Taseko Reports Third Quarter 2024 Operational Performance and $48 Million of Adjusted EBITDA

| This release should be read with the Company’s Financial Statements and Management Discussion & Analysis ("MD&A"), available at www.tasekomines.com and filed on www.sedarplus.com. Except where otherwise noted, all currency amounts are stated in Canadian dollars. In March 2024 Taseko acquired the remaining 12.5% interest and now owns 100% of the Gibraltar Mine, located north of the City of Williams Lake in south-central British Columbia. Production and sales volumes stated in this release are on a 100% basis unless otherwise indicated. | |

VANCOUVER, British Columbia, Nov. 06, 2024 (GLOBE NEWSWIRE) -- Taseko Mines Limited (TSX: TKO; NYSE American: TGB; LSE: TKO) ("Taseko" or the "Company") reports third quarter 2024 Adjusted EBITDA* of $48 million and Earnings from mining operations before depletion, amortization and non-recurring items* of $55 million. Revenues for the third quarter were $156 million from the sale of 26 million pounds of copper and 348 thousand pounds of molybdenum. A net loss of $0.2 million ($nil per share) was recorded for the quarter and adjusted net income* was $8 million ($0.03 per share).

Gibraltar produced 27 million pounds of copper and 421 thousand pounds of molybdenum in the third quarter. Copper grades were 0.23%, consistent with the prior quarter. Tons milled increased over the second quarter, however mill availability and throughput was lower than planned due to unscheduled downtime and the completion of the crusher move project and concurrent maintenance in concentrator #1 in July. Copper recoveries increased modestly to 79%. Molybdenum production was boosted by a 33% increase in grades, related to ore from the new Connector pit. Total operating costs (C1)* for the quarter were US$2.92 per pound of copper produced.

Stuart McDonald, President and CEO of Taseko, commented, “The development of the new Connector pit advanced on plan in the third quarter, with the new pit providing approximately half of the mill feed in the period. Due to the lower than planned mill availability in the third quarter, we do not expect to recover the production that was lost during the labour strike in June. Looking ahead to 2025, we expect increased mill throughput and improved ore quality as we move deeper into the Connector pit. Copper production next year is expected to increase to the 120 to 130 million pound range, and molybdenum production is also expected to increase. Lower-grade ore stockpiles will be used to supplement mined ore in the first half of the year, so production will be weighted to the second half of the year.”

Mr. McDonald continued, “Construction at Florence Copper has continued to progress on schedule. We are now in peak construction with nearly 300 contractors working at site. The SX/EW plant activities have shifted from earth works and concrete foundation pouring to now erecting structural steel and installation of processing equipment and electrical services. Development of the wellfield is advancing with four drill rigs now operating and 40 wells completed at the end of October. Development of the wellfield, which is a critical path item, remains on schedule to be completed in the second quarter of next year.”

“We expect Florence Copper to become North America’s lowest GHG-intensity primary copper producer, and we’re optimistic that the project will qualify for the U.S. Department of Energy’s (“DOE”) Qualifying Advanced Energy Project Credit (48C) Program, which we applied for recently. We expect to hear whether our application was successful in January. Our balance sheet remains in a strong position, with $209 million of cash on hand and total liquidity of approximately $317 million at the end of September,” added Mr. McDonald.

“This is a very exciting time for Taseko as we begin to unlock the value of our growth assets. The Florence Copper project continues to be de-risked and is now just a year away from producing first copper. We’re also preparing to take a big step forward with our Yellowhead copper project, which will be entering the environmental assessment process in the coming months. We also plan on issuing an updated feasibility study for the project next year, which will reinforce the significant value of what could be British Columbia’s next major copper mine,” concluded Mr. McDonald.

Third Quarter Review

- Earnings from mining operations before depletion, amortization and non-recurring items* was $54.5 million and Adjusted EBITDA* was $47.7 million;

- Third quarter cash flow from operations was $65.0 million, and included $26.3 million for proceeds received on the insurance claim recorded in the prior quarter;

- Net loss was $0.2 million ($Nil per share) for the quarter and Adjusted net income* was $8.2 million ($0.03 per share);

- Gibraltar produced 27.1 million pounds of copper in the quarter. Average copper head grades were 0.23% and copper recoveries were 79% for the quarter;

- Although 7.6 million tons of ore was milled in the quarter, mill throughput was impacted by nearly three weeks of downtime in Concentrator #1 at the beginning of the quarter for the completion of the crusher relocation project, concurrent mill maintenance, and the ramp back up to full capacity;

- Gibraltar sold 26.3 million pounds of copper in the quarter at an average realized copper price of US$4.23 per pound;

- Total operating costs (C1)* for the quarter were US$2.92 per pound produced. Lower off-property costs are mainly due to favorably lower treatment and refining (“TCRC”) rates realized during the quarter as new offtake agreements begin to take effect;

- Construction of the Florence Copper commercial production facility continues to advance on schedule. A total of 34 production wells out of a total of 90 new wells had been completed as of September 30. Earthworks and site preparation for the plant area and commercial wellfield is estimated to be 75% complete and installation of structural steel, tanks, and process equipment is underway;

- An application has been made to the U.S. Department of Energy’s Qualifying Advanced Energy Project Credit (48C) Program for a tax credit of up to US$110 million, based on Florence Copper’s eligibility as a critical materials project. The Company expects to hear if it has been awarded the tax credit in mid-January 2025;

- On November 6, the Company entered into an amendment for its revolving credit facility, extending the maturity date to November 2027 from July 2026, and increasing the facility amount to US$110 million from US$80 million. No amounts are drawn against the revolving credit facility;

- The Company issued 7.8 million shares under its At-the-Market (“ATM”) equity offering in the quarter and received net proceeds of $23.1 million. Subsequently, the Company issued an additional 4.3 million shares under the ATM and received net proceeds of $14.2 million; and

- The Company had a cash balance of $209 million as at September 30, 2024.

Highlights

| Operating Data (Gibraltar - 100% basis) | Three months ended September 30, | Nine months ended September 30, | ||||||

| 2024 | 2023 | Change | 2024 | 2023 | Change | |||

| Tons mined (millions) | 23.2 | 16.5 | 6.7 | 64.4 | 64.0 | 0.4 | ||

| Tons milled (millions) | 7.6 | 8.0 | (0.4 | ) | 21.0 | 22.4 | (1.4 | ) |

| Production (million pounds Cu) | 27.1 | 35.4 | (8.3 | ) | 77.0 | 88.5 | (11.5 | ) |

| Sales (million pounds Cu) | 26.3 | 32.1 | (5.8 | ) | 80.6 | 84.8 | (4.2 | ) |

| Financial Data | Three months ended September 30, | Nine months ended September 30, | |||||||

| (Cdn$ in thousands, except for per share amounts) | 2024 | 2023 | Change | 2024 | 2023 | Change | |||

| Revenues | 155,617 | 143,835 | 11,782 | 440,294 | 371,278 | 69,016 | |||

| Cash flows provided by operations | 65,038 | 26,989 | 38,049 | 159,323 | 88,257 | 71,066 | |||

| Net (loss) income (GAAP) | (180 | ) | 871 | (1,051 | ) | 7,763 | 44,650 | (36,887 | ) |

| Per share – basic (“EPS”) | - | - | - | 0.03 | 0.15 | (0.12 | ) | ||

| Earnings from mining operations before depletion, amortization and non-recurring items* | 54,516 | 65,445 | (10,929 | ) | 184,241 | 134,248 | 49,993 | ||

| Adjusted EBITDA* | 47,689 | 62,695 | (15,006 | ) | 168,389 | 120,972 | 47,417 | ||

| Adjusted net income* | 8,228 | 19,659 | (11,431 | ) | 46,459 | 20,372 | 26,087 | ||

| Per share – basic (“adjusted EPS”)* | 0.03 | 0.07 | (0.04 | ) | 0.16 | 0.07 | 0.09 | ||

Effective as of March 25, 2024 the Company increased its ownership in Gibraltar from 87.5% to 100%. As a result, the financial results reported in this MD&A include 100% of Gibraltar income and expenses for the period March 25, 2024 to September 30, 2024 (87.5% for the period March 16, 2023 to March 24, 2024, and 75% prior to March 15, 2023). For more information on the Company’s acquisition of Cariboo, please refer to the Financial Statements – Note 3.

The Company finalized the accounting for the acquisition of its initial 50% interest in Cariboo from Sojitz and the related 12.5% interest in Gibraltar in the fourth quarter of 2023. In accordance with the accounting standards for business combinations, the comparable financial statements as of September 30, 2023 and for the three and nine months then ended have been revised to reflect the changes in finalizing the consideration paid and the allocation of the purchase price to the assets and liabilities acquired.

Review of Operations

Gibraltar mine

| Operating data (100% basis) | Q3 2024 | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 | ||||||||||

| Tons mined (millions) | 23.2 | 18.4 | 22.8 | 24.1 | 16.5 | ||||||||||

| Tons milled (millions) | 7.6 | 5.7 | 7.7 | 7.6 | 8.0 | ||||||||||

| Strip ratio | 1.2 | 1.6 | 1.7 | 1.5 | 0.4 | ||||||||||

| Site operating cost per ton milled (Cdn$)* | $14.23 | $13.93 | $11.73 | $9.72 | $12.39 | ||||||||||

| Copper concentrate | |||||||||||||||

| Head grade (%) | 0.23 | 0.23 | 0.24 | 0.27 | 0.26 | ||||||||||

| Copper recovery (%) | 78.9 | 77.7 | 79.0 | 82.2 | 85.0 | ||||||||||

| Production (million pounds Cu) | 27.1 | 20.2 | 29.7 | 34.2 | 35.4 | ||||||||||

| Sales (million pounds Cu) | 26.3 | 22.6 | 31.7 | 35.9 | 32.1 | ||||||||||

| Inventory (million pounds Cu) | 2.9 | 2.3 | 4.9 | 6.9 | 8.8 | ||||||||||

| Molybdenum concentrate | |||||||||||||||

| Production (thousand pounds Mo) | 421 | 185 | 247 | 369 | 369 | ||||||||||

| Sales (thousand pounds Mo) | 348 | 221 | 258 | 364 | 370 | ||||||||||

| Per unit data (US$ per pound produced)* | |||||||||||||||

| Site operating costs* | $2.91 | $2.88 | $2.21 | $1.59 | $2.10 | ||||||||||

| By-product credits* | (0.25 | ) | (0.26 | ) | (0.17 | ) | (0.13 | ) | (0.23 | ) | |||||

| Site operating costs, net of by-product credits* | $2.66 | $2.62 | $2.04 | $1.46 | $1.87 | ||||||||||

| Off-property costs | 0.26 | 0.37 | 0.42 | 0.45 | 0.33 | ||||||||||

| Total operating costs (C1)* | $2.92 | $2.99 | $2.46 | $1.91 | $2.20 | ||||||||||

Operations Analysis

Third Quarter Review

Gibraltar produced 27 million pounds of copper in the quarter. Copper production and mill throughput were impacted by nearly three weeks of downtime in Concentrator #1 at the beginning of the quarter to complete the crusher relocation project, concurrent mill maintenance, and the ramp back up to full capacity.

Copper head grades were 0.23% and more Connector pit ore was fed to the mill. Copper recoveries in the third quarter were 79%, in line with recent quarters, but lower than normal, as the upper benches of the Connector pit contain transition ore with higher oxide content. As mining progresses deeper in the Connector pit, recoveries are expected to improve as oxide content reduces.

A total of 23.2 million tons were mined in the third quarter, and the majority of ore and waste mining occurred in the Connector pit during the period. A total of 1.7 million tons of oxide ore from the upper benches of the Connector pit were also added to the heap leach pads in the period for future copper cathode production from Gibraltar’s currently idled SX/EW plant.

Total site costs* at Gibraltar of $111.3 million (which includes capitalized stripping of $3.6 million) was higher compared to the previous quarter due to the Gibraltar mine being on care and maintenance during the labour strike

in June. Total site costs* were generally in line with the fourth quarter of 2023 and first quarter of 2024. Higher repairs and maintenance costs were incurred in the quarter due to a large maintenance project on one of the shovels.

During the three months ended September 30, 2024, the Company incurred costs of $4.1 million in relation to the final phase of the in-pit crusher relocation project for Concentrator #1 including demolition of the old station’s concrete foundation. Under IFRS, these costs are expensed in the quarter through the statement of income (loss).

Molybdenum production was 421 thousand pounds in the third quarter. The 128% increase in quarter-over-quarter production is primarily due to higher molybdenum grade in the Connector pit ore. At an average molybdenum price of US$21.77 per pound, molybdenum generated a by-product credit per pound of copper produced of US$0.25 in the third quarter.

Off-property costs per pound produced* were US$0.26 for the third quarter, which is lower than recent quarters and reflects lower average TCRC rates realized on third quarter shipments, some of which were tendered earlier in the year at negative rates.

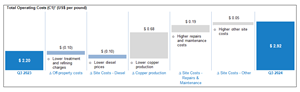

Total operating costs per pound produced (C1)* was US$2.92 for the quarter, compared to US$2.20 in the prior year quarter as shown in the bridge graph below with the difference substantially attributed to the lower copper production in the quarter:

https://www.globenewswire.com/NewsRoom/AttachmentNg/0d7f5203-7171-4c0b-a812-df2577edc1cf

Gibraltar Outlook

The major project and related mill maintenance work was completed in the third quarter, and lower than planned mill availability and throughput impacted copper production in the period. As a result, management does not expect to recover the copper production that was lost during the 18-day strike in June and copper production for the year is now expected to be in the range of 105 to 110 million pounds, compared to the original guidance of 115 million pounds. Increased mill availability and higher throughput is expected to be the primary driver of improved copper production in the fourth quarter.

Mining activities have mostly transitioned to the Connector pit, which will be the main source of mill feed in the fourth quarter and going forward. Mining of the current phase of the Gibraltar pit is expected to be finished in the first quarter of 2025. Additional oxide ore from the Connector pit will also be added to the heap leach pads this year. Refurbishment of Gibraltar’s SX/EW plant, which has been idle since 2015, has begun and the plant is expected to be restarted in mid-2025.

For 2025, copper head grade and tonnes milled are expected to improve and total copper production is expected to be in the range of 120 to 130 million pounds. Lower grade ore stockpiles will be utilized to supplement mined ore in the first half of 2025, which will result in copper production being weighted to the second half of the year. Molybdenum production is forecast to increase next year as molybdenum head grades are expected to be notably higher in the Connector pit compared to the Gibraltar pit.

The Company has tendered Gibraltar concentrate to various customers for the remainder of 2024 and for significant tonnages in 2025 and 2026. In 2023, TCRCs accounted for approximately US$0.17 per pound of off-property costs. With these recently awarded offtake contracts, the Company expects TCRCs to reduce to nil on average in 2025 on the sale of its copper concentrate.

The Company has a prudent hedging program in place to protect a minimum copper price during the Florence construction period. Currently, the Company has copper collar contracts that secure a minimum copper price of US$3.75 per pound for 21 million pounds of copper covering the fourth quarter of 2024, and copper collar contracts that secure a minimum copper price of US$4.00 per pound for 108 million pounds of copper for 2025. The copper collar contracts also have ceiling prices between US$5.00 and US$5.40 per pound (refer to the section “Hedging Strategy” for details).

Florence Copper

The Company has all the key permits in place for the commercial production facility at Florence Copper and construction has commenced. First copper production is expected in the fourth quarter of 2025.

The Company has a technical report entitled “NI 43-101 Technical Report Florence Copper Project, Pinal County, Arizona” dated March 30, 2023 (the “2023 Technical Report”) on SEDAR+. The 2023 Technical Report was prepared in accordance with NI 43-101 and incorporated the results of testwork from the Production Test Facility (“PTF”) as well as updated capital and operating costs (Q3 2022 basis) for the commercial production facility.

Project highlights based on the 2023 Technical Report:

- Net present value of US$930 million (at $US 3.75 copper price, 8% after-tax discount rate)

- Internal rate of return of 47% (after-tax)

- Payback period of 2.6 years

- Operating costs (C1) of US$1.11 per pound of copper

- Annual production capacity of 85 million pounds of LME grade A cathode copper

- 22 year mine life

- Total life of mine production of 1.5 billion pounds of copper

- Remaining initial capital cost of US$232 million (Q3 2022 basis)

Construction of the Florence Copper commercial production facility continues to advance on schedule. A total of 34 production wells out of a total of 90 new wells had been completed as of September 30, 2024. Earthworks and site preparation for the plant area and commercial wellfield is estimated to be 75% complete and installation of structural steel, tanks, and process equipment is underway. Construction of process and surface water run off ponds and the hiring of additional personnel for the construction and operations teams continues.

The Company has a fixed-price contract with the general contractor for construction of the SX/EW plant and associated surface infrastructure.

Florence Copper Quarterly Capital Spend

| Three months ended | Nine months ended | |

| (US$ in thousands) | September 30, 2024 | September 30, 2024 |

| Site and PTF operations | 4,946 | 13,505 |

| Commercial facility construction costs | 42,405 | 97,253 |

| Other capital costs | 6,251 | 29,013 |

| Total Florence project expenditures | 53,602 | 139,771 |

Based on the 2023 Technical report, the estimated remaining construction costs for the commercial facility were US$232 million (basis Q3 2022), and management expects that total costs will be within 10% to 15% of that estimate. The project remains on track for first copper production in late 2025.

Construction costs in the third quarter were US$42.4 million, and US$97.3 million has been incurred for the nine months ended September 30, 2024. Other capital costs of US$29.0 million include final payments for delivery of long-lead equipment that was ordered in 2022, and the construction of an evaporation pond to provide additional water management flexibility. Construction of this evaporation pond was completed in the third quarter.

The Company has closed several Florence project level financings to fund initial commercial facility construction costs. In July the Company received the third deposit of US$10 million from the US$50 million copper stream transaction with Mitsui & Co. (U.S.A.) Inc. (“Mitsui”). The fourth deposit was received in October and the remaining US$10 million is scheduled to be received in January 2025.

In addition, the Company has applied to the U.S. Department of Energy’s (“DOE”) Qualifying Advanced Energy Project Credit (48C) Program. Florence Copper, which is set to become North America’s lowest GHG-intensity primary copper producer, qualifies as a critical materials project. After submitting a concept paper in June, Florence Copper received encouragement to proceed with the full application. The full application has now been filed seeking a tax credit of up to US$110 million, and the Company expects to hear whether the project receives the credit, or not, in mid-January 2025. The Department of the Treasury (“Treasury”) and the Internal Revenue Service (“IRS”), in partnership with DOE, have announced up to US$6 billion in a second round of tax credit allocations for projects that expand clean energy manufacturing and recycling and critical materials refining, processing and recycling, and for projects that reduce greenhouse gas emissions at industrial facilities. DOE’s Office of Manufacturing & Energy Supply Chains manages the 48C program on behalf of IRS and Treasury.

Remaining project construction costs are expected to be funded with the Company’s available liquidity, remaining instalment from Mitsui, and cashflow from its 100% ownership interest in Gibraltar. The Company also has in place an undrawn corporate revolving credit facility for US$110 million.

Long-term Growth Strategy

Taseko’s strategy has been to grow the Company by acquiring and developing a pipeline of projects focused on copper in North America. We continue to believe this will generate long-term returns for shareholders. Our other development projects are located in British Columbia, Canada.

Yellowhead Copper Project

Based on a NI 43-101 technical report published in 2020, the Yellowhead Copper Project (“Yellowhead”) has an 817 million tonne mineral reserve and a 25-year mine life. During the first 5 years of operation, the copper equivalent grade will average 0.35% producing an average of 200 million pounds of copper per year at an average C1* cost, net of by-product credit, of US$1.67 per pound. The Yellowhead copper project contains valuable precious metal by-products with 440,000 ounces of gold and 19 million ounces of silver production over the life of mine.

The 2020 technical report was prepared using long-term copper price of US$3.10 per pound, a gold price of US$1,350 per ounce, and silver price of US$18 per ounce. A new technical report will be published in 2025 using updated long-term metal price assumptions, updated project costing, and incorporating the new Canadian tax credits available for copper mine development.

The Company is preparing to enter the environmental assessment process in early 2025, and has recently opened a project office to support ongoing engagement with local communities including First Nations. A site investigation field program was completed in the third quarter, and the additional baseline data and modeling will be used to support the environmental assessment and permitting of the project.

New Prosperity Gold-Copper Project

In late 2019, the Tŝilhqot’in Nation, as represented by Tŝilhqot’in National Government, and Taseko Mines Limited entered into a confidential dialogue, with the involvement of the Province of British Columbia, seeking a long-term resolution of the conflict regarding Taseko’s proposed copper-gold mine previously known as New Prosperity, acknowledging Taseko’s commercial interests and the Tŝilhqot’in Nation’s opposition to the project.

This dialogue has been supported by the parties’ agreement, beginning December 2019, to a series of standstill agreements on certain outstanding litigation and regulatory matters relating to Taseko’s tenures and the area in the vicinity of Teẑtan Biny (Fish Lake).

The dialogue process has made meaningful progress in recent months but is not complete. The Tŝilhqot’in Nation and Taseko acknowledge the constructive nature of discussions, and the opportunity to conclude a long-term and mutually acceptable resolution of the conflict that also makes an important contribution to the goals of reconciliation in Canada.

In March 2024, Tŝilhqot’in and Taseko formally reinstated the standstill agreement for a final term, with the goal of finalizing a resolution before the end of this year.

Aley Niobium Project

Environmental monitoring and product marketing initiatives on the Aley niobium project continue. The converter pilot test is ongoing and is providing additional process data to support the design of the commercial process facilities and will provide final product samples for marketing purposes. The Company has also initiated a scoping study to investigate the potential production of niobium oxide at Aley to supply the growing market for niobium-based batteries.

Conference Call and Webcast The Company will host a telephone conference call and live webcast on Thursday, November 7, 2024, at 11:00 a.m. Eastern Time (8:00 a.m. Pacific) to discuss these results. After opening remarks by management, there will be a question-and-answer session open to analysts and investors. Participants can join by conference call dial-in or webcast: Conference Call Dial-In

| |

For further information on Taseko, please see the Company's website at www.tasekomines.com or contact:

Brian Bergot, Vice President, Investor Relations – 778-373-4554, toll free 1-800-667-2114

Stuart McDonald

President & CEO

No regulatory authority has approved or disapproved of the information in this news release.

* Non-GAAP Performance Measures

This document includes certain non-GAAP performance measures that do not have a standardized meaning prescribed by IFRS. These measures may differ from those used by, and may not be comparable to such measures as reported by, other issuers. The Company believes that these measures are commonly used by certain investors, in conjunction with conventional IFRS measures, to enhance their understanding of the Company’s performance. These measures have been derived from the Company’s financial statements and applied on a consistent basis. The following tables below provide a reconciliation of these non-GAAP measures to the most directly comparable IFRS measure.

Total operating costs and site operating costs, net of by-product credits

Total costs of sales include all costs absorbed into inventory, as well as transportation costs and insurance recoverable. Site operating costs are calculated by removing net changes in inventory, depletion and amortization, insurance recoverable, and transportation costs from cost of sales. Site operating costs, net of by-product credits is calculated by subtracting by-product credits from the site operating costs. Site operating costs, net of by-product credits per pound are calculated by dividing the aggregate of the applicable costs by copper pounds produced. Total operating costs per pound is the sum of site operating costs, net of by-product credits and off-property costs divided by the copper pounds produced. By-product credits are calculated based on actual sales of molybdenum (net of treatment costs) and silver during the period divided by the total pounds of copper produced during the period. These measures are calculated on a consistent basis for the periods presented.

| (Cdn$ in thousands, unless otherwise indicated) | 2024 Q3 | 2024 Q2 | 2024 Q11 | 2023 Q41 | 2023 Q31 | |||||

| Cost of sales | 124,833 | 108,637 | 122,528 | 93,914 | 94,383 | |||||

| Less: | ||||||||||

| Depletion and amortization | (20,466 | ) | (13,721 | ) | (15,024 | ) | (13,326 | ) | (15,993 | ) |

| Net change in inventories of finished goods | 2,938 | (10,462 | ) | (20,392 | ) | (1,678 | ) | 4,267 | ||

| Net change in inventories of ore stockpiles | 9,089 | 1,758 | 2,719 | (3,771 | ) | 12,172 | ||||

| Transportation costs | (8,682 | ) | (6,408 | ) | (10,153 | ) | (10,294 | ) | (7,681 | ) |

| Site operating costs | 107,712 | 79,804 | 79,678 | 64,845 | 87,148 | |||||

| Less by-product credits: | ||||||||||

| Molybdenum, net of treatment costs | (8,962 | ) | (7,071 | ) | (6,112 | ) | (5,441 | ) | (9,900 | ) |

| Silver, excluding amortization of deferred revenue | (241 | ) | (144 | ) | (137 | ) | 124 | 290 | ||

| Site operating costs, net of by-product credits | 98,509 | 72,589 | 73,429 | 59,528 | 77,538 | |||||

| Total copper produced (thousand pounds) | 27,101 | 20,225 | 26,694 | 29,883 | 30,978 | |||||

| Total costs per pound produced | 3.63 | 3.59 | 2.75 | 1.99 | 2.50 | |||||

| Average exchange rate for the period (CAD/USD) | 1.36 | 1.37 | 1.35 | 1.36 | 1.34 | |||||

| Site operating costs, net of by-product credits (US$ per pound) | 2.66 | 2.62 | 2.04 | 1.46 | 1.87 | |||||

| Site operating costs, net of by-product credits | 98,509 | 72,589 | 73,429 | 59,528 | 77,538 | |||||

| Add off-property costs: | ||||||||||

| Treatment and refining costs | 816 | 3,941 | 4,816 | 7,885 | 6,123 | |||||

| Transportation costs | 8,682 | 6,408 | 10,153 | 10,294 | 7,681 | |||||

| Total operating costs | 108,008 | 82,938 | 88,398 | 77,707 | 91,342 | |||||

| Total operating costs (C1) (US$ per pound) | 2.92 | 2.99 | 2.46 | 1.91 | 2.20 | |||||

1 Q3 and Q4 2023 includes the impact from the March 15, 2023 acquisition of Cariboo from Sojitz, which increased the Company’s Gibraltar ownership from 75% to 87.5%. Q1 2024 includes the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company’s Gibraltar ownership from 87.5% to 100%.

Total Site Costs

Total site costs are comprised of the site operating costs charged to cost of sales as well as mining costs capitalized to property, plant and equipment in the period. This measure is intended to capture Taseko’s share of the total site operating costs incurred in the quarter at Gibraltar calculated on a consistent basis for the periods presented.

| (Cdn$ in thousands, unless otherwise indicated) – 87.5% basis (except for Q1, Q2 and Q3 2024) | 2024 Q3 | 2024 Q2 | 2024 Q11 | 2023 Q41 | 2023 Q31 |

| Site operating costs | 107,712 | 79,804 | 79,678 | 64,845 | 87,148 |

| Add: | |||||

| Capitalized stripping costs | 3,631 | 10,732 | 16,152 | 31,916 | 2,083 |

| Total site costs – Taseko share | 111,343 | 90,536 | 95,830 | 96,761 | 89,231 |

| Total site costs – 100% basis | 111,343 | 90,536 | 109,520 | 110,584 | 101,978 |

1 Q3 and Q4 2023 includes the impact from the March 15, 2023 acquisition of Cariboo from Sojitz, which increased the Company’s Gibraltar ownership from 75% to 87.5%. Q1 2024 includes the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company’s Gibraltar ownership from 87.5% to 100%.

Adjusted net income (loss) and Adjusted EPS

Adjusted net income (loss) removes the effect of the following transactions from net income as reported under IFRS:

- Unrealized foreign currency gains/losses;

- Unrealized gain/loss on derivatives;

- Other operating costs;

- Call premium on settlement of debt;

- Loss on settlement of long-term debt, net of capitalized interest;

- Gain on Cariboo acquisition;

- Gain on acquisition of control of Gibraltar;

- Realized gain on sale of inventory;

- Inventory write-ups to net realizable value that was sold or processed;

- Accretion and fair value adjustment on Florence royalty obligation; and

- Finance and other non-recurring costs for Cariboo acquisition.

Management believes these transactions do not reflect the underlying operating performance of our core mining business and are not necessarily indicative of future operating results. Furthermore, unrealized gains/losses on derivative instruments, changes in the fair value of financial instruments, and unrealized foreign currency gains/losses are not necessarily reflective of the underlying operating results for the reporting periods presented.

Adjusted net income (loss) and Adjusted EPS

| (Cdn$ in thousands, except per share amounts) | 2024 Q3 | 2024 Q2 | 2024 Q1 | 2023 Q4 | ||||

| Net (loss) income | (180 | ) | (10,953 | ) | 18,896 | 38,076 | ||

| Unrealized foreign exchange (gain) loss | (7,259 | ) | 5,408 | 13,688 | (14,541 | ) | ||

| Unrealized loss on derivatives | 1,821 | 10,033 | 3,519 | 1,636 | ||||

| Other operating costs | 4,098 | 10,435 | - | - | ||||

| Call premium on settlement of debt | - | 9,571 | - | - | ||||

| Loss on settlement of long-term debt, net of capitalized interest | - | 2,904 | - | - | ||||

| Gain on Cariboo acquisition | - | - | (47,426 | ) | - | |||

| Gain on acquisition of control of Gibraltar** | - | - | (14,982 | ) | - | |||

| Realized gain on sale of inventory*** | - | 3,768 | 13,354 | - | ||||

| Inventory write-ups to net realizable value that was sold or processed**** | 3,266 | 4,056 | - | - | ||||

| Accretion and fair value adjustment on Florence royalty obligation | 3,703 | 2,132 | 3,416 | - | ||||

| Accretion and fair value adjustment on consideration payable to Cariboo | 9,423 | 8,399 | 1,555 | (916 | ) | |||

| Non-recurring other expenses for Cariboo acquisition | - | 394 | 138 | - | ||||

| Estimated tax effect of adjustments | (6,644 | ) | (15,644 | ) | 15,570 | (195 | ) | |

| Adjusted net income | 8,228 | 30,503 | 7,728 | 24,060 | ||||

| Adjusted EPS | 0.03 | 0.10 | 0.03 | 0.08 | ||||

| (Cdn$ in thousands, except per share amounts) | 2023 Q3 | 2023 Q2 | 2023 Q1 | 2022 Q4 | ||||

| Net income (loss) | 871 | 9,991 | 33,788 | (2,275 | ) | |||

| Unrealized foreign exchange loss (gain) | 14,582 | (10,966 | ) | (950 | ) | (5,279 | ) | |

| Unrealized loss (gain) on derivatives | 4,518 | (6,470 | ) | 2,190 | 20,137 | |||

| Gain on Cariboo acquisition | - | - | (46,212 | ) | - | |||

| Accretion and fair value adjustment on consideration payable to Cariboo | 1,244 | 1,451 | - | - | ||||

| Non-recurring other expenses for Cariboo acquisition | - | 263 | - | - | ||||

| Estimated tax effect of adjustments | (1,556 | ) | 1,355 | 16,272 | (5,437 | ) | ||

| Adjusted net income (loss) | 19,659 | (4,376 | ) | 5,088 | 7,146 | |||

| Adjusted EPS | 0.07 | (0.02 | ) | 0.02 | 0.02 | |||

** The $15.0 million gain on acquisition of control of Gibraltar in Q1 2024 relates to the write-up of finished copper concentrate inventory for Taseko’s 87.5% share to its fair value at March 25, 2024.

*** Cost of sales for the nine months ended September 30, 2024 included $17.1 million in write-ups to net realizable value for concentrate inventory held at the date of acquisition of control of Gibraltar (March 25, 2024) that were subsequently sold. The realized portion of the gains recorded in the first quarter for GAAP purposes was $13.4 million and for the second quarter were $3.8 million and have been included in Adjusted net income in the period they were sold.

**** Write-ups to net realizable value for inventory held at the date of acquisition of control of Gibraltar (March 25, 2024) totaled $9.2 million. The inventory write-ups in the first quarter for GAAP purposes have been included in Adjusted net income in the period they were sold or processed. Cost of sales for the nine months ended September 30, 2024 included $7.3 million in inventory write-ups that were subsequently sold or processed in the second and third quarters.

Adjusted EBITDA

Adjusted EBITDA is presented as a supplemental measure of the Company’s performance and ability to service debt. Adjusted EBITDA is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in the industry, many of which present Adjusted EBITDA when reporting their results. Issuers of “high yield” securities also present Adjusted EBITDA because investors, analysts and rating agencies consider it useful in measuring the ability of those issuers to meet debt service obligations.

Adjusted EBITDA represents net income before interest, income taxes, and depreciation and also eliminates the impact of a number of items that are not considered indicative of ongoing operating performance. Certain items of expense are added and certain items of income are deducted from net income that are not likely to recur or are not indicative of the Company’s underlying operating results for the reporting periods presented or for future operating performance and consist of:

- Unrealized foreign exchange gains/losses;

- Unrealized gain/loss on derivatives;

- Amortization of share-based compensation expense;

- Other operating costs;

- Call premium on settlement of debt;

- Loss on settlement of long-term debt;

- Gain on Cariboo acquisition;

- Gain on acquisition of control of Gibraltar;

- Realized gain on sale of inventory;

- Inventory write-ups to net realizable value that was sold or processed; and

- Finance and other non-recurring costs for Cariboo acquisition.

| (Cdn$ in thousands) | 2024 Q3 | 2024 Q2 | 2024 Q1 | 2023 Q4 | ||||

| Net (loss) income | (180 | ) | (10,953 | ) | 18,896 | 38,076 | ||

| Add: | ||||||||

| Depletion and amortization | 20,466 | 13,721 | 15,024 | 13,326 | ||||

| Finance expense | 25,685 | 21,271 | 19,849 | 12,804 | ||||

| Finance income | (1,504 | ) | (911 | ) | (1,086 | ) | (972 | ) |

| Income tax (recovery) expense | (200 | ) | (3,247 | ) | 23,282 | 17,205 | ||

| Unrealized foreign exchange (gain) loss | (7,259 | ) | 5,408 | 13,688 | (14,541 | ) | ||

| Unrealized loss on derivatives | 1,821 | 10,033 | 3,519 | 1,636 | ||||

| Amortization of share-based compensation expense | 1,496 | 2,585 | 5,667 | 1,573 | ||||

| Other operating costs | 4,098 | 10,435 | - | - | ||||

| Call premium on settlement of debt | - | 9,571 | - | - | ||||

| Loss on settlement of long-term debt | - | 4,646 | - | - | ||||

| Gain on Cariboo acquisition | - | - | (47,426 | ) | - | |||

| Gain on acquisition of control of Gibraltar** | - | - | (14,982 | ) | - | |||

| Realized gain on sale of inventory*** | - | 3,768 | 13,354 | - | ||||

| Inventory write-ups to net realizable value that was sold or processed**** | 3,266 | 4,056 | - | - | ||||

| Non-recurring other expenses for Cariboo acquisition | - | 394 | 138 | - | ||||

| Adjusted EBITDA | 47,689 | 70,777 | 49,923 | 69,107 | ||||

** The $15.0 million gain on acquisition of control of Gibraltar in Q1 2024 relates to the write-up of finished copper concentrate inventory for Taseko’s 87.5% share to its fair value at March 25, 2024.

*** Cost of sales for the nine months ended September 30, 2024 included $17.1 million in write-ups to net realizable value for concentrate inventory held at the date of acquisition of control of Gibraltar (March 25, 2024) that were subsequently sold. The realized portion of the gains recorded in the first quarter for GAAP purposes was $13.4 million and for the second quarter were $3.8 million and have been included in Adjusted net income in the period they were sold.

**** Write-ups to net realizable value for inventory held at the date of acquisition of control of Gibraltar (March 25, 2024) totaled $9.2 million. The inventory write-ups in the first quarter for GAAP purposes have been included in Adjusted net income in the period they were sold or processed. Cost of sales for the nine months ended September 30, 2024 included $7.3 million in inventory write-ups that were subsequently sold or processed in the second and third quarters.

| (Cdn$ in thousands) | 2023 Q3 | 2023 Q2 | 2023 Q1 | 2022 Q4 | ||||

| Net income (loss) | 871 | 9,991 | 33,788 | (2,275 | ) | |||

| Add: | ||||||||

| Depletion and amortization | 15,993 | 15,594 | 12,027 | 10,147 | ||||

| Finance expense | 14,285 | 13,468 | 12,309 | 10,135 | ||||

| Finance income | (322 | ) | (757 | ) | (921 | ) | (700 | ) |

| Income tax expense | 12,041 | 678 | 20,219 | 1,222 | ||||

| Unrealized foreign exchange loss (gain) | 14,582 | (10,966 | ) | (950 | ) | (5,279 | ) | |

| Unrealized loss (gain) on derivatives | 4,518 | (6,470 | ) | 2,190 | 20,137 | |||

| Amortization of share-based compensation expense | 727 | 417 | 3,609 | 1,794 | ||||

| Gain on Cariboo acquisition | - | - | (46,212 | ) | - | |||

| Non-recurring other expenses for Cariboo acquisition | - | 263 | - | - | ||||

| Adjusted EBITDA | 62,695 | 22,218 | 36,059 | 35,181 | ||||

Earnings from mining operations before depletion, amortization and non-recurring items

Earnings from mining operations before depletion, amortization and non-recurring items is earnings from mining operations with depletion and amortization, and any items that are not considered indicative of ongoing operating performance added back. The Company discloses this measure, which has been derived from our financial statements and applied on a consistent basis, to assist in understanding the results of the Company’s operations and financial position and it is meant to provide further information about the financial results to investors.

| Three months ended September 30, | Nine months ended September 30, | |||

| (Cdn$ in thousands) | 2024 | 2023 | 2024 | 2023 |

| Earnings from mining operations | 26,686 | 49,452 | 96,053 | 90,634 |

| Add: | ||||

| Depletion and amortization | 20,466 | 15,993 | 49,211 | 43,614 |

| Realized gain on sale of inventory | - | - | 17,122 | - |

| Inventory write-ups to net realizable value that was sold or processed | 3,266 | - | 7,322 | - |

| Other operating costs | 4,098 | - | 14,533 | - |

| Earnings from mining operations before depletion, amortization and non-recurring items | 54,516 | 65,445 | 184,241 | 134,248 |

During the nine months ended September 30, 2024, the realized gain on sale of inventory and inventory write-ups to net realizable value that was sold or processed, relates to inventory held at the date of acquisition of control of Gibraltar (March 25, 2024) that was written-up from book value to net realizable value and subsequently sold or processed.

Site operating costs per ton milled

The Company discloses this measure, which has been derived from our financial statements and applied on a consistent basis, to provide assistance in understanding the Company’s site operations on a tons milled basis.

| (Cdn$ in thousands, except per ton milled amounts) | 2024 Q3 | 2024 Q2 | 2024 Q11 | 2023 Q41 | 2023 Q31 | |||||

| Site operating costs (included in cost of sales) – Taseko share | 107,712 | 79,804 | 79,678 | 64,845 | 87,148 | |||||

| Site operating costs – 100% basis | 107,712 | 79,804 | 90,040 | 74,109 | 99,598 | |||||

| Tons milled (thousands) | 7,572 | 5,728 | 7,677 | 7,626 | 8,041 | |||||

| Site operating costs per ton milled | $14.23 | $13.93 | $11.73 | $9.72 | $12.39 | |||||

1 Q3 and Q4 2023 includes the impact from the March 15, 2023 acquisition of Cariboo from Sojitz, which increased the Company’s Gibraltar ownership from 75% to 87.5%. Q1 2024 includes the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company’s Gibraltar ownership from 87.5% to 100%.

Caution Regarding Forward-Looking Information

This document contains “forward-looking statements” that were based on Taseko’s expectations, estimates and projections as of the dates as of which those statements were made. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “outlook”, “anticipate”, “project”, “target”, “believe”, “estimate”, “expect”, “intend”, “should” and similar expressions.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements. These included but are not limited to:

- uncertainties about the effect of COVID-19 and the response of local, provincial, federal and international governments to the threat of COVID-19 on our operations (including our suppliers, customers, supply chain, employees and contractors) and economic conditions generally and in particular with respect to the demand for copper and other metals we produce;

- uncertainties and costs related to the Company’s exploration and development activities, such as those associated with continuity of mineralization or determining whether mineral resources or reserves exist on a property;

- uncertainties related to the accuracy of our estimates of mineral reserves, mineral resources, production rates and timing of production, future production and future cash and total costs of production and milling;

- uncertainties related to feasibility studies that provide estimates of expected or anticipated costs, expenditures and economic returns from a mining project;

- uncertainties related to the ability to obtain necessary licenses permits for development projects and project delays due to third party opposition;

- uncertainties related to unexpected judicial or regulatory proceedings;

- changes in, and the effects of, the laws, regulations and government policies affecting our exploration and development activities and mining operations, particularly laws, regulations and policies;

- changes in general economic conditions, the financial markets and in the demand and market price for copper, gold and other minerals and commodities, such as diesel fuel, steel, concrete, electricity and other forms of energy, mining equipment, and fluctuations in exchange rates, particularly with respect to the value of the U.S. dollar and Canadian dollar, and the continued availability of capital and financing;

- the effects of forward selling instruments to protect against fluctuations in copper prices and exchange rate movements and the risks of counterparty defaults, and mark to market risk;

- the risk of inadequate insurance or inability to obtain insurance to cover mining risks;

- the risk of loss of key employees; the risk of changes in accounting policies and methods we use to report our financial condition, including uncertainties associated with critical accounting assumptions and estimates;

- environmental issues and liabilities associated with mining including processing and stock piling ore; and

- labour strikes, work stoppages, or other interruptions to, or difficulties in, the employment of labour in markets in which we operate mines, or environmental hazards, industrial accidents or other events or occurrences, including third party interference that interrupt the production of minerals in our mines.

For further information on Taseko, investors should review the Company’s annual Form 40-F filing with the United States Securities and Exchange Commission www.sec.gov and home jurisdiction filings that are available at www.sedarplus.com.

Cautionary Statement on Forward-Looking Information

This discussion includes certain statements that may be deemed "forward-looking statements". All statements in this discussion, other than statements of historical facts, that address future production, reserve potential, exploration drilling, exploitation activities, and events or developments that the Company expects are forward-looking statements. Although we believe the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continued availability of capital and financing and general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except to the extent required by applicable law. Further information concerning risks and uncertainties associated with these forward-looking statements and our business may be found in our most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities.

![]()

Total Operating Costs (C1)* (US$ per pound) - Q3 2024