Yamana Gold Announces Fourth Quarter and Full Year 2018 Results

TORONTO, Feb. 14, 2019 (GLOBE NEWSWIRE) -- YAMANA GOLD INC. (TSX:YRI; NYSE:AUY) (“Yamana” or “the Company”) is herein reporting its financial and operational results for the fourth quarter and full year 2018, and its Mineral Reserve and Mineral Resource estimates as at December 31, 2018.

|

|||||||||||||||||||||||||||||||||||||||||||||

FOURTH QUARTER HIGHLIGHTS

Gold equivalent ounce (“GEO”)(1) production from Yamana Mines(2) for the fourth quarter was 310,369, including 270,193 ounces of gold and 3.26 million ounces of silver. Total Yamana gold production(3) was 292,484 ounces. The Company also produced 39.0 million pounds of copper.

Full year GEO production from Yamana Mines was 1,041,350, including 940,619 ounces of gold and 8.02 million ounces of silver. Full year copper production was 129.2 million pounds.

Full year gold and copper production from Yamana Mines exceeded the higher guidance levels set in October of last year while full year silver production exceeded the lower guidance provided at that time. Original guidance set in February 2018 was for 900,000 ounces of gold, 120 million pounds of copper and 8.15 million ounces of silver.

Fourth quarter costs for Yamana Mines included all-in sustaining costs (“AISC”) on a by-product basis(4) of $656 per GEO; cash costs on a by-product basis(4) of $418 per GEO; and total cost of sales of $1,019 per GEO. Full year costs for Yamana Mines included AISC on a by-product basis(4) of $699 per GEO; cash costs on a by-product basis(4) of $448 per GEO; and total cost of sales of $1,028 per GEO, which was in line with or better than guided ranges for the cost metrics. Refer to page 18 of this press release for additional information on costs by metal on a co-product and by-product basis. Going forward, reported cost metrics and cost guidance will reflect a change to the presentation methodology. Specifically, the Company, as an active member of the World Gold Council, has adopted the updated version of the Guidance Note on AISC, among other changes, that are detailed in Section 2 of the Company’s fourth quarter 2018 Management’s Discussion & Analysis, which has been filed on SEDAR. In the Company’s 2019-2021 Outlook press release, issued on February 14, 2019, cost metrics for 2018 have been restated for the updated methodology to facilitate direct comparisons.

(All amounts are expressed in United States dollars unless otherwise indicated.)

- Gold equivalent ounces include gold plus silver at a ratio of 81.3:1 for Q4 2018 and 79.6:1 for the full year 2018.

- Yamana Mines include Chapada, El Peñón, Canadian Malartic, Minera Florida, Jacobina and Cerro Moro.

- Total Yamana production includes production from Gualcamayo.

- Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion included at the end of this press release under the heading “Non-GAAP Financial Measures and Additional Line Items and Subtotals in Financial Statements”. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q42018 and in Section 11 of the Company’s fourth quarter 2018 Management’s Discussion & Analysis, which has been filed on SEDAR.

Adjusted Earnings(4) for the three months ended December 31, 2018 excluding certain items (see below), were $26.2 million or $0.03 per share. Net loss attributable to Yamana equity holders for the same period, was $61.4 million or $0.06 per share basic and diluted. This includes certain non-cash and other items that may not be reflective of current and ongoing operations, which reduced the Company’s net income by $87.6 million, or $0.09 per share basic and diluted.

Cash flows from operating activities for the fourth quarter were $114.7 million and cash flows from operating activities before net change in working capital(4) were $115.8 million. Fourth quarter cash flows were net of amortization of deferred revenue, $33.3 million of which related to deferred revenue recognized attributable to deliveries under the Company’s copper advanced sales program during the quarter. Deliveries under the Company's copper advanced sales program began during the third quarter 2018 and will continue until mid-2019. If not for the timing difference of cash proceeds attributable to this transaction, the Company’s cash flows from operating activities before net change in working capital would have been higher by those amounts during the quarter as follows:

| (In millions of US Dollars, unless otherwise noted) | For the three months ended | |||||||||||

| Illustration of impact due to copper advanced sales program | March 31, 2018 | June 30, 2018 | September 30, 2018 | December 31, 2018 | March 31, 2019(6) | June 30, 2019(6) | Cumulative impact | |||||

| Copper pounds to be delivered per contract (millions) | 13.2 | 10.7 | 8.2 | 8.2 | 40.3 | |||||||

| Cash flows from operating activities before net change in working capital (5) | $ | 206.4 | $ | 157.5 | $ | 86.6 | $ | 115.8 | n/a | n/a | ||

| Impact due to copper advanced sales program | (125.0 | ) | — | 41.7 | 33.3 | 25.1 | 24.9 | — | ||||

| Cash flows from operating activities before net change in working capital, normalized for the copper advanced sales program (5) | $ | 81.4 | $ | 157.5 | $ | 128.3 | $ | 149.1 | n/a | n/a | ||

- Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion included at the end of this press release under the heading “Non-GAAP Financial Measures and Additional Line Items and Subtotals in Financial Statements”. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q42018 and in Section 11 of the Company’s fourth quarter 2018 Management’s Discussion & Analysis, which has been filed on SEDAR. Adjusted operating cash flows are adjusted for payments not reflective of current period operations and advance payments received pursuant to metal purchase agreements.

- For illustration purposes only; the Company intends to provide information each subsequent period reflecting the impact due to the copper advanced sales program over its term.

A non-cash impairment reversal of $150.0 million in respect of Jacobina was recognized following the significant increase in mineral reserves and mineral resources, which extends the life of the mine, and other operational improvements. The reversal was offset by non-cash accounting impairments of $151.0 million in respect of Minera Florida and $45.0 million in respect of goodwill on the acquisition of Canadian Malartic. No indicators of impairment or reversal were identified for the other operating mine sites. In addition, the current quarter includes an income tax expense of $33.3 million incurred and payable at the end of the year, following an administrative interpretation of relevant tax legislation and approach by Brazilian tax authorities under that tax legislation in December. The expense was unexpected, not consistent with the Company's interpretations of the tax legislation and inconsistent with past practice. The Company has made the payment so as to avoid penalties and interest but in respect of which, the Company is pursuing legal recourse and remedies. Adjustments to net earnings during the periods noted below are as follows:

Summary of Certain Non-Cash and Other Items Included in Net Loss

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | |||||||

| 2018 | 2017 | 2018 | 2017 | |||||

| Non-cash unrealized foreign exchange losses/(gains) | 3.2 | (1.2 | ) | 9.5 | 15.0 | |||

| Share-based payments/mark-to-market of deferred share units | (0.5 | ) | 3.7 | 5.3 | 12.8 | |||

| Mark-to-market (gains) losses on derivative contracts | (2.6 | ) | 12.8 | (9.4 | ) | 9.3 | ||

| Net mark-to-market losses (gains) on investment and other assets | 0.9 | (0.5 | ) | 9.8 | 2.5 | |||

| Revision in estimates and liabilities including contingencies | 0.3 | 1.9 | 12.9 | (26.6 | ) | |||

| Gain on sale of subsidiaries | (2.7 | ) | - | (73.7 | ) | - | ||

| Impairment (reversal) of mining and non-operational mineral properties, and properties held for sale | (13.0 | ) | 356.4 | 250.0 | 356.5 | |||

| Impairment of goodwill | 45.0 | - | 45.0 | - | ||||

| Financing costs paid on early note redemption | - | - | 14.7 | - | ||||

| Reorganization costs | 2.2 | 1.2 | 10.1 | 4.8 | ||||

| Other provisions, write-downs and adjustments | 16.4 | (0.5 | ) | 34.9 | 18.5 | |||

| Non-cash tax unrealized foreign exchange losses/(gains) | (43.2 | ) | 11.6 | 151.9 | 9.9 | |||

| Income tax effect of adjustments and other one-time tax adjustments | 81.6 | (141.3 | ) | (64.4 | ) | (143.4 | ) | |

| TOTAL ADJUSTMENTS(7) | 87.6 | 244.1 | 396.5 | 259.3 | ||||

| Increase to net loss per share | 0.09 | 0.26 | 0.42 | 0.27 | ||||

- For the three months ended December 31, 2018, net loss from operations, attributable to Yamana equity holders, would be adjusted by an increase of $87.6 million (2017 - $244.1 million). For the twelve months ended December 31, 2018, net earnings from operations, attributable to Yamana equity holders, would be adjusted by an increase of $396.5 million (2017 - $259.3 million).

In the fourth quarter of 2018, the Company completed the previously announced sale of the Gualcamayo mine in Argentina to Mineros S.A. The Company received consideration with a total value of approximately $85 million, which includes cash proceeds of $30 million; $30 million in additional payments related to the advancement of the Deep Carbonates project; and royalties related to metal production at Gualcamayo and the Deep Carbonates project. The consideration received offers significant upside in the case of new oxide discoveries, higher gold prices and/or development of the Deep Carbonates project, thereby preserving considerable optionality. The transaction also includes an option for Mineros to acquire up to a 51% interest in the La Pepa project in Chile.

The Company's exploration programs continue to deliver on mineral resources discovery and mineral reserve replacement and growth. The exploration program successfully increased gold mineral reserves to replace 2018 mineral depletion, excluding assets that were disposed of in 2018. On the same basis, measured and indicated gold mineral resources and inferred mineral resources increased by 5% and 7%, respectively. For silver, mineral reserves decreased 3%, measured and indicated mineral resources decreased 4% and inferred mineral resources decreased 3%. For copper, mineral reserves increased 6%, measured and indicated mineral resources increased 55% and inferred mineral resources increased 211%.

The balance sheet as at December 31, 2018 includes cash and cash equivalents of $98.5 million with available credit of $705.0 million for total liquidity of $803.5 million. Net debt(4) as at December 31, 2018, was $1.66 billion.

Daniel Racine, Yamana’s President and Chief Executive Officer, commented as follows: “In 2018 we achieved another year of exceeding our production guidance for all metals and at costs better than or in line with our guidance. Gold and copper exceeded the increased guidance levels we announced in October, while silver production exceeded the guidance that was lowered at that time. Our operational performance would not have been possible without our success in delivering Cerro Moro on time and on budget and exceeding expectations on both production and costs through the first six months of commercial production.

Throughout the year we also advanced several strategic initiatives, including closing the sale of the Canadian Malartic exploration properties, the Gualcamayo mine and completion of the business combination between Brio Gold and Leagold in addition to the ongoing evaluation and engagement in discussions relating to scenarios to develop Agua Rica.

Overall, we remain in a strong position to carry the Company’s health and safety, operational, and balance sheet momentum into 2019.”

DEVELOPMENT, OPTIMIZATION, AND STRATEGIC INITIATIVES

Chapada: The Company continues to advance its exploration program with the objective of identifying higher-grade copper and gold opportunities that are near the Chapada mine, completing infill drilling of the Sucupira and Baru deposits which would lead to a pit expansion, and advancing district scale targets. Mineralization has been identified along a 15-kilometre trend with numerous prospective areas under consideration for further drilling. Infill drilling in the Baru area is expected to reduce stripping ratios for the Sucupira deposit and drilling on oxide mineralization, such as Hidrotermalito, brings the potential for heap leaching opportunities that could complement the Suruca Oxides Project. Notwithstanding the focus on the exploration potential to discover higher-grade copper and gold areas, the Company has also advanced other projects that are expected to further enhance returns from the Chapada mine.

To this end, the Company has completed studies and evaluations on several of the development opportunities at Chapada and has embarked on a feasibility-level review of a three-phase plan at Chapada. These opportunities range in scope from plant optimization initiatives to enhance copper and gold recoveries, to plant expansions to bring forward cash flows, and pit wall pushbacks to expose higher-grade zones. The study and evaluations include third party design and engineering, estimates of capital expenses, production and operating cost forecasts.

Given the nature of the opportunities, the projects can be considered on their own or as part of a phased development plan. This flexibility in approach allows the Company to balance the maximization of value at Chapada with the allocation of capital across the broader Company portfolio.

The Phase 1- Plant Optimization Work, with expected recovery improvements in the range of 2% for both metals, has been approved. Associated capital expenditures are estimated to be approximately $9 million. The Company is continuing to prioritize engineering for long lead-time equipment for Phase 1 and, during the fourth quarter, the flotation circuit expansion continued as planned with the installation of six new DFR flotation cells. Commissioning is scheduled for mid-2019.

Engineering is being advanced for Phases 2 and 3, an expansion of the Chapada mill, and pushback of the Chapada pit wall to expose higher grade Sucupira ores, respectively. While review of these projects are in the evaluation process, the Company does not anticipate the allocation of significant expansionary capital for these projects before 2021.

Based on the work completed to date, the Company estimates the phased plan will provide the foundation to sustain annual production in the range of 100,000 to 110,000 ounces of gold (not including contributions to gold production from identified higher-grade areas of Suruca, which is a gold-only ore body) and 150 to 160 million pounds of copper until at least 2034. This represents an opportunity to deliver significant cash flow increases and cash flow returns on invested capital and an increase to the production outlook, as disclosed in the Chapada NI 43-101 Technical Report dated March 21, 2018. Further project details are expected to be available in mid-2019 with the completion of the Feasibility Study. A development decision for Phase 2 is expected to follow in 2020.

Suruca - Gold-Only Oxide and Sulphide Development Opportunity

Concurrent with the multi-phase plan for Chapada, development of the gold-only Suruca oxides deposit continues to be evaluated as a standalone heap leach operation for which a feasibility study level update has been completed. Furthermore, the Suruca Sulphides project has been updated in the 2018 exploration results for these ore bodies resulting in an increase of gold mineral resources. The integrated scenario for Suruca ore bodies includes processing of the oxides through a heap leach and processing of the gold-only sulphides through a carbon-in-leach ("CIL") plant located at Chapada. Alternatives to process the sulphide portion of Suruca earlier in the life of mine are currently being contemplated, including an exploration program designed to test further extensions of the sulphide mineralization and metallurgical test work. The Company expects to continue this development program through 2019 in order to build on the results from the 2017 and 2018 programs, which resulted in extensions of the oxide and sulphide deposits.

Canadian Malartic: The Canadian Malartic Extension Project is continuing according to plan, with contributions from Barnat expected to begin in 2019 with more meaningful contributions in 2020. On a 50% basis, expansionary capex is expected to be $37 million, of which $34 million is earmarked for the extension project in 2019. Work in the fourth quarter, continued to focus on the highway 117 road deviation, pit preparation and tailings expansion.

OTHER OPTIMIZATION AND MONETIZATION INITIATIVES

Agua Rica: The Company is continuing its evaluation of and engagement in discussions relating to various development scenarios for Agua Rica. This includes an integration scenario between Agua Rica and Alumbrera pursuant to which a joint pre-feasibility study has started. Concurrently, the Company continues the engagement with the other partners of Alumbrera and with various other stakeholders at the national and provincial level. Separately, the Company continues to advance alternatives for the development of Agua Rica. This includes technical work and analysis for project development options for Agua Rica, as well as the review and consideration of various strategic alternatives, all in an effort to advance the project and surface value. Considerable effort has been undertaken to advance two development scenarios, one a large-scale open pit integrated operation and the other an initially smaller scale but scalable standalone operation. The large-scale open pit scenario contemplates the aforementioned integration with the neighboring Alumbrera mine in which the Company holds a 12.5% interest and for which it expects to complete an updated pre-feasibility study during the first half of 2019.

Suyai: The Company previously completed a scoping study that evaluated two options for ore processing, both of which provide favorable project economics. The first considered the construction of a CIL processing facility for the on-site production of gold and silver in the form of doré. The second considered the construction of a processing facility for on-site production of gold and silver contained in a high-grade concentrate, which would be shipped abroad for subsequent precious metal recovery. Both approaches considered an identical underground configuration with average annual production expected to be in excess of 200,000 ounces of gold and 300,000 ounces of silver. The Company believes both scenarios address past concerns regarding open pit mining, and the development scenario that includes production of an on-site concentrate addresses many of the past concerns regarding the use of cyanide, and would potentially meet provincial regulations currently in place in Chubut. The Company will work with local stakeholders to obtain and sustain its social license should the project progress to a more advanced stage.

The Company continues to pursue development plans and other strategic alternatives for the project. Given the extensive amount of work performed, to date the existing scoping study could rapidly progress to a feasibility study allowing for the project to be developed in a short time frame. The Suyai project is one of the highest gold grade development-ready projects in the Americas. While a financial adviser has not been retained at this time, the Company is evaluating its strategic alternatives in addition to development of the project.

Monument Bay: The Monument Bay deposits are hosted in the Stull Lake Greenstone Belt comprised by three volcanic assemblages, ranging in age from 2.85 to 2.71 Ga. Gold and tungsten mineralization occurs along the steeply north dipping Twin Lakes Shear Zone and the AZ Sheer Zone.

In 2018 approximately 16,270 metres of drilling were completed on the Monument Bay project. The focus was testing targets near the Twin Lakes deposit and testing regional targets. In addition, during the period a new geological interpretation of the deposit was formed and is expected to form the basis for an updated block model and mineral resource estimate. Groundwork is continuing and generating prospects for follow-up testing in 2019.

On September 13, 2018, the Company signed an Exploration Agreement with Red Sucker Lake First Nations in relation to the Monument Bay exploration site in Northern Manitoba. This is an important step allowing the Company to solidify a strategic collaboration with this community, as it continues to advance the project.

Other: The Company continues to pursue development and strategic initiatives for the 56.7% held Agua De La Falda joint venture with Codelco, located in northern Chile. The historical Jeronimo Feasibility Study focused on maximizing production from the sulfide deposits. The Company completed the study of a low capital start-up project based on the remaining oxide inventory with positive results and is evaluating exploration plans on the highly prospective claims surrounding the mine. Agua De La Falda has installed processing capacity and infrastructure.

YEAR END MINERAL RESERVES AND MINERAL RESOURCES SUMMARY

As at December 31, 2018.

| Proven and Probable Mineral Reserves | |||

| Tonnes (000s) | Grade (g/t) | Contained oz. (000s) | |

| Gold | 865,653 | 0.45 | 12,496 |

| Silver | 11,736 | 174.5 | 65,828 |

| Tonnes (000s) | Grade (%) | Contained lbs (M) | |

| Copper | 673,357 | 0.25 | 3,784 |

| Measured and Indicated Mineral Resources | |||

| Tonnes (000s) | Grade (g/t) | Contained oz. (000s) | |

| Gold | 771,033 | 0.64 | 15,941 |

| Silver | 13,807 | 84.1 | 37,317 |

| Tonnes (000s) | Grade (%) | Contained lbs (M) | |

| Copper | 431,522 | 0.22 | 2,090 |

| Inferred Mineral Resources | |||

| Tonnes (000s) | Grade (g/t) | Contained oz. (000s) | |

| Gold | 333,516 | 0.95 | 10,162 |

| Silver | 25,770 | 64.4 | 53,377 |

| Tonnes (000s) | Grade (%) | Contained lbs (M) | |

| Copper | 156,928 | 0.23 | 785 |

Additional details relating to the Company’s mineral reserve and mineral resource estimates as at December 31, 2018 are presented below.

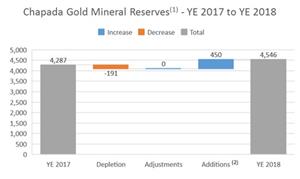

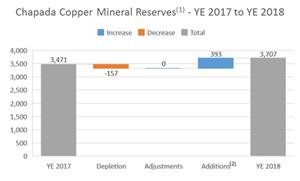

Chapada, Brazil

As the result of the continued definition and expansion of the Sucupira mineral reserve, immediately adjacent to the main Chapada pit, gold and copper mineral reserves increased by 6% and 7%, respectively, over the prior year, representing a significant overall improvement over depletion in 2018. Gold measured and indicated mineral resources increased by 20%, while copper increased by 54% compared to the prior year, following the drilling for extensions of the mineral envelopes at Corpo Sul under the Bois River and Santa Cruz mineral resources, in addition to Sucupira and Baru. Gold inferred mineral resources are unchanged from 2017, while copper increased significantly.

The following chart summarizes the changes in gold mineral reserves at Chapada as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/a2b0885d-7377-4c2d-a074-05caed4a106c

- Gold mineral reserves in thousands of ounces.

- Additions at Sucupira and Baru as a result of infill drilling and engineering studies.

The following chart summarizes the changes in copper mineral reserves at Chapada as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/945eebb7-1176-4393-8531-e046c6728fba

- Copper mineral reserves in millions of pounds.

- Additions at Sucupira and Baru as a result of infill drilling and engineering studies.

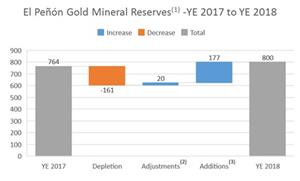

El Peñón, Chile

El Peñón's mineral reserves increased by 5% for gold and 6% for silver over mining depletion in 2018. Gold measured and indicated mineral resources increased by 24%, while silver increased by 30% compared to the prior year, continuing from numerous secondary vein structures in the east mine area. Lower gold and silver inferred mineral resources reflect conversion to indicated mineral resources.

The following chart summarizes the changes in gold mineral reserves at El Peñón as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/25d422cc-335c-4a1f-842e-7e1d58bd7d9b

- Gold mineral reserves in thousands of ounces.

- Adjustments with optimization of mine design.

- Additions with infill drilling and conversion of the low grade stockpile after sampling and metallurgical testing.

The following chart summarizes the changes in silver mineral reserves at El Peñón as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/e873b1d4-bbfa-481d-9174-8a57c021c142

- Silver mineral reserves in thousands of ounces.

- Adjustments with optimization of mine design.

- Additions with infill drilling and conversion of the low grade stockpile after sampling and metallurgical testing.

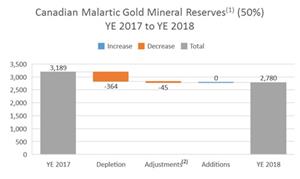

Canadian Malartic including Odyssey, Canada (50%)

Gold mineral reserves reflect depletion associated with 2018 production at Canadian Malartic. Separately, much of the mineral resource accretion in 2018 is associated with the East Malartic underground. Additional drilling, also at East Malartic and Odyssey, contributed to the 33% increase in gold measured and indicated mineral resources and the 1% increase in gold inferred mineral resources.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/93a3cf9e-9188-461c-a270-206a08d47e6c

- Gold mineral reserves in thousands of ounces.

- Adjustments to pit design and cut-off grade.

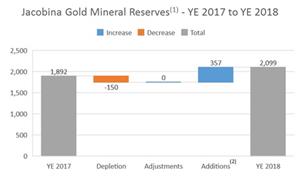

Jacobina, Brazil

Jacobina successfully increased gold mineral reserves by 11% over 2018 mining depletion. Measured and indicated mineral resources are in line with 2017 and reflect the conversion to mineral reserves. Inferred mineral resources increased significantly by over 800,000 ounces of gold, despite increasing the cut-off grade from 0.5 g/t to 1.0 g/t. The exploration program at Jacobina also achieved the main goal for the year which was to identify and define high-grade mineralization close to current infrastructure. Several zones were defined including down dip of João Belo, Morro do Vento South and the northern portion, Serra do Corrego and Canavieiras Sul. In 2019, the exploratory drilling will continue focusing on the extension of these high-grade zones, including the south extension of João Belo. The definition drilling program will continue in 2019 to increase confidence in reef geometry and fault locations for sectors planned to be mined within the next three years.

The following chart summarizes the changes in gold mineral reserves at Jacobina as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/286fc621-c8b1-438d-8505-662cb7a8f53f

- Gold mineral reserves in thousands of ounces.

- Additions mostly at Morro do Vento with additional reefs.

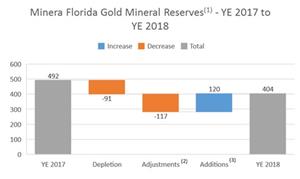

Minera Florida, Chile

At Minera Florida, the decrease in mineral reserves is a result of mine depletion and the application of an updated geological model and more conservative design parameters with higher cut-off grades, especially around the historic mining areas. Gold measured and indicated mineral resources increased by 5%, resulting from an upgrade of certain inferred mineral resources. The PVS and Pataguas zones will be the main targets of 2019 exploration drilling.

The following chart summarizes the changes in gold mineral reserves at Minera Florida as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/c9fc2b40-b146-4ad3-82a3-3daed9c27d8b

- Gold mineral reserves in thousands of ounces.

- Adjustment to geological interpretation and cut-off grade.

- Additions due to infill drilling.

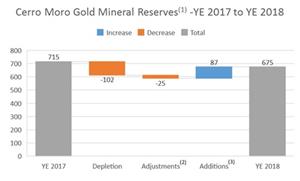

Cerro Moro, Argentina

At Cerro Moro, increases in gold and silver mineral reserves partially offset depletion associated with 2018 production. The main increases came from the discovery of new high grade, near surface vein Veronica and the extensions of Nini. Also drilling in the core mine area returned mineralized intercepts at Michelle, Milagros and Tres Lomas which will be followed-up upon in 2019. Updated economical parameters with higher cut-off grades for both mineral reserves and mineral resources had the impact of reducing tonnage, but increasing the overall grade. Due to the previous focus of the site on project development, start-up and ramp-up of operations, long-term exploration effort began in 2018 and as result the current mineral resources do not consider drilling results for the last four months of the year. These results are in the process of being analyzed and are expected to provide good quality targets for 2019. This ultimately resulted in 13% lower gold for remaining measured and indicated mineral resources and 24% lower inferred mineral resources. Regional exploration south of the mine area intercepted a wide zone of mineralization at Naty. These zones are expected to undergo further drilling in 2019, as part of the increased exploration budget allocation to the mine.

The following chart summarizes the changes in gold mineral reserves at Cerro Moro as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/ce40cb4e-75b5-4d71-a621-201a6ee21ea5

- Gold mineral reserves in thousands of ounces.

- Adjustments to cut-off grade and mine design parameters.

- Additions of new zones, especially Veronica and Nini.

The following chart summarizes the changes in silver mineral reserves at Cerro Moro as at December 31, 2018 compared to the prior period.

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/789900bd-8843-4438-b4bf-2e0fbf3aff8b

- Silver mineral reserves in thousands of ounces.

- Adjustments to cut-off grade and mine design parameters.

- Additions of new zones, especially Veronica and Nini.

KEY STATISTICS

Key operating and financial statistics for the fourth quarter and full year 2018 are outlined in the following tables.

Financial Summary

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | |||||||

| (In millions of US Dollars except for shares and per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||

| Revenue | 483.4 | 478.8 | 1,798.5 | 1,803.8 | ||||

| Cost of sales excluding depletion, depreciation and amortization | (266.2 | ) | (264.7 | ) | (1,010.0 | ) | (1,042.4 | ) |

| Depletion, depreciation and amortization | (130.9 | ) | (100.9 | ) | (438.3 | ) | (426.8 | ) |

| Total cost of sales | (397.1 | ) | (365.6 | ) | (1,448.3 | ) | (1,469.2 | ) |

| Mine operating earnings (loss) | 40.3 | (143.7 | ) | 201.2 | 77.7 | |||

| General and administrative expenses | (21.0 | ) | (34.0 | ) | (91.8 | ) | (113.6 | ) |

| Exploration and evaluation expenses | (3.6 | ) | (7.0 | ) | (13.0 | ) | (21.2 | ) |

| Net loss from operations | (61.4 | ) | (198.3 | ) | (297.7 | ) | (198.1 | ) |

| Net loss attributable to Yamana Gold equity holders | (61.4 | ) | (188.6 | ) | (284.6 | ) | (188.5 | ) |

| Net loss from operations, per share - basic and diluted(1) | (0.06 | ) | (0.20 | ) | (0.30 | ) | (0.20 | ) |

| Cash flow generated from operations after changes in non-cash working capital | 114.7 | 158.5 | 404.2 | 484.0 | ||||

| Cash flow from operations before changes in non-cash working capital(2) | 115.8 | 122.3 | 566.3 | 498.0 | ||||

| Revenue per ounce of gold | 1,223 | 1,269 | 1,263 | 1,250 | ||||

| Revenue per ounce of silver | 14.59 | 16.46 | 15.37 | 16.80 | ||||

| Revenue per pound of copper | 2.56 | 2.36 | 2.70 | 2.36 | ||||

| Average realized gold price per ounce | 1,226 | 1,286 | 1,267 | 1,264 | ||||

| Average realized silver price per ounce | 14.59 | 16.49 | 15.37 | 16.83 | ||||

| Average realized copper price per pound | 2.90 | 3.02 | 2.99 | 2.78 | ||||

- For the three and twelve months ended December 31, 2018, the weighted average numbers of shares outstanding, basic and diluted, was 949,337 thousand and 949,030 thousand, respectively.

- Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion included at the end of this press release under the heading “Non-GAAP Financial Measures and Additional Line Items and Subtotals in Financial Statements”. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q42018 and in Section 11 of the Company’s fourth quarter 2018 Management’s Discussion & Analysis, which has been filed on SEDAR.

Production, Financial and Operating Summary

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | |||||||

| Gold | 2018 | 2017 | 2018 | 2017 | ||||

| Total cost of sales per ounce sold - Yamana Mines | $ | 999 | $ | 929 | $ | 1,008 | $ | 973 |

| Total cost of sales per ounce sold - Total Yamana | $ | 1,010 | $ | 966 | $ | 1,031 | $ | 1,023 |

| Total cost of sales per ounce sold – consolidated | $ | 1,010 | $ | 980 | $ | 1,042 | $ | 1,038 |

| Co-product cash costs per ounce produced - Yamana Mines(1) | $ | 570 | $ | 612 | $ | 614 | $ | 621 |

| Co-product cash costs per ounce produced - Total Yamana(1) | $ | 610 | $ | 660 | $ | 649 | $ | 672 |

| All-in sustaining co-product costs per ounce produced - Yamana Mines(1) | $ | 763 | $ | 884 | $ | 816 | $ | 869 |

| All-in sustaining co-product costs per ounce produced - Total Yamana(1) | $ | 801 | $ | 899 | $ | 843 | $ | 888 |

| Silver | 2018 | 2017 | 2018 | 2017 | ||||

| Total cost of sales per ounce sold | $ | 14.23 | $ | 13.26 | $ | 15.58 | $ | 13.63 |

| Co-product cash costs per ounce produced(1) | $ | 7.12 | $ | 8.86 | $ | 8.25 | $ | 10.01 |

| All-in sustaining co-product costs per ounce produced(1) | $ | 9.57 | $ | 11.90 | $ | 10.81 | $ | 13.48 |

| Copper | 2018 | 2017 | 2018 | 2017 | ||||

| Total cost of sales per copper pound sold | $ | 1.87 | $ | 1.68 | $ | 1.80 | $ | 1.74 |

| Co-product cash costs per pound of copper produced(1) | $ | 1.50 | $ | 1.51 | $ | 1.51 | $ | 1.54 |

| All-in sustaining co-product costs per pound of copper produced(1) | $ | 1.86 | $ | 1.85 | $ | 1.90 | $ | 1.89 |

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | |||||||

| By-Product Costs | 2018 | 2017 | 2018 | 2017 | ||||

| By-product cash costs per gold ounce produced - Yamana Mines(1) | $ | 420 | $ | 476 | $ | 445 | $ | 490 |

| All-in sustaining by-product costs per gold ounce produced - Yamana Mines(1) | $ | 657 | $ | 800 | $ | 696 | $ | 788 |

| By-product cash costs per silver ounce produced(1) | $ | 4.99 | $ | 7.44 | $ | 5.90 | $ | 8.58 |

| All-in sustaining by-product costs per silver ounce produced(1) | $ | 7.99 | $ | 11.05 | $ | 9.11 | $ | 12.65 |

- Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion included at the end of this press release under the heading “Non-GAAP Financial Measures and Additional Line Items and Subtotals in Financial Statements”. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q42018 and in Section 11 of the Company’s fourth quarter 2018 Management’s Discussion & Analysis, which has been filed on SEDAR.

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | ||||

| Gold Ounces | 2018 | 2017 | 2018 | 2017 | |

| Chapada | 40,841 | 36,578 | 121,003 | 119,852 | |

| El Peñón | 37,956 | 39,401 | 151,893 | 160,509 | |

| Canadian Malartic (50%) | 84,732 | 80,743 | 348,600 | 316,731 | |

| Jacobina | 37,071 | 34,566 | 144,695 | 135,806 | |

| Cerro Moro | 45,066 | - | 92,793 | - | |

| Minera Florida | 24,526 | 23,540 | 81,635 | 90,366 | |

| Production - Yamana Mines | 270,193 | 214,828 | 940,619 | 823,263 | |

| Gualcamayo | 22,291 | 44,778 | 92,285 | 154,052 | |

| Production - Total Yamana | 292,484 | 259,606 | 1,032,903 | 977,315 | |

| Three Months Ending Dec 31st | Twelve Months Ending Dec 31st | ||||

| Silver Ounces | 2018 | 2017 | 2018 | 2017 | |

| El Peñón | 1,186,789 | 1,052,423 | 3,903,961 | 4,282,339 | |

| Cerro Moro | 2,077,906 | - | 4,119,085 | - | |

| TOTAL | 3,264,695 | 1,052,423 | 8,023,046 | 4,282,339 | |

For a full discussion of Yamana’s operational and financial results and Mineral Reserve and Mineral Resource estimates please refer to the Company’s fourth quarter 2018 Management’s Discussion & Analysis and Consolidated Financial Statements which have been filed on SEDAR and are also available on the Company’s website.

| MINERAL RESERVE AND MINERAL RESOURCE ESTIMATES | |||||||||

| Mineral Reserves (Proven and Probable) | |||||||||

| The following table sets forth the Mineral Reserve estimates for the Company’s mineral projects as at December 31, 2018. | |||||||||

| Proven Mineral Reserves | Probable Mineral Reserves | Total Proven & Probable | |||||||

| Gold | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 8,435 | 0.39 | 106 | 294 | 0.37 | 4 | 8,728 | 0.39 | 109 |

| Canadian Malartic (50%) | 23,029 | 0.89 | 658 | 55,799 | 1.18 | 2,122 | 78,829 | 1.10 | 2,780 |

| Cerro Moro | 43 | 10.57 | 15 | 1,766 | 11.64 | 661 | 1,809 | 11.61 | 675 |

| Chapada Zones | 388,701 | 0.17 | 2,103 | 275,928 | 0.16 | 1,381 | 664,629 | 0.16 | 3,484 |

| Suruca Zones | 11,454 | 0.42 | 153 | 53,741 | 0.53 | 908 | 65,195 | 0.51 | 1,062 |

| Total Chapada | 400,155 | 0.18 | 2,256 | 329,669 | 0.22 | 2,289 | 729,824 | 0.19 | 4,546 |

| El Peñón Ore | 693 | 5.11 | 114 | 3,738 | 5.38 | 646 | 4,431 | 5.33 | 760 |

| El Peñón Stockpiles | 17 | 2.41 | 1 | 1,029 | 1.18 | 39 | 1,047 | 1.20 | 40 |

| Total El Peñón | 710 | 5.04 | 115 | 4,768 | 4.47 | 685 | 5,478 | 4.55 | 800 |

| Jacobina | 18,565 | 2.32 | 1,385 | 9,290 | 2.39 | 714 | 27,855 | 2.34 | 2,099 |

| Jeronimo (57%) | 6,350 | 3.91 | 798 | 2,331 | 3.79 | 284 | 8,681 | 3.88 | 1,082 |

| Minera Florida Ore | 690 | 3.61 | 80 | 2,512 | 3.54 | 286 | 3,202 | 3.56 | 366 |

| Minera Florida Tailings | 0 | 0.00 | 0 | 1,248 | 0.94 | 38 | 1,248 | 0.94 | 38 |

| Total Minera Florida | 690 | 3.61 | 80 | 3,760 | 2.68 | 324 | 4,449 | 2.82 | 404 |

| Total Gold Mineral Reserves | 457,977 | 0.37 | 5,413 | 407,677 | 0.54 | 7,083 | 865,653 | 0.45 | 12,496 |

| Agua Rica | 384,871 | 0.25 | 3,080 | 524,055 | 0.21 | 3,479 | 908,926 | 0.22 | 6,559 |

| Silver | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Cerro Moro | 43 | 620.7 | 857 | 1,766 | 653.3 | 37,102 | 1,809 | 652.6 | 37,959 |

| El Peñón Ore | 693 | 166.1 | 3,700 | 3,738 | 171.7 | 20,630 | 4,431 | 170.8 | 24,330 |

| El Peñón Stockpiles | 17 | 107.2 | 60 | 1,029 | 15.2 | 502 | 1,046 | 16.7 | 562 |

| Total El Peñón | 710 | 164.7 | 3,760 | 4,768 | 137.9 | 21,133 | 5,478 | 141.3 | 24,893 |

| Minera Florida Ore | 690 | 28.1 | 623 | 2,512 | 21.9 | 1,770 | 3,202 | 23.2 | 2,393 |

| Minera Florida Tailings | 0 | 0.0 | 0 | 1,248 | 14.6 | 584 | 1,248 | 14.6 | 584 |

| Total Minera Florida | 690 | 28.1 | 623 | 3,760 | 19.5 | 2,353 | 4,449 | 20.8 | 2,976 |

| Total Silver Mineral Reserves | 1,443 | 112.9 | 5,240 | 10,294 | 183.1 | 60,588 | 11,736 | 174.5 | 65,828 |

| Agua Rica | 384,871 | 3.7 | 46,176 | 524,055 | 3.3 | 56,070 | 908,926 | 3.5 | 102,246 |

| Copper | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | |

| Alumbrera (12.5%) | 8,435 | 0.40 | 74 | 294 | 0.38 | 3 | 8,728 | 0.40 | 77 |

| Chapada Zones | 388,701 | 0.25 | 2,138 | 275,928 | 0.26 | 1,568 | 664,629 | 0.25 | 3,707 |

| Suruca Zones | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0 |

| Total Chapada | 388,701 | 0.25 | 2,138 | 275,928 | 0.26 | 1,568 | 664,629 | 0.25 | 3,707 |

| Total Copper Mineral Reserves | 397,136 | 0.25 | 2,212 | 276,222 | 0.26 | 1,571 | 673,357 | 0.25 | 3,784 |

| Agua Rica | 384,871 | 0.56 | 4,779 | 524,055 | 0.43 | 5,011 | 908,926 | 0.49 | 9,790 |

| Zinc | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | |

| Minera Florida Ore | 690 | 1.53 | 23 | 2,512 | 1.13 | 62 | 3,202 | 1.21 | 85 |

| Minera Florida Tailings | 0 | 0.00 | 0 | 1,248 | 0.58 | 16 | 1,248 | 0.58 | 16 |

| Total Zinc Mineral Reserves | 690 | 1.53 | 23 | 3,760 | 0.94 | 78 | 4,449 | 1.04 | 102 |

| Molybdenum | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | |

| Alumbrera (12.5%) | 8,435 | 0.013 | 2.45 | 294 | 0.014 | 0.09 | 8,728 | 0.013 | 2.54 |

| Total Moly Mineral Reserves | 8,435 | 0.013 | 2.45 | 294 | 0.014 | 0.09 | 8,728 | 0.013 | 2.54 |

| Agua Rica | 384,871 | 0.033 | 279 | 524,055 | 0.030 | 350 | 908,926 | 0.031 | 629 |

| Mineral Resources (Measured, Indicated, and Inferred) | |||||||||

| The following tables set forth the Mineral Resource estimates for the Company’s mineral projects as at December 31, 2018. | |||||||||

| Measured Mineral Resources | Indicated Mineral Resources | Total Measured & Indicated | |||||||

| Gold | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 6,792 | 0.39 | 85 | 1,917 | 0.54 | 33 | 8,709 | 0.42 | 117.8 |

| Arco Sul | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0.0 |

| Canadian Malartic (50%) | 1,885 | 1.36 | 83 | 13,615 | 1.80 | 786 | 15,500 | 1.74 | 868.7 |

| Cerro Moro | 18 | 10.83 | 6 | 1,224 | 5.14 | 202 | 1,241 | 5.22 | 208.4 |

| Chapada Zones | 58,885 | 0.12 | 222 | 363,929 | 0.14 | 1,676 | 422,814 | 0.14 | 1,897.8 |

| Suruca Zones | 1,284 | 0.39 | 16 | 81,039 | 0.54 | 1,416 | 82,323 | 0.54 | 1,432.0 |

| Total Chapada | 60,169 | 0.12 | 238 | 444,968 | 0.22 | 3,092 | 505,137 | 0.21 | 3,329.8 |

| El Peñón Mine | 232 | 8.02 | 60 | 1,579 | 5.88 | 298 | 1,811 | 6.15 | 358.0 |

| El Peñón Tailings | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0.0 |

| El Peñón Stockpiles | 0 | 0.00 | 0 | 1,019 | 1.13 | 37 | 1,019 | 1.13 | 37.0 |

| El Peñón Total | 232 | 8.04 | 60.0 | 2,598.0 | 4.0 | 336.0 | 2,830 | 4.35 | 396.0 |

| Jacobina | 24,999 | 2.48 | 1,994 | 15,711 | 2.45 | 1,238 | 40,710 | 2.47 | 3,232.0 |

| Jeronimo (57%) | 772 | 3.77 | 94 | 385 | 3.69 | 46 | 1,157 | 3.74 | 139.0 |

| La Pepa | 15,750 | 0.61 | 308 | 133,682 | 0.57 | 2,452 | 149,432 | 0.57 | 2,760.0 |

| Lavra Velha | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0.0 |

| Minera Florida | 1,207 | 5.87 | 228 | 3,829 | 4.79 | 590 | 5,036 | 5.05 | 817.0 |

| Monument Bay | 0 | 0.00 | 0 | 36,581 | 1.52 | 1,787 | 36,581 | 1.52 | 1,787.2 |

| Suyai | 0 | 0.00 | 0 | 4,700 | 15.00 | 2,286 | 4,700 | 15.00 | 2,286.0 |

| Total Gold Mineral Resources | 111,823 | 0.86 | 3,095 | 659,210 | 0.61 | 12,849 | 771,033 | 0.64 | 15,941 |

| Agua Rica | 27,081 | 0.14 | 120 | 173,917 | 0.14 | 776 | 200,998 | 0.14 | 896 |

| Silver | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Cerro Moro | 18 | 1,253.0 | 707 | 1,224 | 381.2 | 14,997 | 1,241 | 393.5 | 15,704 |

| El Peñón Mine | 232 | 194.6 | 1,450 | 1,579 | 207.1 | 10,512 | 1,811 | 205.4 | 11,962 |

| El Peñón Tailings | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0.00 | 0.0 | 0 |

| El Peñón Stockpiles | 0 | 0.00 | 0 | 1,019 | 28.80 | 942 | 1,019 | 28.8 | 942 |

| El Peñón Total | 232 | 194.6 | 1,450 | 2,598 | 137.1 | 11,454 | 2,830 | 141.8 | 12,904 |

| Minera Florida | 1,207 | 41.0 | 1,592 | 3,829 | 29.2 | 3,594 | 5,036 | 32.0 | 5,186 |

| Suyai | 0 | 0.0 | 0 | 4,700 | 23.0 | 3,523 | 4,700 | 23.0 | 3,523 |

| Total Silver Mineral Resources | 1,457 | 80.1 | 3,749 | 12,351 | 84.5 | 33,568 | 13,807 | 84.1 | 37,317 |

| Agua Rica | 27,081 | 2.4 | 2,042 | 173,917 | 2.9 | 16,158 | 200,998 | 2.8 | 18,200 |

| Copper | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 6,792 | 0.37 | 55 | 1,917 | 0.24 | 10 | 8,709 | 0.34 | 65 |

| Chapada Zones | 58,885 | 0.20 | 261 | 363,929 | 0.22 | 1,765 | 422,814 | 0.22 | 2,025 |

| Suruca Zones | 0 | 0.00 | 0 | 0 | 0 | 0 | 0 | 0.00 | 0 |

| Total Chapada | 58,885 | 0.20 | 261 | 363,929 | 0.22 | 1,765 | 422,814 | 0.22 | 2,025 |

| Total Copper Mineral Resources | 65,676 | 0.22 | 316 | 365,846 | 0.22 | 1,775 | 431,522 | 0.22 | 2,090 |

| Agua Rica | 27,081 | 0.45 | 266 | 173,917 | 0.38 | 1,447 | 200,998 | 0.39 | 1,714 |

| Zinc | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Minera Florida | 1,207 | 2.22 | 62 | 3,829 | 1.63 | 138 | 5,036 | 1.77 | 197 |

| Total Zinc Mineral Resources | 1,207 | 2.22 | 62 | 3,829 | 1.63 | 138 | 5,036 | 1.77 | 197 |

| Molybdenum | Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 6,192 | 0.014 | 1.94 | 462 | 0.013 | 0.13 | 6,654 | 0.014 | 2.07 |

| Total Moly Mineral Resources | 6,192 | 0.014 | 1.94 | 462 | 0.013 | 0.13 | 6,654 | 0.014 | 2.07 |

| Agua Rica | 27,081 | 0.049 | 29 | 173,917 | 0.037 | 142 | 200,998 | 0.039 | 172 |

| Inferred Mineral Resources | |||

| Gold | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 848 | 0.46 | 13 |

| Arco Sul | 5,000 | 4.02 | 646 |

| Canadian Malartic (50%) | 36,210 | 1.99 | 2,319 |

| Cerro Moro | 1,706 | 3.84 | 211 |

| Chapada Zones | 156,081 | 0.08 | 422 |

| Suruca Zones | 12,565 | 0.48 | 194 |

| Total Chapada | 168,646 | 0.11 | 616 |

| El Peñón Mine | 2,953 | 7.25 | 689 |

| El Peñón Tailings | 13,767 | 0.55 | 245 |

| El Peñón Stockpiles | 0 | 0.00 | 0 |

| El Peñón Total | 16,719 | 1.74 | 933 |

| Jacobina | 12,145 | 2.58 | 1,008 |

| Jeronimo (57%) | 1,118 | 4.49 | 161 |

| La Pepa | 37,900 | 0.50 | 620 |

| Lavra Velha | 3,934 | 4.29 | 543 |

| Minera Florida | 6,445 | 5.01 | 1,038 |

| Monument Bay | 41,946 | 1.32 | 1,781 |

| Suyai | 900 | 9.90 | 274 |

| Total Gold Mineral Resources | 333,516 | 0.95 | 10,162 |

| Agua Rica | 642,110 | 0.12 | 2,444 |

| Silver | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | |

| Cerro Moro | 1,706 | 257.8 | 14,139 |

| El Peñón Mine | 2,953 | 254.8 | 24,190 |

| El Peñón Tailings | 13,767 | 18.9 | 8,380 |

| El Peñón Stockpiles | 0 | 0.0 | 0 |

| El Peñón Total | 16,719 | 60.6 | 32,570 |

| Minera Florida | 6,445 | 29.4 | 6,093 |

| Suyai | 900 | 21.0 | 575 |

| Total Silver Mineral Resources | 25,770 | 64.4 | 53,377 |

| Agua Rica | 642,110 | 2.3 | 48,124 |

| Copper | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 848 | 0.21 | 4 |

| Chapada Zones | 156,081 | 0.23 | 781 |

| Suruca Zones | 0 | 0 | 0 |

| Total Chapada | 156,081 | 0.23 | 781 |

| Total Copper Mineral Resources | 156,928 | 0.23 | 785 |

| Agua Rica | 642,110 | 0.34 | 4,853 |

| Zinc | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | |

| Minera Florida | 6,445 | 1.32 | 187 |

| Total Zinc Mineral Resources | 6,445 | 1.32 | 187 |

| Molybdenum | Tonnes | Grade | Contained |

| (000's) | (g/t) | oz. (000's) | |

| Alumbrera (12.5%) | 85 | 0.014 | 0.03 |

| Total Molybdenum Mineral Resources | 85 | 0.014 | 0.03 |

| Agua Rica | 642,110 | 0.034 | 480 |

Mineral Reserve and Mineral Resource Reporting Notes

1. Metal Price, Cut-off Grade, Metallurgical Recovery:

| Mine | Mineral Reserves | Mineral Resources | ||

| Alumbrera Projects (12.5%) | ||||

| Alumbrera Deposit | Price assumption: $1,250 gold, $2.91 copper | Price assumption: $1,250 gold, $2.95 copper | ||

| Underground cut-off at 0.5% copper equivalent | Underground cut-off at 0.43% copper equivalent | |||

| Metallurgical recoveries average 87.85% for copper and 72.31% for gold | ||||

| Bajo El Durazno Deposit | N/A | Price assumption: $1,250 gold, $2.95 copper | ||

| 0.74 g/t Aueq cutoff within underground economic envelope | ||||

| Arco Sul | N/A | Price assumption: $1,500 gold | ||

| 2.5 g/t Au cutoff | ||||

| Canadian Malartic (50%) | Price assumption: $1,200 gold | Price assumption: $1,200 gold | ||

| Open pit cut-off grades range from 0.374 to 0.384 g/t Au | Cut-off grades range from 0.35 g/t Au inside pit to 1.0 g/t Au outside or below pit | |||

| Metallurgical recoveries for gold range from 87% to 96.7% depending on zone | Underground Cut-off grade at Odyssey is 1.15 g/t Au (stope optimized) and at East Malartic Underground is 1.25 g/t Au (stope optimized) | |||

| Cerro Moro | Price assumption: $1,250 gold and $18.00 silver | Price assumption: $1,600 gold and $24.00 silver | ||

| Open pit cut-off at 3.27 g/t gold and Underground cut-off at 5.71 g/t gold | 3.0 g/t Aueq cut-off | |||

| Metallurgical recoveries average 95% for gold and 93% for silver | ||||

| Chapada | ||||

| Chapada Zone | Price assumption: $1,250 gold, $3.00 copper | Price assumption: $1,600 gold , $4.00 copper | ||

| Open pit cut-off at $4.06/t (Main Pit, Corpo Sul, Cava Norte and Sucupira) | Open pit cut-off at $4.06/t (Chapada pits and Suruca SW) | |||

| Metallurgical recoveries at Chapada are dependent on zone and average 83.11% for copper and 56.94% for gold | Metallurgical recoveries at Chapada are dependent on zone and average 83.11% for copper and 56.94% for gold | |||

| Suruca Zone | Price assumption: $1,300 gold | Price assumption: $1,600 gold | ||

| Cut-off grade 0.19 g/t gold for Suruca oxide | Cut-off grade 0.16 g/t gold for Suruca oxide | |||

| Cut-off grade 0.3 g/t gold for Suruca sulfide | Cut-off grade 0.23 g/t gold for Suruca sulphide | |||

| Metallurgical recoveries for Suruca oxide average 85% for gold | Metallurgical recoveries for Suruca oxide average 85% for gold | |||

| Metallurgical recoveries for Suruca sulphide average 88% for gold | Metallurgical recoveries for Suruca sulphide average 88% for gold | |||

| El Peñón | Price Assumption:$1,250 gold, $18.00 silver | Price Assumption:$1,600 Au, $24.00 Ag | ||

| Open Pit cut-off at 1.75 g/t gold equivalent | Underground cut-off at 2.78 g/t gold equivalent except for Pampa Agusta Victoria (2.88 g/t), Chiquilla Chica (2.87 g/t), Laguna (2.85 g/t ) | |||

| Underground cut-off ranging from 3.57 g/t gold equivalent to 3.70 g/t gold equivalent | Fortuna-Dominador zones (2.84 g/t). Mill recoveries of 95% and 86.5% used for Mineral Resource Estimation | |||

| Low grade stockpiles cut-off 0.95 g/t gold equivalent | Mineral Resources contained in tailings and stockpiles reported at cut-offs of 05.0 g/t and 0.79 g/t gold equivalent respectively | |||

| Metallurgical recoveries for open pit ores range from 89.0% to 95.6% for gold and from 80.7% to 97.7% for silver | Metallurgical recoveries range from 87.2% to 99.0% for gold and from 59.8% to 92.6% for silver | |||

| Metallurgical recoveries for underground ores range from 87.2% to 99.0% for gold and from 59.8% to92.6% for silver | Metallurgical recoveries for tailings estimated to be 60% for gold and 30% for silver | |||

| Metallurgical recoveries for low grade stockpiles are 95.2% for gold and83.0% for silver | Metallurgical recoveries for stockpiles estimated to be 88.0% for gold and 80.8% for silver | |||

| Jacobina | Price assumptions: $1,250 gold | Price assumptions: $1600 gold | ||

| Underground cut-off grade is 1.20 g/t gold | Underground cut-off grade is 1.0 g/t gold with a minimum mining width of 1.5 metres | |||

| Metallurgical recovery is 96% | ||||

| Jeronimo (57%) | Price Assumption: $900 Au | |||

| Cut-off grade at 2.0 g/t gold | Cut-off grade at 2.0 g/t gold | |||

| Metallurgical recovery for Au is 86%. | ||||

| La Pepa | N/A | Price Assumption: $780 Au | ||

| cut-off grade at 0.30 g/t gold | ||||

| Lavra Velha | N/A | Price assumption: $1,300 gold and $3.50 copper | ||

| cut-off grade at 0.2g/t gold and 0.1% copper | ||||

| Minera Florida | Price assumption: $1,250/oz gold, $18.00/oz silver and $1.25/lb Zn. | Price assumption: $1,250/oz gold, $18.00/oz silver and $1.25/lb Zn | ||

| Underground cut-offs for Las Pataguas Zone USD90.75/t and for the Core Mine Zones USD94.79/t | Underground cut-off grade is 2.50 g/t gold | |||

| Metallurgical recoveries are 90.16% for gold, 52.31% for silver and 68.80% for zinc | Metallurgical recoveries are 90.16% for gold, 52.31% for silver and 68.80% for zinc | |||

| Monument Bay | N/A | Price Assumption: $1,200 Au | ||

| Cut-off grades are 0.4 g/t gold and 0.7 g/t gold for the open pits and 4.0 g/t gold for underground | ||||

| Suyai | N/A | 5.0 g/t Au cut-off inside mineralized wireframe modeling | ||

| Agua Rica | Price assumption: $1,000/oz gold, $2.25/lb copper, $17.00/oz silver and $12.00/lb molybdenum | Cut-off grade at 0.2% Copper | ||

| Metallurgical recoveries are 84.9% for copper, 52.7% for gold, 67.6% for silver, 65.9% for zinc and 68.0% for molybdenum | ||||

| 2. All Mineral Reserves and Mineral Resources have been calculated in accordance with the standards of the Canadian Institute of Mining, Metallurgy and Petroleum and National Instrument 43-101, other than the estimates for the Alumbrera mine which have been calculated in accordance with the JORC Code which is accepted under NI 43-101. | ||||

| 3. All Mineral Resources are reported exclusive of Mineral Reserves. | ||||

| 4. Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability. | ||||

| 5. Mineral Reserves and Mineral Resources are reported as of December 31, 2018. | ||||

| 6. For the qualified persons responsible for the Mineral Reserve and Mineral Resource estimates at the Company’s material properties, see the qualified persons list below. | ||||

| Property | Qualified Persons for Mineral Reserves | Qualified Persons for Mineral Resources |

| Canadian Malartic | Sylvie Lampron, Canadian Malartic Corporation | Pascal Lehouiller, Canadian Malartic Corporation |

| Chapada | Luiz Pignatari, EDEM Engenharia | Felipe Machado de Araujo, Member of Chilean Mining Commission, Mineral Resources Coordinator Brazil, Yamana Gold Inc. |

| El Peñón | Sergio Castro, Yamana Gold Inc. | Jorge Camacho, Yamana Gold Inc. |

FOURTH QUARTER 2018 CONFERENCE CALL

The Company will host a conference call and webcast on Friday, February 15, 2019 at 9:00 a.m. ET.

Fourth Quarter and Full Year 2018 Conference Call Details

| Toll Free (North America): | 1-800-273-9672 | |

| Toronto Local and International: | 416-340-2216 | |

| Webcast: | www.yamana.com |

Conference Call Replay

| Toll Free (North America): | 1-800-408-3053 | |

| Toronto Local and International: | 905-694-9451 | |

| Passcode: | 6784586 |

The conference call replay will be available from 12:00 p.m. ET on February 15, 2019 until 11:59 p.m. ET on March 1, 2019.

Qualified Persons

Scientific and technical information contained in this Management’s Discussion and Analysis has been reviewed and approved by Sébastien Bernier (Senior Director, Geology and Mineral Resources). Sébastien Bernier is an employee of Yamana Gold Inc. and a "Qualified Person" as defined by Canadian Securities Administrators' National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

About Yamana

Yamana is a Canadian-based gold, silver and copper producer with a significant portfolio comprised of operating mines, development stage projects, and exploration and mineral properties throughout the Americas, mainly in Canada, Brazil, Chile and Argentina. Yamana plans to continue to build on this base through expansion and optimization initiatives at existing operating mines, development of new mines, the advancement of its exploration properties and, at times, by targeting other consolidation opportunities with a primary focus in the Americas. The Company is listed on the Toronto Stock Exchange (trading symbol "YRI") and the New York Stock Exchange (trading symbol "AUY").

FOR FURTHER INFORMATION PLEASE CONTACT:

Investor Relations

416-815-0220

1-888-809-0925

Email: investor@yamana.com

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This news release contains or incorporates by reference “forward-looking statements” and “forward-looking information” under applicable Canadian securities legislation within the meaning of the United States Private Securities Litigation Reform Act of 1995. Forward-looking information includes, but is not limited to information with respect to the Company’s strategy, plans or future financial or operating performance continued advancements at Chapada, Jacobina, Canadian Malartic, Cerro Moro, El Peñón and Minera Florida, expected production and costs, future work and drilling programs, and the potential for future additions to mineral resources and mineral reserves.. Forward-looking statements are characterized by words such as “plan,” “expect”, “budget”, “target”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the Company’s expectations in connection with the production and exploration, development and expansion plans at the Company's projects discussed herein being met, the impact of proposed optimizations at the Company's projects, changes in national and local government legislation, taxation, controls or regulations and/or changes in the administration or laws, policies and practices, and the impact of general business and economic conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, copper, silver and zinc), currency exchange rates (such as the Brazilian real, the Chilean peso, and the Argentine peso versus the United States dollar), the impact of inflation, possible variations in ore grade or recovery rates, changes in the Company’s hedging program, changes in accounting policies, changes in Mineral Resources and Mineral Reserves, risks related to asset disposition, risks related to metal purchase agreements, risks related to acquisitions, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, unanticipated costs and expenses, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting timelines, government regulation and the risk of government expropriation or nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, risks relating to joint venture operations, title disputes or claims, limitations on insurance coverage and timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, as well as those risk factors discussed or referred to herein and in the Company's Annual Information Form filed with the securities regulatory authorities in all provinces of Canada and available at www.sedar.com, and the Company’s Annual Report on Form 40-F filed with the United States Securities and Exchange Commission. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is presented for the purpose of assisting investors in understanding the Company’s expected financial and operational performance and results as at and for the periods ended on the dates presented in the Company’s plans and objectives and may not be appropriate for other purposes.

CAUTIONARY NOTE TO UNITED STATES INVESTORS CONCERNING ESTIMATES OF MEASURED, INDICATED AND INFERRED MINERAL RESOURCES

This news release uses the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and required to be disclosed by National Instrument 43-101. However, these terms are not defined terms under Industry Guide 7 and are not permitted to be used in reports and registration statements of United States companies filed with the Commission. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into Mineral Reserves. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a Mineral Resource is permitted disclosure under Canadian regulations. In contrast, the Commission only permits U.S. companies to report mineralization that does not constitute “Mineral Reserves” by Commission standards as in place tonnage and grade without reference to unit measures. Accordingly, information contained in this news release may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations of the Commission thereunder.

NON-GAAP FINANCIAL MEASURES AND ADDITIONAL LINE ITEMS AND SUBTOTALS IN FINANCIAL STATEMENTS

The Company has included certain non-GAAP financial measures to supplement its Consolidated Financial Statements, which are presented in accordance with IFRS, including the following:

- Cash costs per ounce of gold produced on a co-product and by-product basis;

- Cash costs per ounce of silver produced on a co-product and by-product basis;

- Co-product cash costs per pound of copper produced;

- All-in sustaining costs per ounce of gold produced on a co-product and by-product basis;

- All-in sustaining costs per ounce of silver produced on a co-product and by-product basis;

- All-in sustaining co-product costs per pound of copper produced;

- Net debt;

- Net free cash flow;

- Average realized price per ounce of gold sold;

- Average realized price per ounce of silver sold; and

- Average realized price per pound of copper sold.

The Company believes that these measures, together with measures determined in accordance with IFRS, provide investors with an improved ability to evaluate the underlying performance of the Company. Non-GAAP financial measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Management's determination of the components of non-GAAP and additional measures are evaluated on a periodic basis influenced by new items and transactions, a review of investor uses and new regulations as applicable. Any changes to the measures are duly noted and retrospectively applied as applicable.

CASH COSTS AND ALL-IN SUSTAINING COSTS

The Company discloses “cash costs” because it understands that certain investors use this information to determine the Company’s ability to generate earnings and cash flows for use in investing and other activities. The Company believes that conventional measures of performance prepared in accordance with IFRS do not fully illustrate the ability of its operating mines to generate cash flows. The measures, as determined under IFRS, are not necessarily indicative of operating profit or cash flows from operating activities. Cash costs figures are calculated in accordance with a standard developed by The Gold Institute, which was a worldwide association of suppliers of gold and gold products and included leading North American gold producers. The Gold Institute ceased operations in 2002, but the standard remains the generally accepted standard of reporting cash costs of production in North America. Adoption of the standard is voluntary and the cost measures presented herein may not be comparable to other similarly titled measures of other companies.

The measure of cash costs, along with revenue from sales, is considered to be a key indicator of a company’s ability to generate operating earnings and cash flows from its mining operations. This data is furnished to provide additional information and is a non-GAAP financial measure. The terms co-product and by-product cash costs per ounce of gold or silver produced, co-product cash costs per pound of copper produced, co-product and by-product AISC per ounce of gold or silver produced and co-product AISC per pound of copper produced do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. Non-GAAP financial measures should not be considered in isolation as a substitute for measures of performance prepared in accordance with IFRS and is not necessarily indicative of operating costs, operating profit or cash flows presented under IFRS.

By-Product and Co-Product Cash Costs

Cash costs include mine site operating costs such as mining, processing, administration, production taxes and royalties which are not based on sales or taxable income calculations, but are exclusive of amortization, reclamation, capital, development and exploration costs. The Company believes that such measure provides useful information about the Company’s underlying cash costs of operations. Cash costs are computed on a weighted average basis, net of by-product sales and on a co-product basis as follows:

Cash costs of gold and silver on a by-product basis - shown on a per ounce basis.

- The attributable cost for each metal is calculated net of by-products by applying copper and zinc net revenues, which are incidental to the production of precious metals, as a credit to gold and silver ounces produced, thereby allowing the Company’s management and stakeholders to assess net costs of precious metal production. These costs are then divided by gold and silver ounces produced.

Cash costs of gold and silver on a co-product basis - shown on a per ounce basis.

- Costs directly attributed to gold and silver will be allocated to each metal. Costs not directly attributed to each metal will be allocated based on the relative value of revenues which will be determined annually.

- The attributable cost for each metal will then be divided by the production of each metal in calculating cash costs per ounce on a co-product basis for the period.

Cash costs of copper on a co-product basis - shown on a per pound basis.

- Costs attributable to copper production are divided by commercial copper pounds produced.

By-Product and Co-Product AISC

All-in sustaining costs per ounce of gold and silver produced seeks to represent total sustaining expenditures of producing gold and silver ounces from current operations, based on co-product costs or by-product costs, including cost components of mine sustaining capital expenditures, corporate general and administrative expense excluding stock-based compensation, and exploration and evaluation expense. All-in sustaining costs do not include capital expenditures attributable to projects or mine expansions, exploration and evaluation costs attributable to growth projects, income tax payments, financing costs and dividend payments. Consequently, this measure is not representative of all of the Company's cash expenditures. In addition, the calculation of all-in sustaining costs does not include depletion, depreciation and amortization expense as it does not reflect the impact of expenditures incurred in prior periods.

All-in sustaining co-product costs reflect allocations of the aforementioned cost components on the basis that is consistent with the nature of each of the cost component to the gold, silver or copper production activities. Similarly, all-in sustaining by-product costs reflect allocations of the aforementioned cost components on the basis that is consistent with the nature of each of the cost component to the gold and silver production activities but net of by-product revenue credits from sales of copper and zinc.

A reconciliation of total cost of sales of gold, silver and copper sold (cost of sales excluding depreciation, depletion and amortization, plus depreciation, depletion and amortization) per the Consolidated Financial Statements to co-product cash costs of gold produced, co-product cash costs of silver produced, co-product cash costs of copper produced, co-product AISC of gold produced, co-product AISC of silver produced, co-product AISC of copper produced, by-product cash costs of gold produced, by-product cash costs of silver produced, by-product AISC of gold produced and by-product AISC of silver produced is provided in Section 11: of the MD&A for the three and twelve months ended December 31, 2018 and comparable period of 2017 which has been filed on SEDAR.

NET DEBT

The Company uses the financial measure "Net Debt", which is a non-GAAP financial measure, to supplement information in its Consolidated Financial Statements. The Company believes that in addition to conventional measures prepared in accordance with IFRS, the Company and certain investors and analysts use this information to evaluate the Company’s performance. The non-GAAP financial measure of net debt does not have any standardized meaning prescribed under IFRS, and therefore it may not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Net Debt is calculated as the sum of the current and non-current portions of long-term debt net of the cash and cash equivalent balance as at the balance sheet date. A reconciliation of Net Debt is provided in Section 11: of the MD&A for the three and twelve months ended December 31, 2018 and comparable period of 2017 which has been filed on SEDAR.:

NET FREE CASH FLOW

The Company uses the financial measure "Net Free Cash Flow", which is a non-GAAP financial measure, to supplement information in its Consolidated Financial Statements. Net Free Cash Flow does not have any standardized meaning prescribed under IFRS, and therefore it may not be comparable to similar measures employed by other companies. The Company believes that in addition to conventional measures prepared in accordance with IFRS, the Company and certain investors and analysts use this information to evaluate the Company’s performance with respect to its operating cash flow capacity to meet non-discretionary outflows of cash. The presentation of Net Free Cash Flow is not meant to be a substitute for the cash flow information presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. Net Free Cash Flow is calculated as cash flows from operating activities of continuing operations adjusted for advance payments received pursuant to metal purchase agreements, non-discretionary expenditures from sustaining capital expenditures and interest and financing expenses paid related to the current period. A reconciliation of Net Free Cash Flow is provided in Section 1: of the MD&A for the three and twelve months ended December 31, 2018 and comparable period of 2017 which has been filed on SEDAR.

AVERAGE REALIZED METAL PRICES

The Company uses the financial measures "average realized gold price", "average realized silver price" and "average realized copper price", which are non-GAAP financial measures, to supplement in its Consolidated Financial Statements. Average realized price does not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The Company believes that in addition to conventional measures prepared in accordance with IFRS, the Company and certain investors and analysts use this information to evaluate the Company’s performance vis-à-vis average market prices of metals for the period. The presentation of average realized metal prices is not meant to be a substitute for the revenue information presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measure.

Average realized metal price represents the sale price of the underlying metal before deducting sales taxes, treatment and refining charges, and other quotational and pricing adjustments. Average realized prices are calculated as the revenue related to each of the metals sold, i.e. gold, silver and copper, divided by the quantity of the respective units of metals sold, i.e. gold ounce, silver ounce and copper pound. Reconciliations of average realized metal prices to revenue are provided in Section 11: of the MD&A for the three and twelve months ended December 31, 2018 and comparable period of 2017 which has been filed on SEDAR.

ADDITIONAL LINE ITEMS OR SUBTOTALS IN FINANCIAL STATEMENTS

The Company uses the following additional line items and subtotals in the Consolidated Financial Statements as contemplated in IAS 1: Presentation of Financial Statements:

- Gross margin excluding depletion, depreciation and amortization — represents the amount of revenue in excess of cost of sales excluding depletion, depreciation and amortization. This additional measure represents the cash contribution from the sales of metals before all other operating expenses and DDA, in the reporting period.

- Mine operating earnings — represents the amount of revenue in excess of cost of sales excluding depletion, depreciation and amortization and depletion, depreciation and amortization.

- Operating earnings — represents the amount of earnings before net finance income/expense and income tax recovery/expense. This measure represents the amount of financial contribution, net of all expenses directly attributable to mining operations and overheads. Finance income, finance expense and foreign exchange gains/losses are not classified as expenses directly attributable to mining operations.