4). Preliminary metallurgical test work is currently underway.

- Capital optimization: alternative acid plant and processing plant/equipment sourcing, including evaluating options for “over the fence” acid and power purchase from a third-party operator.

- Operating cost optimization: long-term contracts for major consumables, reduction in processing consumables and/or costs through process model optimization.

Table 1. - Falchani Project PEA Key Highlights

The Falchani Project PEA presents a “Base Case” scenario which is inclusive of both the Falchani and Ocacasa 4 concessions. The “Alternative Case” scenario presented represents only the Falchani concession to demonstrate the economic value as if the Falchani concession were a standalone or phase 1 project in light of the current dispute with regards to the ownership of the Ocacasa 4 concession. Please refer to the Cautionary Note Regarding Concessions at the end of this news release.

| Description | Units | Base Case | Alternative Case |

| LCE Spot Price | tonne | 12,000 | 12,000 |

| Life of Mine | years | 33 | 26 |

| Processing Rate P1 / P2 / P31 | Mtpa | 1.5 / 3.0 / 6.0 | 1.5 / 3.0 / NA |

| Average Throughput (P1) | tpa | 1,437,500 | 1,437,500 |

| Average Throughput (LOM) | tpa | 4,407,687 | 2,421,780 |

| Li2CO3 Produced (average LOM)1 | tpa | 63,034 | 33,842 |

| P1 Li2CO3 Production (steady state) | tpa | 22,678 | 22,731 |

| P2 Li2CO3 Production (steady state) | tpa | 44,227 | 41,252 |

| P3 Li2CO3 Production (steady state) | tpa | 85,230 | n/a |

| LCE Produced (total LOM)1 | tonnes | 2,080,113 | 879,895 |

| Unit Operating Cost (OPEX) P12 | $/LCE tonne | 4,438 | 4,348 |

| Unit Operating Cost (OPEX) LOM2 | $/LCE tonne | 3,958 | 4,333 |

| Gross Revenue | $ B | 24,961 | 10,558 |

| Capital Cost (CAPEX)3 P1 | $ M | 587 | 587 |

| Capital Cost (CAPEX)3 LOM | $ M | 1,970 | 1,082 |

| Sustaining Capital Costs (undiscounted) | $ M | 119.6 | 66.4 |

| Project Economics - $12,000/t Li2CO3 | |||

| Pre-tax: | |||

| Net Present Value (NPV) (8%) | U$ M | 2,712 | 1,514 |

| Internal Rate of Return (IRR) | % | 24.2 | 23.5 |

| Payback Period (undiscounted) | years | 4.3 | 4.2 |

| Average Annual Cash Flow (LOM) | $ M | 444 | 215 |

| Cumulative Cash Flow (undiscounted) | $ M | 14,638 | 5,597 |

| After-tax: | |||

| Net Present Value (NPV) (8%) After-Tax | $ M | 1,554 | 844 |

| Internal Rate of Return (IRR) After-Tax | % | 19.7 | 18.8 |

| Payback Period (undiscounted) | years | 4.7 | 4.6 |

| Average Annual Cash Flow (LOM/P2 or P3 steady state) | $ M | 272 / 430 (P3) | 131 / 198 (P2) |

| Cumulative Cash Flow (undiscounted) | $ M | 8,977 | 3,418 |

Notes:

- Production: base case is 3 phases, 1.5Mtpa, 3Mtpa and 6Mtpa; alternative case is 2 phases 1.5Mtpa and 3Mtpa.

- Includes all operating expenditures, the estimate is expected to fall within an accuracy level of ±35%.

- Includes 11% contingency on process plant capital costs, 15% contingency is included in the tailings and infrastructure costs, and closure costs (LOM).

The Falchani Project PEA

The Falchani Project is within the Falchani and Ocacasa 4 concessions held by Macusani Yellowcake S.A.C (“Macusani”), a 100% controlled subsidiary of Plateau. The Falchani Project is situated on the Macusani Plateau, located in the Carabaya Province, Puno District of south-eastern Peru in the Andes Mountains, which has been actively explored for uranium since the 1980’s, and more recently for lithium. Located approximately 650 km east southeast of Lima and about 220 km by the Interoceanica Highway from Juliaca in the south, two roads connect the Falchani Project to the Interoceanica Highway and are accessible year-round. The town of Macusani is 25 km to the southeast of the Company’s Project area.

The PEA has considered only the lithium-rich bearing tuffs (“LRT”), namely LRT1, LRT2, and LRT3, three of five geological units presented in the Falchani Project technical report, effective March 1, 2019, prepared in accordance with NI 43-101 by Mr. Stewart Nupen (“QP”) of The Mineral Corporation and filed on SEDAR (the “2019 Technical Report”). As a result, the Base Case and Alternative Case utilize less than 48% and 47%, respectively, of the total mineral resource estimates included in the 2019 Technical Report.

Readers are cautioned that the PEA is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty the results of the PEA will be realized. Mineral resources are not mineral reserves and do not have demonstrated economic viability. Additional work is required to upgrade the mineral resources to mineral reserves. In addition, the mineral resource estimates could be materially affected by environmental, geotechnical, permitting, legal, title, taxation, socio-political, marketing or other relevant factors.

Table 2. - Falchani Project Mineral Resources

The Mineral Resource estimates in the PEA, are based on a 1,000 ppm lithium (“Li”) cut-off grade.

| Licence | Category | Zone | Metric Tonnes (Mt) | Li (ppm) | Li2O (%) | Li2CO3 (%) | Contained Li2CO3 (Mt) |

| FALCHANI | Indicated | UBX | 5.38 | 1 472 | 0.32 | 0.78 | 0.04 |

| LRT1 | 6.15 | 3 718 | 0.80 | 1.98 | 0.12 | ||

| LRT2 | 16.66 | 3 321 | 0.72 | 1.77 | 0.29 | ||

| LRT3 | 11.03 | 3 696 | 0.80 | 1.97 | 0.22 | ||

| LBX | 10.16 | 1 901 | 0.41 | 1.01 | 0.10 | ||

| Total | 49.39 | 2 961 | 0.64 | 1.58 | 0.78 | ||

| Inferred | UBX | 8.44 | 1 616 | 0.35 | 0.86 | 0.07 | |

| LRT1 | 13.84 | 3 290 | 0.71 | 1.75 | 0.24 | ||

| LRT2 | 28.68 | 2 994 | 0.64 | 1.59 | 0.46 | ||

| LRT3 | 16.13 | 3 292 | 0.71 | 1.75 | 0.28 | ||

| LBX | 57.39 | 2 250 | 0.48 | 1.20 | 0.69 | ||

| Total | 124.48 | 2 629 | 0.57 | 1.40 | 1.74 | ||

| OCACASA 4 | Indicated | UBX | 0.85 | 1 750 | 0.38 | 0.93 | 0.01 |

| LRT1 | 1.32 | 3 668 | 0.79 | 1.95 | 0.03 | ||

| LRT2 | 5.37 | 3 232 | 0.70 | 1.72 | 0.09 | ||

| LRT3 | 2.00 | 3 658 | 0.79 | 1.95 | 0.04 | ||

| LBX | 2.00 | 1 379 | 0.30 | 0.73 | 0.01 | ||

| Total | 11.53 | 2 926 | 0.63 | 1.56 | 0.18 | ||

| Inferred | UBX | 5.33 | 1 911 | 0.41 | 1.02 | 0.05 | |

| LRT1 | 10.17 | 3 422 | 0.74 | 1.82 | 0.19 | ||

| LRT2 | 33.62 | 3 292 | 0.71 | 1.75 | 0.59 | ||

| LRT3 | 21.11 | 3 349 | 0.72 | 1.78 | 0.38 | ||

| LBX | 65.36 | 2 297 | 0.49 | 1.22 | 0.80 | ||

| Total | 135.59 | 2 777 | 0.60 | 1.48 | 2.00 |

UBX = upper breccia; LRT = lithium rich tuff; LBX = lower breccia

Notes: Minor discrepancies due to rounding may occur. Li Conversion Factors as follows: Li:Li2O=2.153; Li:Li2CO3=5.323; Li2O:Li2CO3=2.473. Geological losses of 5% or 10% have been applied, based on geological structure and data density. The average geological loss is 6%. Density = 2.40.

Base Case PEA Economics

The PEA indicates that the Falchani Project has the potential to be a long-life project, with significant cash flows, strong margins and project flexibility.

Table 3. - Falchani Project Metal Pricing NPV8% and IRR Sensitivity

| Sensitivity ($)/t | -30% | -20% | -10% | Base Case $12,000/t | 10% | 20% | 30% |

| Pre-tax NPV8% (millions) | $951 | $1,538 | $2,125 | $2,713 | $3,300 | $3,887 | $4,474 |

| Pre-tax IRR (%) | 14.7 | 18.1 | 21.2 | 24.2 | 26.9 | 29.6 | 32.1 |

| After-tax NPV8% (millions) | $431 | $815 | $1,192 | $1,554 | $1,919 | $2,286 | $2,645 |

| After-tax IRR (%) | 11.8 | 14.7 | 17.4 | 19.7 | 22.0 | 24.2 | 26.1 |

Base Case Mining

Based on the analysis completed by DRA, the Falchani Project is highly amenable for development by conventional open pit truck and shovel operation.

Table 4. - Mining Rates

| Parameter | Unit | Value |

| Mine Production Life | Years | 33 (+1 for pre-production)1 |

| Material milled | Mt | 145.4 |

| Mill head grade | % Li2CO3 | 1.78 |

| Recovered Li2CO3 | Mt | 2.1 |

| Waste | Mt | 141 |

| Total Material | Mt | 287 |

| Strip Ratio | (tw:to) | 0.97 |

1. 2 years for construction.

Falchani concession mineralized material in the Base Case mine plan is 100% in the first 10 years and 62% for the following 5 years, after which 55% of mineralized material increasingly comes from the Ocacasa 4 concession. The strip ratio is higher in the early years to gain quick access to the higher-grade LRT. The mining inventory contains 70.2% inferred mineral resources and is based on preliminary geotechnical designs and test work gathered during the DRA site visit. All waste and overburden material are considered non-payable and will be used as fill or be placed on stockpile nearby the open pit. The open pit is developed in six phases during the life of the Project.

Table 5. - In-situ Optimized Shell Content (Base Case)

| Falchani and Ocacasa 4 | ||||

| Pit Shell | Mineralized (Mt) | Lithium (ppm) | Li2CO3 Equivalent (%) | Contained LCE (Mt) |

| Indicated | 43.2 | 3,439 | 1.83 | 0.79 |

| Inferred | 102.2 | 3,296 | 1.75 | 1.79 |

| TOTAL | 145.4 | 3,338 | 1.78 | 2.58 |

Notes: Minor discrepancies due to rounding may occur. Li Conversion Factors as follows: Li:Li2O=2.153; Li:Li2CO3=5.323; Li2O:Li2CO3=2.473. UBX and LBX included in the 2019 Technical Report are not included. Geological losses of 5% or 10% have been applied, in the Mineral Corporation 2019 Technical Report resource model, based on geological structure and data density. LRT only.

The majority of the upper breccia (“UBX”) mined is stockpiled for potential future processing and the majority of lower breccia (“LBX”) is currently not incorporated into the PEA mine plan until any additional revenue streams are further evaluated. The UBX and LBX tend to be lower grade in lithium, when compared to the LRT, however elevated in the content of what is currently considered as an impurity rejection, such as potassium (“K”) for potential sulfate of potash (“SOP”) production (refer to flow sheet in July 18, 2019 news release referenced below).

Base Case Processing

The process flow sheet, including plant, equipment and up-front leaching and downstream precipitation was developed by DRA, working with ANSTO Minerals’ (“ANSTO”) laboratories with input from M.Plan International (“M.Plan”). Following mining, mineralized material will be crushed to P80 150 mm, followed by warm (95 °C) sulfuric acid (H2SO4) tank leach processing for a residence time of 24 hours, to extract 89% of lithium to leach solution. The process utilizes conventional up-front tank leaching, widely used in various mining operations to extract metals from mineralized material today. This is followed by a 3-stage purification process to reduce various impurities in the leach solution, mechanical evaporation and conventional precipitation, using a crystallization plant, to produce a high purity/low impurity battery grade Li2CO3 product as demonstrated by test work run by ANSTO and described in the July 18, 2019, press release. The estimated time from mining to producing a battery grade end-product is approximately 48 hours. An overall recovery of 80% from mineralized material to Li2CO3 is utilized in the PEA.

As a significant portion of the operating costs are derived from sulfuric acid use as the leaching reagent, the PEA includes the construction of a 1,700 tonnes per day (“tpd”) sulfur burning acid plant at site, in P1, to produce, on average, 1,500 tpd of sulfuric acid. In subsequent phases, additional modules are added to meet expanded processing capacity.

Base Case Capital Costs

P1 capital costs are estimated at $587 million, which includes all indirect costs and a $51 million contingency for the process plant (or 11% of total processing plant costs). The contingency is a weighted average obtained by applying different contingency percentages, ranging from 7.5% to 20%, to the different cost elements of the capital estimate based on the level of detail of the quotes received, their inclusions, and the DRA estimates. A separate contingency is included in the infrastructure capital cost estimate of 15%. The capital cost estimates are based on quotes for current labour and material costs, sourcing in-country where possible and out of country for certain plant and equipment. Quotes were received from third-party vendors with recent plant build and implementation experience for over 80% of the value of the P1 equipment. DRA, utilizing its recent engineering, procurement and construction management (“EPCM”) experience on numerous other projects with similar plant and equipment accordingly estimated the installed completion cost.

Capital expenditures for future expansion phases were factored where P2 and P3 plant and equipment capital were adjusted to 80% of the initial plant and equipment capital costs to account for sunk costs in P1 and use of existing development completed in P1. Tailings storage facilities capital costs are proportioned over the life of the mine, with a total of three facilities utilized in the base case.

The construction period has been scoped out for 24 months. A two-year ramp-up allowance for the processing plant has been included based on 50% of nameplate capacity in year 1, 75% in year 2 and 100% in year 3 for P1. Expansion for P2 and P3 allow for a processing ramp-up of 50% in the first year and achieving 100% in the second year. The mining rate and mine plan reflect this ramp-up period accordingly.

Cash flow from P1 at $12,000 per tonne Li2CO3 is anticipated to partially fund P2 expansion and P2 cash flows anticipate to fully fund P3 expansion.

Table 6. - Detailed Capital Cost Estimates (Base Case):

| Capital Costs ($ millions) | P1 | P2 | P3 | LOM |

| Mining (pre-strip and capital) | 19.2 | - | - | 19.2 |

| Processing plant - Direct costs | 341.5 | 297 | 595 | 1,161.1 |

| Processing plant – Infrastructure | 30.3 | - | 103.1 | |

| Tailings & bulk infrastructure1 | 53.6 | 7.2 | 112 | 173.0 |

| Total Direct Costs | 444.6 | 304.8 | 609.5 | 1,456.4 |

| Total Indirect Costs (Process Plant)2 | 91.4 | 73.1 | 146.3 | 310.8 |

| Contingency (Process Plant)11% | 51.0 | 40.8 | 81.5 | 173.2 |

| Closure Costs | - | - | - | 30.0 |

| TOTAL | 587.0 | 418.6 | 934.8 | 1,970.4 |

| Sustaining Capital Costs | - | - | - | 119.6 |

- Tailings built in phases and included in P1 and P3 capital cost estimate, inclusive of 15% contingency

- Includes EPCM, spares, insurances, owners’ team.

Base Case Operating Costs

The PEA is based on the use of a mining contractor with an estimated cost of $2.40 per tonne of material moved; this mining cost has been reviewed based on high altitude operating conditions, cross-checked with benchmarking of similar operations.

Operating costs for the Project are based on reagent consumable quantities, sourcing of the reagents (in-country, where available, and out-of-country), transportation costs to site from various source locations and include value added taxes of approximately 18%. In-country reagents, specifically limestone and quicklime have been quoted from local suppliers and benefit the Project from reduced transportation costs as well as benefitting local operators.

The price to produce sulfuric acid is a significant component of operating costs, representing approximately 30% of process operating costs. Local sourcing of sulfuric acid (H2SO4) is an option, at approximately $100 per tonne of H2SO4 delivered to the Project site, based on previous estimations. As the price of sulfuric acid has fluctuated in a wide range over the past 15 years, and given the significant component to the total operating cost, onsite production of sulfuric acid was chosen for the operating plan and is optimal for health, safety and environmental management.

The sulfuric acid plant will convert bulk sulfur into low-cost sulfuric acid reducing transportation costs, risks and hazards, and includes a waste heat boiler system for high pressure steam generation and clean energy production. Excess power is generated, but no economic value or alternative use has been incorporated in the PEA, i.e. potentially being introduced into the grid, at this time.

Sulfur is a waste product of heavy oil refining and as part of future development work the Company will seek opportunities to work with oil and gas companies to secure a long-term, low cost supply of bulk sulfur.

The acid plant was quoted from Outotec OYJ of Finland and represents $140 million of the initial capital cost estimate as noted above.

An onsite acid plant will benefit the Falchani Project in a number of ways, including: (i) reducing the cost per tonne of H2SO4; (ii) efficiency of transportation – one part sulfur will make three parts sulfuric acid; (iii) producing steam used in the downstream processing to produce Li2CO3; and (iv) generating sufficient and clean energy to be a self-sustaining project (approximately 18 mega-watts (“MW”) in P1, 36 MW in P2 and 72 MW in P3).

The estimated LOM average cash operating cost per tonne of battery grade Li2CO3 in the Base Case is $3,958, the total operating cost, inclusive of sustaining capital, is $4,016 with a breakdown as follows:

Table 7. - Base Case Operating Costs – LOM

| $ per tonne of mineralized material | $ per tonne of Li2CO3 | |||

| Mining | $4.63 | $324 | ||

| Processing Costs | $49.24 | $3,443 | ||

| General & Administration | $1.77 | $124 | ||

| Tailings Handling | $0.97 | $68 | ||

| Total Cash Operating Costs | $56.60 | $3,958 | ||

| Sustaining capital expenditures | $0.82 | $58 | ||

| Total Operating Costs* | $57.42 | $4,016 | ||

* See Alternative Performance Measures at the end of this news release for additional information.

Based on the market supply, demand and operating cost profile of the industry as completed by Benchmark Mineral Intelligence, the Falchani Project ranks in the low 2nd quartile of the total cost curve (as defined by Benchmark) in all categories in 2025.

Taxation and Royalties

Taxation and royalties, calculated for the PEA, include the progressive Modified Mining Royalty (MMR), Workers Participation Tax, Mining Pension Fund contribution and Corporate Tax. The Falchani Project is not subject to the Specialty Mining Tax as lithium and Li2CO3 are not considered a metallic mineral. The tax model used should be regarded as conceptual but is deemed to be suitable for a PEA.

Alternative Case

The PEA also presents an Alternative Case which includes only the mineral resources from the Falchani concession. Like the Base Case, the Alternative Case will use the same operating parameters, metal price and selling costs and consists of an open pit mine and an associated processing facility along with onsite and off-site infrastructure. The mine is projected to be 26 years with two phases: P1 - at 1.5 Mtpa (years 1-7) milling rate and P2 at 3.0 Mtpa (years 8-26). Positive after-tax cash flow from P1 at $12,000 per tonne Li2CO3 is achieved prior to P2 expansion. Costs are generally higher for the Alternative Case as a result of a reduction in economies of scale provided by the Base Case scenario ramp-up to 6 million tpa throughput rate.

Contributions to the economic development in Peru with total capital investment of approximately half of the Base Case at $1.15 billion LOM. Tax and royalty contributions, also approximately 50% less, are estimated at $2.6 billion.

Table 8. - In-situ Optimized Shell Content (Alternative Case)

| Falchani Concession | ||||

| Pit Shell | Mineralized (Mt) | Lithium (ppm) | Li2CO3 (%) | Contained LCE (Mt) |

| Indicated | 24.8 | 3 492 | 1.86 | 0.46 |

| Inferred | 38.6 | 3 115 | 1.66 | 0.64 |

| TOTAL | 63.4 | 3 262 | 1.74 | 1.10 |

Notes: Minor discrepancies due to rounding may occur. Li Conversion Factors as follows: Li:Li2O=2.153; Li:Li2CO3=5.323; Li2O:Li2CO3=2.473. UBX and LBX included in the 2019 Technical Report are not included. Geological losses of 5% or 10% have been applied, in The Mineral Corporation 2019 Technical Report resource model, based on geological structure and data density. LRT only.

Table 9. - Falchani Project Metal Pricing NPV8% and IRR Sensitivity (Alternative Case)

| Sensitivity ($)/t | -30% | -20% | -10% | Base Case $12,000/t | 10% | 20% | 30% |

| Pre-tax NPV8% (millions) | $418 | $783 | $1,149 | $1,514 | $1,880 | $2,245 | $2,610 |

| After-tax IRR (%) | 13.2 | 17.0 | 20.4 | 23.5 | 26.4 | 29.2 | 31.8 |

| After-tax NPV8% (millions) | $130 | $376 | $616 | $844 | $1,076 | $1,307 | $1,532 |

| After-tax IRR (%) | 10.0 | 13.4 | 16.3 | 18.8 | 21.2 | 23.5 | 25.6 |

Table 10. - Capital Expenditures (Alternative Case)

| Capital Costs ($ millions) | P1 | P2 | LOM |

| Mining (pre-strip and capital) | 19.2 | - | 19.2 |

| Processing plant - Direct costs | 341.5 | 297.4 | 638.9 |

| Processing plant – Infrastructure | 30.3 | - | 30.3 |

| Tailings & bulk infrastructure1 | 53.6 | 54.5 | 108.2 |

| Total Direct Costs | 444.6 | 351.9 | 796.6 |

| Total Indirect Costs | 91.4 | 73.1 | 164.5 |

| Contingency | 51.0 | 40.8 | 91.7 |

| Closure Costs | - | - | 30.0 |

| TOTAL | 587.0 | 465.9 | 1,082.8 |

| Sustaining Capital Costs | - | - | 66.4 |

- Tailings built in phases and included in P1 and LOM capital cost estimate due to phased capital expenditures.

Table 11. - Operating Costs (Alternative Case)

| Operating Costs – LOM | $ per tonne of mineralized material | $ per tonne of Li2CO3 | ||

| Mining | $5.63 | $403 | ||

| Processing Costs | $51.40 | $3,678 | ||

| General & Administration | $2.64 | $189 | ||

| Tailings Handling | $0.88 | $63 | ||

| Total Cash Operating Costs | $60.50 | $4,333 | ||

| Sustaining capital expenditures | $1.05 | $75 | ||

| Total Operating Costs* | $61.55 | $4,408 | ||

* See Alternative Performance Measures at the end of this news release for additional information.

Permitting & Environmental

A baseline environmental study (the “Baseline Study”) started by ACOMISA, a Lima-based environmental consulting company, and continued in collaboration with Anddes is ongoing. The Baseline Study was expanded to include each of the Falchani Lithium Project and Macusani Uranium Project areas and now covers the affected areas belonging to the communities of Isivilla, Tantamaco, Corani, Chimboya, Paquaje and Chacaconiza. This expanded Baseline Study was accepted by the Peruvian Government Agency SENACE (Servicio Nacional de Certificacion Ambiental) and built on previous environmental monitoring that was started by the Company in 2010. The Baseline Study has recently progressed into an EIA that includes community relations and impacts of future development, as well as flora, fauna, water, air and noise sampling and comprehensive archaeological studies.

Concessions Update

An administrative court in Lima, Peru, has granted one (1) of Macusani Yellowcake S.A.C.’s (“Macusani”) applications for an injunction, known as a Medida Cautelar (“Precautionary Measure”), against 17 of the administrative resolutions issued by the Mining Council of the Ministry of Energy and Mines (“MINEM”) in July 2019 (the “Concession Resolutions”). A full background and chronology of events, is available for review in news releases issued on July 31, 2019 and August 6, 2019.

The Precautionary Measure is granted via a judicial resolution through which the validity, rights and ownership of 171 of the 32 mining concessions are restored to Macusani as they were prior to the issuance of the Concession Resolutions. The Precautionary Measures are issued on a “temporary” basis for the duration of the legal process. The judicial resolution supports the Company’s assertions that Macusani made the 2017 annual validity rights payments for the concessions into the Institute of Geology Mining and Metallurgy’s (“INGEMMET”) bank account, complied with its legal obligations under Peru’s General Mining Law and INGEMMET did not comply with the Administrative Law. The INGEMMET database has been updated and currently shows 17 of the 32 concessions as valid. The judicial resolution has been opposed by INGEMMET, however, the restoration of the validity, rights and ownership will remain in place until there are no further appeals available.

It is anticipated that the application for Precautionary Measure for the remaining 152 concessions will be reviewed in front of the presiding judge that granted the first Precautionary Measure and management believes there is a reasonable expectation that the decision for the second Precautionary Measure will be consistent with the first Precautionary Measure as the arguments being presented will be the same as outlined in the successful first Precautionary Measure.

The Company expects to have a decision for the Precautionary Measure on the remaining 15 concessions shortly, and will provide updates as and when they become available.

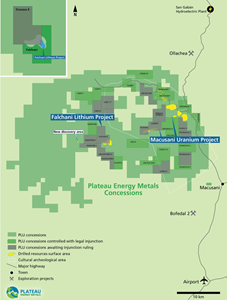

Figure 1: Plateau Mineral Concessions

Figure 1 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/c9159f22-e4b3-48dd-83e1-3c45baa5d76c

_____________________

1 The 17 concessions are: Sillatoco; Triunfador 5; Huiquiza 3; Lincoln XXIX; Lincoln XXVI; Tantamaco 7; Tantamaco II; Triunfador 3; Chilcuno; Chapi II; Colibrí I; Corani U2; Liocco; Samilio IV; Huarituña I; Chapi V; and Triunfador 1.

2 The 15 concessions are: Ocacasa 4; Triunfador 2; Chapi "U"; Tupuramani; Triunfador 4; Huarituña II; Huarituña 3; Tantamaco 6; Chachaconiza II; Chapi III; Colibri II; Samilio I; Lincoln XXXII; Porsiaca Estrella; Chachaconiza

Qualified Persons

Stewart Nupen, B.Sc. (Hons), FGSSA, Pr Sci Nat (No 400174/07) of The Mineral Corporation, South Africa, an independent mining consulting firm to the Company, is a Qualified Person as defined under NI 43-101, and has reviewed and approved the scientific and technical data pertaining to the Mineral Resource estimates contained in this release.

John Joseph Riordan, BSc, CEng, FAuslMM, MIChemE, RPEQ, of DRA Pacific (Pty) Ltd., an Independent Qualified Person as defined by NI 43-101 Standards of Disclosure for Mineral Projects, has reviewed and approved the scientific and technical metallurgical information contained in this news release.

Mr. Ted O’Connor, P.Geo., a Director and Technical Advisor to Plateau, is the Company’s designated Qualified Person as defined by NI 43-101, has reviewed and approved the scientific and technical information contained in this news release.

In accordance with NI 43-101, the Company intends to file the completed technical report on the PEA under the Company's profile on SEDAR (www.sedar.com) and on the Company's website within 45 days from the date of this news release.

About DRA Global

DRA Global is a diversified global engineering, project delivery and operations management group, with an impressive track record spanning more than three decades. With expertise in the areas of project development, mining, mineral processing, plant optimisation, operations & maintenance and related water, energy, and infrastructure requirements, DRA Global delivers comprehensive solutions to the resources sector. DRA, through its wholly owned subsidiary DRA Met-Chem, based in Montreal, as well as their regional offices in Perth, Johannesburg and Cape Town, possess significant lithium process and metallurgical experts who are able to identify and develop the process requirements, through flowsheet development to the selection of process equipment, in order to minimize costs and ensure overall plant efficiency.

Alternative Performance Measures

Items marked with a * in this news release are alternative performance measures. Alternative performance measures are furnished to provide additional information. These non-IFRS performance measures are included in this news release because the Company believes these statistics are key performance measures that provide investors, analysts and other stakeholders with additional information to understand the costs associated with the Project. These performance measures do not have a standard meaning within IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance in accordance with IFRS.

About Plateau Energy Metals

Plateau Energy Metals Inc., a Canadian exploration and development company, is enabling the new energy paradigm through exploring and developing its Falchani Lithium Project and its Macusani Uranium Project in southeastern Peru. The Company has significant and growing lithium resources and all reported uranium resources known in Peru, all of which are situated near infrastructure.

For further information, please contact:

Plateau Energy Metals Inc.

Alex Holmes, CEO & Director

+1-416-628-9600

IR@PlateauEnergyMetals.com

Facebook: www.facebook.com/pluenergy/

Twitter: www.twitter.com/pluenergy/

Website: www.PlateauEnergyMetals.com

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

Forward Looking Information: This news release contains certain forward-looking information and forward-looking statements (collectively “forward-looking statements”) within the meaning of applicable securities legislation and may include future-oriented financial information. All statements, other than statements of historical fact, are forward-looking statements. Forward-looking statements in this news release include, but are not limited to, statements with respect to: (i) the results of the PEA, including statements about the Base Case and Alternative Case, future Project opportunities, future mining methods, future operating and capital costs, the projected IRR, NPV, construction timelines, permit timelines and Plateau’s ability to receive the requisite permits; (ii) the outcome of the administrative process, the judicial process, and any and all future remedies pursued by Plateau and its subsidiary Macusani to resolve the title for 32 of its concessions; (iii) metallurgical testing and results; (iv) the economics and potential returns associated with the Falchani Project; (v) the estimation of mineral reserves and mineral resources; (vi) the technical viability of the Falchani Project; (vii) the market and future price of and demand for battery-grade lithium carbonate and other commodities; (viii) environmental impact of the Falchani Project; (ix) projected employment and other social benefits resulting from the Falchani Project; and (x) the ongoing ability to work cooperatively with stakeholders, including but not limited to local communities and all levels of government.

Forward-looking statements are frequently identified by such words as "may", "will", "plan", "expect", "anticipate", "estimate", "intend", “indicate”, “scheduled”, “projected”, “target”, “goal”, “potential”, “opportunity” “subject”, “efforts”, “option”, “outlook” and similar words, or the negative connotations thereof, referring to future events and results. Forward-looking statements are based on the current opinions and expectations of management. Although the Company believes that the current opinions and expectations reflected in such forward-looking statements are reasonable, undue reliance should not be placed on forward-looking statements since the Company can provide no assurance that such opinions and expectations will prove to be correct. All forward-looking statements are inherently uncertain and subject to a variety of assumptions, risks and uncertainties, including risks and uncertainties relating to the Falchani Project PEA and the results presented herein including risks and uncertainties related to but not limited to: the economics and potential returns associated with the Falchani Project, the projected IRR and NPV, the Base Case and Alternative Case, the estimation of mineral reserves and mineral resources included in the Falchani PEA, the technical viability of the Falchani Project, future mining methods, future operating and capital costs, metallurgical testing and results, the future Project opportunities, construction timelines, permit timelines and Plateau’s ability to receive the requisite permits, , delays or increased costs that may be encountered during the development process, the market and future price of battery-grade lithium carbonate, sulfuric acid and other commodities, increased competition in the market for battery-grade lithium carbonate and related products, environmental impact of the Falchani Project, projected employment and other social benefits resulting from the Falchani Project, the results of the PEA, including statements about future mining methods, future operating and capital costs, the projected IRR, NPV, construction timelines, permit timelines and Plateau’s ability to receive the requisite permits. Additional potential risks include, and are not limited to, the status of the “Precautionary Measures” filed by Macusani, the outcome of the administrative process, the judicial process, and any and all future remedies pursued by Plateau and its subsidiary Macusani to resolve the title for 32 of its concessions (see “Cautionary Note Regarding Concessions” below); the ongoing ability to work cooperatively with stakeholders, including but not limited to local communities and all levels of government; the interpretation of drill results, the geology, grade and continuity of mineral deposits; the possibility that any future exploration, development or mining results will not be consistent with our expectations; mining and development risks, including risks related to accidents, equipment breakdowns, labour disputes (including work stoppages and strikes) or other unanticipated difficulties with or interruptions in exploration and development; the potential for delays in exploration or development activities; risks related to commodity price and foreign exchange rate fluctuations; risks related to foreign operations; the cyclical nature of the industry in which we operate; risks related to failure to obtain adequate financing on a timely basis and on acceptable terms or delays in obtaining governmental approvals; risks related to environmental regulation and liability; political and regulatory risks associated with mining and exploration; risks related to the certainty of title to our properties; risks related to the uncertain global economic environment; and other risks and uncertainties related to our prospects, properties and business strategy as identified in the “Risks and Uncertainties” section of Plateau’s Management’s Discussion and Analysis filed on January 20, 2020 and described in more detail in Plateau’s recent securities filings available at www.sedar.com. Actual events or results may differ materially from those projected in the forward-looking statements and Plateau cautions against placing undue reliance thereon. Except as required by applicable securities legislation, neither Plateau nor its management assume any obligation to revise or update these forward-looking statements.

Cautionary Note Regarding Concessions: The Ocacasa 4 concession, which forms part of the mineral resources considered in the Base Case of the Falchani Project PEA, is currently subject to Administrative and Judicial processes (together, the “Processes”) in Peru to overturn resolutions issued by INGEMMET and the Mining Council of MINEM in February 2019 and July 2019, respectively, which declared Macusani’s title to the Ocacasa 4 concession invalid due to late receipt of the annual validity payment. In November 2019, the Company applied for injunctive relief on 32 concessions in a Court in Lima, Peru and was successful in obtaining such an injunction on 17 of the concessions. The grant of the Precautionary Measures (Medida Cautelars) has restored the title, rights and validity of those 17 concessions to Macusani until a final decision is obtained in at the last stage of the judicial process. A Precautionary Measure application was made at the same time for the remaining 15 concessions, including Ocacasa 4, however the process has been delayed due to various in-country factors. A date for the hearing has not yet been set, but the Company expects it should take place shortly. If the Company does not obtain a successful resolution of Processes, Macusani’s title to the Ocacasa 4 concession could be revoked and the Falchani Project would proceed as presented in the Alternative Case.

Cautionary Note Regarding Mineral Resource Estimates: Information regarding mineral resource estimates has been prepared in accordance with the requirements of Canadian securities laws, which differ from the requirements of United States Securities and Exchange Commission ("SEC") Industry Guide 7. In October 2018, the SEC approved final rules requiring comprehensive and detailed disclosure requirements for issuers with material mining operations. The provisions in Industry Guide 7 and Item 102 of Regulation S-K, have been replaced with a new subpart 1300 of Regulation S-K under the United States Securities Act and will become mandatory for SEC registrants after January 1, 2021. The changes adopted are intended to align the SEC's disclosure requirements more closely with global standards as embodied by the Committee for Mineral Reserves International Reporting Standards (CRIRSCO), including Canada's NI 43-101 and CIM Definition Standards. Under the new SEC rules, SEC registrants will be permitted to disclose "mineral resources" even though they reflect a lower level of certainty than mineral reserves. Additionally, under the New Rules, mineral resources must be classified as “measured”, “indicated”, or “inferred”, terms which are defined in and required to be disclosed by NI 43-101 for Canadian issuers and are not recognized under SEC Industry Guide 7. An “Inferred Mineral Resource” has a lower level of confidence than that applying to an “Indicated Mineral Resource” and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of “Inferred Mineral Resources” could be upgraded to “Indicated Mineral Resources” with continued exploration. Accordingly, the mineral resource estimates and related information may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements under the United States federal laws and the rules and regulations thereunder, including SEC Industry Guide 7.

Figure 1