Roxgold Delivers Robust PEA for the S?(C)gu?(C)la Gold Project With After-Tax NPV of $268 Million and 66% IRR

Roxgold Inc. (“Roxgold” or the “Company”) (TSX:ROXG) (OTCQX:ROGFF) is pleased to announce the results of a Preliminary Economic Assessment (“PEA”) for the high-grade Séguéla Gold Project (“Séguéla”) in Côte d’Ivoire. The PEA was prepared in accordance with Canadian Securities Administrators’ National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”). The PEA provides a base case assessment of developing the Antenna, Ancien, Agouti and Boulder deposits as open pit mines feeding a central gold processing facility. Roxgold expects to continue its evaluation of Séguéla with the intent of growing the resource base and advancing to the feasibility stage.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20200414005946/en/

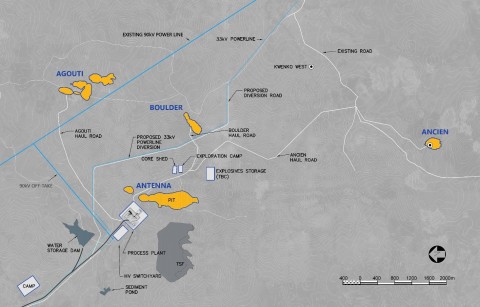

Séguéla Plan Infrastructure (Graphic: Business Wire)

A webcast and conference call to discuss the PEA results will be held on Wednesday, April 15th, 2019, at 8:00AM Eastern time – details of the call are outlined in the “Séguéla Gold Project PEA Conference Call” section below.

Key Highlights (all financial results are in U.S. dollars unless otherwise noted):

Production

- Life of Mine (“LOM”) gold production of 841,000 ounces with average annual gold production of 103,000 ounces

- Average annual gold production of 143,000 ounces over the first three years of production, with an estimated production peak of 154,000 ounces in year three

Costs

- Average cash costs1 of $605 per ounce over the LOM, including a cash cost of $475 per ounce over the first three years of production

- Average All-In Sustaining Costs (“AISC”)1 of $749 per ounce over the LOM, including an AISC of $600 per ounce over the first three years of production

Development Capital

- Estimated pre-production capital cost of $142 million (including a $20 million contingency)

- Conventional processing plant with a processing rate of 1.25 million tonnes per year with scalability incorporated into plant design for potential expansion

Financial

- LOM after-tax net cash flow of $354 million at a gold price of $1,450 per ounce

- Project payback of 1.2 years

- Robust economics with net present value (“NPV”) and internal rate of return (“IRR”) of:

Metric |

Base Case @

|

Spot Price @

|

NPV5% after-tax – attributable to Roxgold’s 90% interest |

$268 million |

$379 million |

After tax IRR |

66% |

88% |

John Dorward, President and Chief Executive Officer commented: “The PEA illustrates the substantial value accretion of the Séguéla Gold Project which stands alongside our current operations to build the foundation for Roxgold and its future. We acquired Séguéla in April 2019 for $20 million, and through the hard work of our exploration and project team have been able to generate exceptional prospective project economics with an after-tax NPV attributable to Roxgold of $268 million and an IRR of 66% at a gold price of $1,450/oz. In the first three years of operation, the project will produce an average of 143,000 ounces of gold per year at an AISC of $600 per ounce ensuring a payback period of only 1.2 years.

“Importantly, this assessment is just a snapshot of the potential value of Séguéla. Our exploration program has returned material intersections from five of the first seven targets identified, with an additional 21 targets on the property yet to be tested. It is our belief that, with continued drilling success, there is the potential to add significant production ounces and value to the project. Additionally, we have identified several opportunities to expand and optimize the PEA, which we intend to evaluate as we proceed towards a Feasibility Study, which is well underway and with an anticipated completion in the first half of 2021.”

The PEA is preliminary in nature, includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Table 1 – PEA Summary

Metrics |

Units |

Results |

Life of Mine |

years |

8.2 |

Total mineralized material mined |

tonnes |

10,241,000 |

Contained gold in mined resource |

oz |

890,000 |

Strip ratio |

w:o |

8.1:1 |

Throughput |

tpd |

3,500 |

Head grade |

g/t |

2.7 |

Recoveries |

% |

94.5% |

Gold production |

|

|

Total production over LOM |

oz |

841,000 |

Annual production over LOM |

oz |

103,000 |

Annual production over first 3 years |

oz |

143,000 |

Operating costs over LOM |

|

|

Mining |

$/t, mined |

$3.02 |

Processing |

$/t, processed |

$15.55 |

G&A |

$/t, processed |

$5.85 |

Others (incl. refining and royalties) |

$/t, processed |

$7.35 |

Total Operating Costs |

$/t, processed |

$56.30 |

Cash costs1 |

|

|

Average cash costs over LOM |

$/oz |

$605 |

Average cash costs over first 3 years |

$/oz |

$475 |

AISC1 |

|

|

Average AISC over LOM |

$/oz |

$749 |

Average AISC over first 3 years |

$/oz |

$600 |

Capital costs |

|

|

Initial capital expenditure |

$M |

$142 |

Sustaining capital expenditure |

$M |

$36 |

NPV5%, after-tax – attributable to Roxgold’s 90% interest |

$M |

$268 |

After-tax IRR |

% |

66% |

Payback Period |

years |

1.2 |

Annual EBITDA |

|

|

Average EBITDA over LOM |

$M |

$76 |

Average EBITDA over first 3 years |

$M |

$125 |

Séguéla Gold Project Overview

The Séguéla Gold Project is located approximately 240 kilometres north-west of Yamoussoukro, the political capital of Côte d'Ivoire, and approximately 480 kilometres north-west of Abidjan, the commercial capital of the country. The Séguéla property covers an area of 36,300 hectares, defined by two exploration permits. The property is generally accessible year-round by road vehicle. Bituminised national highways facilitate transport between Abidjan, Yamoussoukro and the town of Séguéla (population 65,000) which is the nearest major town to the property. The project is accessible from the town of Séguéla via approximately 20 km of dirt roads.

Mineral Resources Estimate

The Séguéla Mineral Resource used for the PEA includes the Antenna, Ancien, Agouti and Boulder deposits reported in Table 2. Roxgold completed an updated Mineral Resource estimate for the Ancien deposit, based on the drillhole data cut-off of February 12th, 2020. The Antenna, Agouti and Boulder Mineral Resource estimates are unchanged since the previous reported Mineral Resource in the technical report entitled “NI 43-101 Technical Report, Séguéla Project, Worodougou Region, Cote d’Ivoire” with an effective report date of January 29th, 2020 which is available on SEDAR at www.sedar.com.

The Séguéla Mineral Resource estimate incorporates data from all Reverse Circulation (“RC”) and Diamond Drilling (“DD”) drilling prior to the cut-off, comprising 51,463 metres in 348 drillholes targeting Antenna, Ancien, Agouti, and Boulder. Roxgold completed 20,403 metres of RC and DD drilling since the acquisition of the Séguéla Project in April 2019.

Table 2 – Séguéla Mineral Resource Statement Summary

|

Measured |

Indicated |

Measured & Indicated |

Inferred |

||||||||

Tonnes |

Grade |

Metal |

Tonnes |

Grade |

Metal |

Tonnes |

Grade |

Metal |

Tonnes |

Grade |

Metal |

|

(Mt) |

(g/t Au) |

(000 oz) |

(Mt) |

(g/t Au) |

(000 oz) |

(Mt) |

(g/t Au) |

(000 oz) |

(Mt) |

(g/t Au) |

(000 oz) |

|

Antenna |

- |

- |

- |

7.1 |

2.3 |

529 |

7.1 |

2.3 |

529 |

0.9 |

2.2 |

64 |

Ancien |

- |

- |

- |

- |

- |

- |

- |

- |

- |

1.3 |

6.1 |

261 |

Agouti |

- |

- |

- |

- |

- |

- |

- |

- |

- |

1.3 |

2.6 |

110 |

Boulder |

- |

- |

- |

- |

- |

- |

- |

- |

- |

1.9 |

1.2 |

72 |

Total |

- |

- |

- |

7.1 |

2.3 |

529 |

7.1 |

2.3 |

529 |

5.4 |

2.9 |

508 |

Notes:

- Mineral Resources are reported in accordance with NI 43-101 with an effective date of April 14th 2020, for Séguéla.

- The Séguéla Mineral Resources are reported on a 100% basis at a gold grade cut-off of 0.3 g/t Au for Antenna and 0.5 g/t Au for the satellite deposits, based on a gold price of US$1,550/ounce and constrained to MII preliminary pit shells.

- The identified Mineral Resources in the block model are classified according to the “CIM” definitions for the Measured, Indicated, and Inferred categories. The Mineral Resources are reported in situ without modifying factors applied.

- The Séguéla Mineral Resource Statement was prepared under the supervision of Mr. Hans Andersen, Senior Resource Geologist at Roxgold Inc. Mr. Andersen is a Qualified Person as defined in NI 43-101.

- All figures have been rounded to reflect the relative accuracy of the estimates and totals may not add due to rounding.

- Mineral Resources that are not Mineral Reserves do not necessarily demonstrate economic viability.

Preliminary Economic Assessment

Roxgold has worked in collaboration with various consultants to prepare the PEA. The objective was to demonstrate the economic viability of developing multiple open pit mines in proximity to a central processing facility targeting the indicated and inferred Mineral Resources across multiple deposits. This news release provides a summary of the results and findings from each major area of investigation. The level of investigation for each of these areas is consistent with that normally expected with preliminary economic assessments for mineral resource development projects. An NI 43-101 technical report prepared by Roxgold will be filed on SEDAR within 45 days of this news release providing further detail including exploration, geological modelling, Mineral Resource estimation, mine design, process design, infrastructure design, environmental management, capital and operating costs and economic analysis.

The financial analysis performed from the results of this PEA demonstrates the economic viability of the proposed Séguéla Gold Project using the base case assumptions considered. This results in an after-tax net present value cashflow at a 5% discount rate (NPV5%) of $268 million (attributable to Roxgold 90% interest) and an after-tax IRR of 66%. Also considered are opportunities to further strengthen and enhance the project’s economic foundation. Séguéla has become the Company’s highest priority initiative and considering the outstanding potential economics, the project is advancing to the next phase and definition of a Feasibility Study, as well continued drilling designed to expand the size of the existing mineral resource base and test new targets.

Figure 1: Séguéla Plan of Infrastructure

Mining and Recovery Methods

Mining

The Séguéla Gold Project will consist of the simultaneous exploitation of the Antenna deposit and its satellite deposits: Ancien, Agouti, and Boulder. The overall strategy is to have production from these satellite deposits complement the production from Antenna to achieve a total production rate of 1.25 million tonnes per annum (“Mtpa”). The project mine life contemplated in the PEA is eight years.

Mining activities at Séguéla will utilize conventional open-pit mining methods. Drill and blasting are planned for oxide and fresh mineralized material, followed by conventional truck and shovel operations within the pits for the movement of mineralized material and waste. Two 125 tonne (“t”) excavators, complimented with two 65 tonne excavators in the latter stages of the satellite pits, with an estimated total material productive capacity of approximately 8.0 Mtpa, will have sufficient capacity to allow for maintenance, transport between the pits, and make-up capacity to account for low productivity periods such as high rainfall events. A fleet of up to nine Caterpillar 777 trucks (payload of 100 t) will be used in conjunction with several smaller articulated trucks for the latter stages of the satellite pits to truck and haul all mineralized and waste material. Roxgold will engage a mining contractor for the mining of all the deposits over the mine life, several of which provided quotes that were incorporated in the mining cost assumptions in the PEA. A common pool of equipment will be used and scheduled across all active pits so that movement between the pits is minimised.

Figure 2: Séguéla PEA production profile

Run of Mine (“ROM”) mineralized material will be trucked from the pit to the ROM pad and dumped either onto the ROM pad to be reclaimed and loaded to the ROM bin or by direct tipping. The PEA contemplates a single stage primary crush/SAG milling comminution circuit where the mineralized material will be drawn from the ROM bin via an apron feeder, scalped via a vibrating grizzly with the undersize reporting directly to the discharge conveyor and the oversize reporting to a primary jaw crusher for further size reduction. All crushed and scalped material will by conveyed to a surge bin. Crushed mineralized material and water will be fed to the mill.

Processing

The mill will operate in closed circuit with hydrocyclones, with cyclone underflow reporting to the mill feed. A portion of the cyclone underflow slurry will be fed to the gravity circuit for recovery of gravity gold. The gravity concentrator tailings will flow to the cyclone feed hopper, while the gravity concentrate will report to an intensive leach circuit. Gold in solution will be recovered in a dedicated electrowinning system.

Screened cyclone overflow will be thickened prior to the Carbon-in-Leach (“CIL”) circuit. Loaded carbon drawn from the CIL circuit will be stripped by the Zadra method. The resultant gold in solution will be recovered by electrowinning. Recovered gold from the cathodes will be filtered, dried and smelted in a furnace to doré bars.

The PEA assumes a forecast gold recovery rate of 94.5% for the life of the production plan.

Selected operating and production statistics from the PEA are presented in Table 3.

Table 3 – Estimated PEA annual operating statistics

Units |

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

LOM |

|

Tonnes mined |

Kt |

698 |

9,956 |

14,353 |

14,734 |

16,098 |

12,327 |

9,787 |

8,955 |

6,624 |

0 |

93,531 |

Tonnes milled |

Kt |

- |

1,250 |

1,250 |

1,250 |

1,250 |

1,250 |

1,250 |

1,250 |

1,250 |

241 |

10,241 |

Head grade |

g/t |

- |

3.76 |

3.48 |

4.05 |

2.49 |

1.90 |

2.20 |

2.22 |

1.73 |

1.73 |

2.70 |

Recovery |

% |

- |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

94.5% |

Gold production |

koz |

- |

143 |

132 |

154 |

95 |

72 |

84 |

84 |

66 |

13 |

841 |

Metallurgy

Metallurgical testing was performed at the ALS Metallurgy laboratory in Perth, Western Australia, Australia under the supervision of Roxgold. A significant amount of testing was performed on the Antenna deposit, which is mineralogically representative of the other satellite deposits while hosting the majority of the project’s Mineral Resource and will account for the majority of mill feed material in the first five years of operation. In addition to the Antenna deposit, a comprehensive testwork program targeting recovery variability on the satellite deposits (Ancien, Agouti and Boulder) was conducted. The key results are summarized in Table 4.

The testwork included the following:

-

Comminution test work, including:

- Bond impact crushing work index (CWi) determination

- SMC testwork

- Bond abrasion index (Ai) determination

- Bond rod mill work index (RWi) determination

- Bond ball mill work index (BWi) determination

- Head assays

- Mineralogical analysis

- Grind establishment testwork

- Gravity gold recovery and cyanide leach testwork

- Flotation testwork.

Table 4 – Key results from the Antenna metallurgical testwork program

Test |

Range of Results |

Average Result |

Calculated Head Assay (g/t Au) |

1.62 g/t Au – 10.3 g/t Au |

3.1 g/t |

Overall Gold Extraction (%) |

92.0% – 97.1% |

94.5% |

Gravity Gold Recovery (%) |

28% – 60% |

38% |

Cyanide Consumption (kg/t) |

0.09 – 0.30 kg/t |

0.20 kg/t |

Lime Consumption (kg/t) |

0.27 kg/t – 1.96 kg/t |

0.45 kg/t |

Samples tested for Antenna were reasonably competent with Bond Rod and Ball Mill Work Indices of 22.7kWh/t and 19.7 kWh/t respectively, being amenable to a simple comminution circuit design. The mineralized material tested exhibited a degree of grind sensitivity with an optimal grind size of 75 micron being selected for all extraction test work. The results of that program, which tested 14 separate samples from Antenna, were very encouraging, indicating potential for free milling of the mineralized material with good leach kinetics and overall extractions. The three satellite deposits returned positive results when tested at the same criteria. Overall recoveries in excess of 95% with gravity recoveries averaging 40%, indicating that the metallurgical characteristics of the satellite deposits are very similar to those seen at Antenna.

Taken together, Roxgold believes that with the process plant and recovery methods contemplated in the PEA an average gold recovery of 94.5% can be assumed. Further testwork will be done as part of the Feasibility Study phase of the project to validate and expand upon these results and process design criteria.

Tailings & Power

It is intended that the CIL tails will be treated to reduce the Weak Acid Dissociable cyanide level to an environmentally acceptable level. The tailings system will comprise of two parallel tailings lines and associated tailings pumps. The tailings storage facility (“TSF”) will comprise a side-valley storage formed by two multi-zoned earth-fill embankments, designed to accommodate 13.0 Mt of tailings and built utilising the downstream construction methodology.

A water harvesting and storage dam will be the main collection and storage pond for clean raw and process water.

The envisioned power supply is through a connection to the Côte d’Ivoire electricity grid by a 2,400 m tee into the 90kV powerline from the Laboa to Séguéla substation. The Séguéla substation is fed via an existing 90kV transmission line from the 225/90kV Laboa substation. The Laboa substation is part of a 225kV ring main system around the country where various sources of generation are connected and, being a large ring main, offers a great deal of redundancy at 225kV. The grid supply from Côte d’Ivoire is, by world standards, economically priced and much more financially favourable than other options including self-generation as the tariff is based on a mix of hydro and thermal generation with a large portion of hydro.

Environmental and Permitting

The primary environmental approval required to develop Séguéla is decreed by the Ivorian Environment Minister and is necessary for the issuance of the mining license. Roxgold has contracted the consulting firm CECAF to undertake the project baseline studies and compile the environmental and social impact assessment (“ESIA”) required to obtain the environmental decree. The ESIA will identify the potential social and environmental impacts of the development of the project and proposed mitigation measures. Separate to the ESIA, a Resettlement Action Plan (“RAP”) will be developed for any physical or economic displacement of people or communities as a result of the project’s development. As there are no specific regulations or guidelines in Côte d’Ivoire, the RAP will largely follow the guidelines specified in the International Finance Corporation (“IFC”) Performance Standard 5 (PS5). The Séguéla project does not have any permanent settlements in the project area and as such, it is anticipated that the RAP will outline low impact measures.

Currently, there is no permanent artisanal mining (“ASM”) settlement on the identified deposits or nearby, with the presence of only a few hundred of ASM miners from time to time in the project area. The implementation of a stakeholder management plan, as undertaken by the Company elsewhere in the region, should enable the ASM activities in the project area to be effectively managed.

The conceptual closure plan considered in the PEA assumes the mine areas will be reclaimed to a safe and environmentally sound condition consistent with closure commitments developed during the life of the project in compliance with the national regulations and IFC standards and other best practices.

The PEA assumes that all requisite approvals and permits for the expansion will be obtained. While it is believed that such approvals and permits can be obtained on a timely basis and on acceptable terms, there is no certainty that this will be the case.

Capital Costs Summary

The capital required to develop Séguéla is estimated to be $142 million (including $20 million contingency) with an additional $36 million of sustaining capital and $11.5 million of closure costs over the eight-year mine life. The mining production capital relates to mining activities prior to first material being delivered to the processing facility, where 301,000 tonnes of mineralized material and 397,000 tonnes of waste are mined in order to establish a reasonable stockpile ahead of operations commencing. All contractor mobilization and setup are included in the pre-production capital allowance.

The processing plant capital relates to a facility with a nominal throughout of 1.25 Mtpa. The capital cost estimate is based on an engineering, procurement and construction management (“EPCM”) implementation approach and horizontal (discipline based) construction contract packaging. Equipment pricing was based on actual equipment costs from other recent similar scale Lycopodium projects and considered representative for Séguéla.

The surface infrastructure includes site electrical distribution, tailings management facility, water dams and accommodation camp. A summary of estimated capital costs is presented in Table 5 and annual estimated capital costs are shown in Table 6. Capital cost estimates in the PEA reflect the joint efforts of Knight Piésold Consulting, Lycopodium Limited, CSA Global Pty Ltd., ECG and Roxgold. Roxgold compiled the capital cost data into the overall cost estimate. Table 7 outlines the responsibilities of each contributor to the cost estimates.

Table 5 – Summary of PEA development capital costs

Capital Costs |

Value ($M) |

Design & Permitting |

$3.0 |

Mining |

$2.4 |

Processing |

$74.5 |

Infrastructure and Environment |

$34.6 |

G&A |

$7.4 |

Contingency |

$20.3 |

Total |

$142.2 |

Table 6 – Estimated annual sustaining capital costs

Year |

Units |

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Year

|

Mining |

$M |

3.8 |

0.4 |

0.4 |

2.6 |

0.4 |

0.4 |

0.7 |

0.4 |

- |

Processing |

$M |

0.7 |

0.7 |

0.7 |

0.7 |

0.7 |

0.7 |

0.7 |

0.7 |

0.1 |

Infrastructure & Environment |

$M |

3.0 |

2.7 |

2.9 |

2.7 |

2.7 |

3.0 |

2.7 |

0.5 |

0.5 |

Closure |

$M |

- |

- |

- |

- |

- |

- |

- |

- |

11.5 |

Total |

$M |

$7.5 |

$3.8 |

$4.0 |

$6.0 |

$3.8 |

$4.1 |

$4.1 |

$1.6 |

$12.1 |

Table 7 – Cost estimate contributions

Company |

Responsibility |

|

CSA Global Pty Ltd. |

Design and estimates for development and sustaining capital for the open pit mines in conjunction with budget pricing from prospective open pit mining contractors |

|

Lycopodium Limited |

Design and estimate for the processing plant and site access infrastructure |

|

Knight Piésold Consulting |

Design and estimate for the tailings storage facility and water storage and harvest dams |

|

ECG |

Design and estimate for the site power supply / grid connection |

|

Roxgold Inc. |

Owner's costs and miscellaneous surface infrastructure not captured in the scope of work of the consultants |

Operating Costs Summary

Cash costs and AISC per payable ounce of gold sold are non-GAAP financial measures. Please see “Cautionary Note Regarding Non-GAAP Measures”.

Total estimated cash costs in the PEA are presented in Table 8. The mining operating costs were developed based on quotes from reputable mining contractors, with experience in West Africa, including current operating experience in Côte d’Ivoire, and based on the mine plan for the Antenna deposit. The costs and productivity estimates have been validated against CSA Global’s internal database of similar benchmarked operations in West Africa. The processing operating costs were developed from first principles and Lycopodium’s database according to typical industry standards applicable to gold processing plants in West Africa. General and administration costs were factored from historical operating cost data from the development and operation of Roxgold’s Yaramoko Gold Mine in Burkina Faso.

Table 8 – PEA Operating Cash Costs

Cash Costs |

Value ($/t milled) |

Mining |

$27.56 |

Processing |

$15.55 |

General and Administrative |

$5.85 |

Refining |

$0.29 |

Total |

$49.24 |

As summarized in Table 9, operating costs, which includes mining, processing, general and administrative costs, royalties and refining costs totals $692 per payable ounce of gold sold over the eight-year operating plan in the PEA. AISC, which includes sustaining capital, reclamation, and corporate general and administration totals $749 per payable ounce of gold sold over the eight-year operating plan in the PEA.

Table 9 – Life of Mine All-In Sustaining Cost and All-In Cost

$M |

$/t milled |

$/payable oz |

|

Operating Cost |

|||

Mining |

$282 |

$27.56 |

$339 |

Processing |

159 |

15.55 |

191 |

G&A |

60 |

5.85 |

72 |

Refining |

3 |

0.29 |

4 |

Subtotal, Direct Operating Costs |

$504 |

$49.24 |

$605 |

Royalties |

66 |

6.47 |

80 |

Social Fund |

6 |

0.59 |

7 |

Total Operating Costs1 |

$577 |

$56.30 |

$692 |

Sustaining Capital, and Reclamation |

|||

Mining |

$9 |

$0.87 |

$11 |

Processing |

6 |

0.60 |

7 |

Infrastructure and Environment |

21 |

2.00 |

25 |

Closure |

11 |

1.12 |

14 |

All-in Sustaining Cost1 |

$624 |

$60.89 |

$749 |

Development Capital Cost |

|||

Design & Permitting |

$3 |

$0.29 |

$4 |

Mining |

2 |

0.24 |

3 |

Processing |

75 |

7.28 |

89 |

Infrastructure and Environment |

35 |

3.38 |

42 |

G&A |

7 |

0.72 |

9 |

Contingency |

20 |

1.98 |

24 |

Capital Expenditures (non-sustaining) |

$142 |

$13.88 |

$171 |

All-in Cost1 |

$766 |

$74.77 |

$919 |

Financial Analysis

The Séguéla Gold Project has been evaluated on a discounted cash flow basis. The results of the analysis show the project to be economically very robust. The pre-tax net present value with a 5% discount rate (NPV5%) is $335 million and with an IRR of 74% using a base gold price of $1,450/oz. The economic analysis assumes that Roxgold will provide all development funding via inter-company loans to the mine operating entity, which will be repaid with interest from future gold sales. On this basis, over the eight-year operating mine plan outlined in the PEA, Roxgold’s 90% interest in the project is expected to provide an after-tax NPV5% of $268 million and an IRR of 66% at a gold price of $1,450/oz.

Payback period is expected to be 1.2-years at a gold price of $1,450/oz. Payback period is defined as the time after process plant start-up that is required to recover the initial expenditures incurred developing the Séguéla Gold Project.

Table 10 – Key PEA Financial Estimates

|

Units |

LOM Total |

Gold Revenue |

|

|

Gold Price |

$/oz |

1,450 |

Gold Sales |

000 oz |

833 |

Gold Sales Revenue |

$M |

1,208 |

Operating Costs |

|

|

Mining |

$M |

(282) |

Processing |

$M |

(159) |

G&A |

$M |

(60) |

Gold Refining |

$M |

(3) |

Total Opex excluding Royalties and Social Fund |

$M |

(504) |

Royalties |

$M |

(66) |

Social Fund |

$M |

(6) |

Total Opex including Royalties and Social Fund |

$M |

(577) |

Capital and Closure Costs |

|

|

Development Capital |

$M |

(142) |

Sustaining Capital |

$M |

(36) |

Closure |

$M |

(11) |

Total Capital and Closure Costs |

$M |

(189) |

Project Valuation |

|

|

Project Net Cash Flow, pre-tax |

$M |

442 |

NPV5% |

$M |

335 |

IRR |

% |

74% |

Payback Period |

years |

1.1 |

Attributable Net Cash Flow, after-tax |

$M |

354 |

NPV5% – attributable to Roxgold’s 90% interest |

$M |

268 |

IRR |

% |

66% |

Payback Period |

years |

1.2 |

Note: Figures may not total exactly due to rounding |

||

Table 11 – Key Economic Assumptions

Unit |

Value |

|

Currency |

USD |

|

Gold Price |

$/oz |

1,450 |

Gold Payable |

% |

99.0 |

Mill Recovery |

% |

94.5 |

Base Case Discount Rate |

% |

5.0 |

Exchange Rate |

||

EUR to USD |

1.1065 |

|

XOF to USD |

0.0017 |

|

Royalty |

||

1,100 $/oz |

% |

3.0 |

1,300 $/oz |

% |

3.5 |

1,600 $/oz |

% |

4.0 |

2,000 $/oz |

% |

5.6 |

>2,000 $/oz |

% |

6.0 |

Vendor Royalties |

% |

1.5 |

Social Fund |

% |

0.5 |

Sensitivity Analysis

The Séguéla Gold Project contemplated in the PEA demonstrates strong economic performance across a range of variables. Estimated NPV sensitivities for key operating and economic metrics are presented in Table 12, Table 13, Table 14 and Figure 3.

Table 12 – After-tax NPV (for Roxgold’s 90% interest) sensitivity to discount rate and gold price

Gold Price |

||||||

$1,050/oz |

$1,250/oz |

$1,450/oz |

$1,650/oz |

$1,850/oz |

||

Discount

|

5.0% |

$86 |

$183 |

$268 |

$344 |

$431 |

7.5% |

$69 |

$157 |

$234 |

$303 |

$381 |

|

10.0% |

$54 |

$135 |

$205 |

$268 |

$339 |

|

Table 13 – After-tax IRR sensitivity to gold price

Gold Price |

|||||

$1,050/oz |

$1,250/oz |

$1,450/oz |

$1,650/oz |

$1,850/oz |

|

IRR |

25% |

47% |

66% |

81% |

98% |

Table 14 – After-tax NPV5% sensitivity to capital costs and operating costs

Operating Costs |

||||||

-25% |

-10% |

0% |

10% |

25% |

||

Capital

|

-25% |

$362 |

$320 |

$292 |

$264 |

$223 |

-10% |

$348 |

$306 |

$278 |

$250 |

$209 |

|

0% |

$338 |

$296 |

$268 |

$240 |

$199 |

|

10% |

$328 |

$286 |

$258 |

$231 |

$190 |

|

25% |

$314 |

$272 |

$244 |

$216 |

$175 |

|

Figure 3: After-tax NPV5% sensitivities

Opportunities and Next Steps

Several potential opportunities to improve the economics of the Séguéla Gold Project contemplated under the PEA have been identified. Examples include, but may not be limited to:

- Séguéla presents a significant opportunity to further assess multiple priority exploration targets within 15 kilometres of the envisioned central processing facility. These targets have the potential to increase the mineral resource base and enhance the potential economics of the Séguéla project by adding additional ounces;

- Exploration potential to increase the mineral resources of the Antenna, Ancien, Agouti, and Boulder deposits;

- Optimize infrastructure (e.g. TSF, processing facility, etc.) designs resulting in reduced capital costs;

- Further optimize mining strategy resulting in operating cost savings; and

- Further optimize mine designs and scheduling resulting in fully utilized contractor fleet.

Analysis of the results and findings from each major area of investigation suggests several recommendations for further investigations during the upcoming Feasibility study to mitigate risks and improve the base case project definition to be incorporated during the development and operation of the project, including:

- Conduct a thorough geotechnical and hydrogeology investigation for each deposit;

- Additional metallurgical variability test work to confirm recovery assumptions;

- Tender the major construction (e.g. bulk earthworks, EPCM) and mining contracts to more accurately define the project costs and economics;

- Infill drilling and conversion of Mineral Resources to Mineral Reserves;

- Advance the ESIA, RAP, and mining permit processes;

- Continue ongoing environmental (e.g. climate, noise, water quality, etc.) testing and monitoring;

- Develop a detailed project implementation plan to precisely define the strategy that will be executed to develop the project successfully.

- Additional geochemical testing of the tailings and waste rock to confirm the Acid Rock Drainage (ARD) and Metal Leaching (ML) potential;

- Continue to engage effectively with all the stakeholders as the project develops; and

- Develop an approach and procedure for the land access associated with the RAP.

Given the positive financial analysis included in the PEA, we expect to advance further exploration, study and engineering work on Séguéla.

Séguéla Gold Project PEA Conference Call

A webcast and conference call to discuss the Séguéla PEA results will be held on Wednesday, April 15th, 2020, at 8:00AM Eastern time. Listeners may access a live webcast of the conference call from the events section of the Company’s website at www.roxgold.com or by dialing toll free 1-844-607-4367 within North America or 1-825-312-2266 from international locations and entering passcode: 886 9387.

An online archive of the webcast will be available by accessing the Company’s website at www.roxgold.com. A telephone replay will be available for two weeks after the call by dialing toll free 1-800-585-8367 and entering passcode: 886 9387.

Notes:

- Cash costs and AISC per payable ounce of gold sold are non-GAAP financial measures. Please see “Cautionary Note Regarding Non-GAAP Measures”. All-in Sustaining Costs are presented as defined by the World Gold Council less Corporate G&A.

Qualified Persons

The scientific and technical information contained in this news release has been reviewed and approved by the following qualified persons under NI 43-101:

Paul Criddle, FAusIMM, Chief Operating Officer for Roxgold, a Qualified Person within the meaning of NI 43-101, has reviewed, verified and approved the scientific and technical disclosure contained in this news release.

The scientific and technical information contained in this document relating to Séguéla’s Mineral Resource is based on, and fairly represents, information compiled by Hans Andersen. Mr. Andersen, MAIG, is a Member of the Australian Institute of Geoscientists. Mr. Andersen has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a “Qualified Person” under NI 43-101. Mr. Andersen has consented to and approved the inclusion in this document of the matters based on his compiled information in the form and context in which it appears in this document.

Both Mr. Criddle and Mr. Andersen are full-time employees of Roxgold and are not “independent” within the meaning of NI 43-101.

Roxgold’s disclosure of Mineral Reserve and Mineral Resource information is governed by NI 43-101 under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as may be amended from time to time by the CIM (“CIM Standards”). There can be no assurance that those portions of Mineral Resources that are not Mineral Reserves will ultimately be converted into Mineral Reserves.

The qualified persons have verified the information disclosed herein, including the sampling, preparation, security and analytical procedures underlying such information, and are not aware of any significant risks and uncertainties that could be expected to affect the reliability or confidence in the information discussed herein.

National Instrument 43-101 Technical Report

A NI 43-101 technical report prepared by Roxgold will be filed on SEDAR at www.sedar.com within 45 days of this news release and will be available at that time on the Roxgold website.

About Roxgold

Roxgold is a Canadian-based gold mining company with assets located in West Africa. The Company owns and operates the high-grade Yaramoko Gold Mine located on the Houndé greenstone belt in Burkina Faso and is advancing the development and exploration of the Séguéla Gold Project located in Côte d’Ivoire. Roxgold trades on the TSX under the symbol ROXG and as ROGFF on OTCQX.

Cautionary Note Regarding Forward-Looking Statements

This news release contains “forward-looking information” within the meaning of applicable Canadian securities laws (“forward-looking statements”). Such forward-looking statements include, without limitation: economic statements related to the PEA, such as future projected production, capital costs and operating costs, statements with respect to Mineral Reserves and Mineral Resource estimates, recovery rates, timing of future studies including the feasibility study, environmental assessments and development plans. These statements are based on information currently available to the Company and the Company provides no assurance that actual results will meet management's expectations. In certain cases, forward-looking information may be identified by such terms as "anticipates", "believes", "could", "estimates", "expects", "may", "shall", "will", or "would". Forward-looking information contained in this news release is based on certain factors and assumptions regarding, among other things, the PEA, the estimation of Mineral Resources and Mineral Reserves, the realization of resource estimates and reserve estimates, any potential upgrades of existing resource estimates, gold metal prices, the timing and amount of future exploration and development expenditures, the estimation of initial and sustaining capital requirements, the estimation of labour and operating costs, the availability of necessary financing and materials to continue to explore and develop the Company’s properties in the short and long-term, the progress of exploration and development activities, the receipt of necessary regulatory approvals, and assumptions with respect to currency fluctuations, environmental risks, title disputes or claims, and other similar matters. While the Company considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect.

Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include: delays resulting from the COVID-19 pandemic, changes in market conditions, unsuccessful exploration results, possibility of project cost overruns or unanticipated costs and expenses, changes in the costs and timing of the development of new deposits, inaccurate reserve and resource estimates, changes in the price of gold, unanticipated changes in key management personnel and general economic conditions. Mining exploration and development is an inherently risky business. Accordingly, actual events may differ materially from those projected in the forward-looking statements. This list is not exhaustive of the factors that may affect any of the Company's forward-looking statements, including the factors included in the Company’s annual information form for the year ended December 31, 2019. These and other factors should be considered carefully and readers should not place undue reliance on the Company's forward-looking statements. The Company does not undertake to update any forward-looking statement that may be made from time to time by the Company or on its behalf, except in accordance with applicable securities laws.

Cautionary Note Regarding Non-GAAP Measures

This news release includes certain terms or performance measures commonly used in the mining industry that are not defined under International Financial Reporting Standards (“IFRS”), including cash costs and AISC per payable ounce of gold sold. Non-GAAP measures do not have any standardized meaning prescribed under IFRS and, therefore, they may not be comparable to similar measures employed by other companies. We believe that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate our performance. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Readers should also refer to our management’s discussion and analysis, available under our corporate profile at www.sedar.com for a more detailed discussion of how we calculate such measures.

View source version on businesswire.com: https://www.businesswire.com/news/home/20200414005946/en/