Yamana Gold Announces Strong Preliminary Second Quarter Operating Results With Exceptional Performance Across Its Core Asset Portfolio Delivering Production Ahead of Plan; Strategic Initiatives at Jacobina and Wasamac Continue to Advance

TORONTO, July 07, 2022 (GLOBE NEWSWIRE) -- YAMANA GOLD INC. (TSX:YRI; NYSE:AUY; LSE:AUY) (“Yamana” or “the Company”) today announces strong preliminary second quarter operating results, with total gold equivalent ounce (“GEO”)(1) production of 260,960 GEO(1). Gold production during the quarter was 232,542 ounces with silver production of 2.36 million ounces. Canadian Malartic, Jacobina, El Peñón and Cerro Moro all delivered standout quarters. All-in sustaining costs ("AISC")(2) for the quarter are expected to be less than US$1,090/oz.

The Company generated strong cash flows during the quarter, which strengthened its cash balance and financial flexibility. Cash and cash equivalents increased by more than $30 million to a total quarter-end cash balance of over $328 million from $298 million at the end of the first quarter, exclusive of approximately $215 million in cash available in MARA for utilization by the project. This represents an improvement in cash flow generation of nearly $40 million compared to the first quarter of 2022.

SECOND QUARTER 2022 PRODUCTION RESULTS

| Second Quarter 2022 Preliminary Production | |

| GEO(1) Production | 260,960 |

| Gold Production (oz.) | 232,542 |

| Silver Production (oz.) | 2,356,853 |

Operational Update

- Year to date operating results comfortably position the Company to achieve both its annual production and cost guidance. The strong year to date gold equivalent production has exceeded budget despite the gold to silver ratio being near an all-time high and significantly above the Company’s budget assumption for that ratio.

- Canadian Malartic produced 87,186 ounces of gold (50% basis) during the second quarter, ahead of plan. Permitting at the Odyssey project remains on schedule while construction is on track and on budget with first production from Odyssey South expected in the first quarter of 2023.

- Jacobina had an exceptional second quarter and delivered record quarterly production of 49,662 ounces of gold. Underground mine development work is in line with the mine plan at 1,500 metres per month to gain access to new mining panels. Together with the higher ore tonnes mined, the mine development provides additional flexibility through the build-up of ore stockpiles supporting the higher throughput of the Phase 2 expansion. Production for 2022 is expected to increase for the ninth consecutive year, a trend that is expected to continue in the coming years, as a result of the phased expansion strategy and the exploration programs aimed at generating significant value from the remarkable geological upside of the property.

- El Peñón produced 54,068 GEO(1), comprised of 46,627 ounces of gold and 619,981 ounces of silver during the quarter, with June production of 19,077 GEO(1) benefitting from access to the Chiquilla Chica zone which entered into production at the beginning of the month. Optimized mining sequencing, bringing forward zones with a higher gold to silver ratio in the first half of the year, has put El Peñón in an excellent position to achieve full year GEO(1) production guidance.

- Minera Florida produced 18,138 ounces of gold during the quarter and remains on track to meet annual production guidance.

- Cerro Moro delivered exceptional results, producing 51,906 GEO(1) comprised of 30,929 ounces of gold and 1,736,872 ounces of silver. Production at the mine continues to benefit from the opening of more mining faces and the resultant increase in mill feed coming from higher-grade underground ore, as well as improved recoveries. Production for the first half of 2022 marks the highest half-yearly production since 2019.

| Mine-by-Mine | Second Quarter 2022 Preliminary Production | |

| Gold (oz.) | ||

| El Peñón | 46,627 | |

| Canadian Malartic (50%) | 87,186 | |

| Jacobina | 49,662 | |

| Cerro Moro | 30,929 | |

| Minera Florida | 18,138 | |

| Total Yamana | 232,542 | |

| Silver (oz.) | ||

| El Peñón | 619,981 | |

| Cerro Moro | 1,736,872 | |

| Total Yamana | 2,356,853 | |

| GEO(1) Production | 260,960 | |

Jacobina Phase 2 Commissioning and Phased Expansion Update

The Phase 2 expansion at Jacobina continued to successfully ramp-up during the quarter, with the mine achieving a sustained throughput rate of over 8,400 tpd in June. Yamana expects the throughput objective of 8,500 tpd to be achieved in July, establishing Jacobina’s sustainable production profile at 230,000 ounces of gold per year.

The Company’s phased expansion strategy at Jacobina is well advanced and the Company anticipates that the low-cost operation will have a strategic mine life exceeding at least two decades, taking mineral reserves and high-conviction mineral resources into consideration. With the Phase 2 expansion delivered ahead of schedule, the Company is now pursuing the Phase 3 expansion to 10,000 tpd through continued incremental debottlenecking. With the permit to expand to 10,000 tpd already in hand, Phase 3 is expected to increase gold production to approximately 270,000 ounces per year by 2025 with a modest incremental capital expenditure of $20 million to $30 million.

A comprehensive plan for the Phase 4 expansion, which envisages throughput of up to 15,000 tpd and gold production in excess of 350,000 ounces per year, is also well underway as is the evaluation of further strategic options related to Jacobina and the significant exploration potential that is present along the prolific Jacobina Greenstone Belt, which hosts the mine. Jacobina is a complex of underground mines with a common plant and now, in addition to local exploration, from which the Company has been successful at new discoveries and developing newer mines in the complex, the Company is advancing a broader regional exploration effort initially north of the current mine complex although more broadly across a more than 110 kilometre greenstone belt north of Jacobina with comparable geology.

Board Approved Wasamac Bulk Sample Program

The Company continues to advance preparations for its board-approved bulk sample program at its wholly-owned Wasamac project in the Abitibi-Témiscamingue Region of Québec, Canada. The initiative would allow construction to commence on the ramp, enabling earlier access to the deposit to increase the level of confidence in metallurgical and geotechnical variables and optimize the processing flow sheet and mining sequence. Construction of surface facilities to support the ramp development activity and associated environmental requirements would also be advanced.

With a high level of continuity and regular geometry, combined with a relatively simple structural setting and average mineralized widths of 13 metres, Wasamac is well positioned for high-production and low-cost underground mining methods given the project’s low level of geological risk and favourable geological environment. Infill drilling results since mid-2021 confirm or exceed expected grades and widths. Similarly, the metallurgical and geomechanical assumptions used in the feasibility study are based on rigorous lab testing from drill hole samples. Bulk sampling and industrial-scale tests will build on these results, enabling development of production-ready models for the grade, recovery, and geotechnical aspects of the project, to support the first three years of production.

Additionally, the bulk sample program will allow the Company to capture opportunities to optimize the processing performance by testing multiple flowsheet options and confirm stope stability parameters to optimize stope dimensions, backfilling strategy and mining sequence while contributing to ensuring a safe working environment. The accelerated development of the ramp will also establish drilling platforms to perform both delineation and exploration drilling at Wasamac main zones, Wildcat and potential new zones from underground.

Preparation of the documentation for the bulk sample permits is underway and scheduled for submission in the third quarter of 2022, with the approval process expected to take less than 6 months. Permit approvals are expected in early 2023 and ramp development could begin in spring 2023. While the permit application is in progress, select site works, including construction of an access road, a temporary 25 kV power line and temporary buildings is scheduled to commence in the second half of 2022.

The bulk sample will not require additional costs above what was included in the feasibility study, rather a fraction of the costs will be brought forward in time slightly. A modest capital expenditure of approximately $7 million is planned for the second half of 2022, in preparation for development to commence in the first half of 2023.

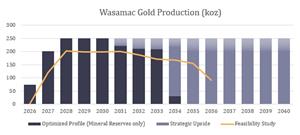

Wasamac Strategic Life-of-Mine (LOM) Plan Highlighting Potential Upside Optionality

During the second quarter, the Company completed an update of the Wasamac strategic LOM plan, building on the 2021 feasibility study and incorporating the results of several value-adding studies that were advanced throughout the first half of 2022. The strategic plan demonstrates an improved gold production profile compared to the feasibility study, while continuing to establish Wasamac as a modern, low-cost, responsible underground mine.

Extension of the processing plant site through land acquisition and additional geotechnical drilling have allowed optimization of the underground mine design and processing plant layout. The revised layout avoids environmentally sensitive areas, improves the plant configuration, and provides additional space for ore stockpiling, while continuing to minimize impacts to the surrounding property holders. Using the revised mine designs, the mining sequence has been optimized to increase feed grades in the first two years, resulting in a faster production ramp-up to 200,000 ounces in 2027 and up to 250,000 ounces in 2028.

Furthermore, the ongoing mine design and sequence optimizations could position the Wasamac mine with the option for a future incremental expansion from 7,000 tpd to 9,000 tpd in year 3 of operations, to extend the gold production profile of 250,000 ounces per year until at least 2030. The results of a comminution trade-off study indicate that the higher throughput of 9,000 tpd could be achieved with limited additional mechanical equipment at modest capital expenditures and without increasing the area of the plant layout.

The strategy to start production at 7,000 tpd, with a later incremental expansion to 9,000 tpd, balances the mining equipment fleet and workforce requirements while minimizing any impact to the ongoing permitting process. As a result, the Company continues to expect to receive the required permits to commence project construction in mid-2024 and the initial capital cost estimate from the feasibility study of $416 million also remains unchanged.

Positive infill and exploration drilling results to date indicate the potential for a strategic mine life of 10 to 15 years at 200,000 to 250,000 ounces of gold per year, compared to the LOM average of 169,000 ounces in the feasibility study. The Wasamac deposit is not only open at depth and along strike but the underexplored secondary zones such as Wildcat are showing promising drilling results. Additional exploration targets on the property, including the adjacent Francoeur, Arntfield, and Lac Fortune properties, provide further upside.

Figure 1: Optimized Strategic Production Profile

https://www.globenewswire.com/NewsRoom/AttachmentNg/f55a81fa-92dc-4171-9927-7a7a749198af

As a result of the improved production profile in the updated strategic LOM plan, unit costs are expected to be lower than the feasibility study LOM average of $828 per ounce and, at the feasibility study gold price of US$1,550, the net present value would approximately double assuming the strategic mine life is extended through 2036 at 9,000 tpd.

Other opportunities that continue to be evaluated but are not yet included in the strategic plan include the processing flow sheet optimization to increase metallurgical recoveries by approximately 3% (for which metallurgical testing is ongoing), optimized configuration of the tailings filter plant and paste backfill plant, and increased levels of electrification, automation and renewable energy usage in the project.

Wasamac further increases the Company’s footprint within the prolific Abitibi-Témiscamingue region. Together with the Odyssey project at Canadian Malartic, the optimized strategic plan increases the attributable sustainable strategic gold production platform to 500,000 – 550,000 ounces, with considerable upside. Assuming a gold price of US$1,550 per ounce, both the Wasamac and Odyssey projects are fully funded with no external capital required and put the Company on a path towards being a regionally dominant producer with two generational, cornerstone mines within the Abitibi-Témiscamingue region.

The Company intends to provide an exploration update alongside its full Q2 2022 operational and financial results on Thursday, July 28, 2022 to highlight the ongoing positive exploration results of its assets in Québec that underpin the strategic outlook and support meaningfully extending the sustainable production platform.

Qualified Persons

Scientific and technical information contained in this news release has been reviewed and approved by Sébastien Bernier (P. Geo and Senior Director, Reserves and Resources). Sébastien Bernier is an employee of Yamana Gold Inc. and a "Qualified Person" as defined by Canadian Securities Administrators' National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

About Yamana

Yamana Gold Inc. is a Canadian-based precious metals producer with significant gold and silver production, development stage properties, exploration properties, and land positions throughout the Americas, including Canada, Brazil, Chile and Argentina. Yamana plans to continue to build on this base through expansion and optimization initiatives at existing operating mines, development of new mines, the advancement of its exploration properties and, at times, by targeting other consolidation opportunities with a primary focus in the Americas.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Investor Relations

416-815-0220

1-888-809-0925

Email: investor@yamana.com

FTI Consulting (UK Public Relations)

Sara Powell / Ben Brewerton

+44 7974 201 715223 / +44 203 727 1000

END NOTES

| (1) | GEO is calculated as the sum of gold ounces and the gold equivalent of silver ounces using a ratio of 82.93 for the three months ended June 30, 2022 and 85.33 for the one month ended June 30, 2022. GEO calculations for actuals are based on an average market gold to silver price ratio for the relevant period. Guidance and forward-looking GEO assumes gold ounces plus the equivalent of silver ounces using a ratio of 72.00:1. | |

| (2) | A cautionary note regarding non-GAAP performance measures and their respective reconciliations, as well as additional line items or subtotals in financial statements is included in Section 11: Non-GAAP Performance Measures and Additional Subtotals in Financial Statements in the Company's MD&A for the three months ended March 31, 2022 and in the 'Non-GAAP Performance Measures' of the associated press release dated April 27, 2022. |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This news release contains or incorporates by reference “forward-looking statements” and “forward-looking information” under applicable Canadian securities legislation and within the meaning of the United States Private Securities Litigation Reform Act of 1995. Forward-looking information includes, but is not limited to information with respect to the Company’s strategy, plans, expectations, beliefs, including future financial or operating performance, expected timing for permitting and construction of the Odyssey project, expectations relating to the phased expansion at Jacobina and timing thereof, Wasamac project construction and development plans and timing thereof and the Company’s expected second quarter production and full year guidance. Forward-looking statements are characterized by words such as “plan", “expect”, “budget”, “target”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the Company’s expectations in connection with the production and exploration, development and expansion plans at the Company's projects discussed herein being met, the impact of proposed optimizations at the Company's projects, changes in national and local government legislation, taxation, controls or regulations and/or change in the administration of laws, policies and practices, and the impact of general business and economic conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, silver, copper and zinc), currency exchange rates (such as the Canadian Dollar, the Brazilian Real, the Chilean Peso and the Argentine Peso versus the United States Dollar), the impact of inflation, possible variations in ore grade or recovery rates, changes in the Company’s hedging program, changes in accounting policies, changes in mineral resources and mineral reserves, risks related to asset dispositions, risks related to metal purchase agreements, risks related to acquisitions, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, risks associated with infectious diseases, including COVID-19, unanticipated costs and expenses, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting timelines, government regulation and the risk of government expropriation or nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, risks relating to joint venture operations, title disputes or claims, limitations on insurance coverage, timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, as well as those risk factors discussed or referred to herein and in the Company's Annual Information Form filed with the securities regulatory authorities in all provinces of Canada and available at www.sedar.com, and the Company’s Annual Report on Form 40-F filed with the United States Securities and Exchange Commission. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is presented for the purpose of assisting investors in understanding the Company’s expected financial and operational performance and results as at and for the periods ended on the dates presented in the Company’s plans and objectives and may not be appropriate for other purposes.

![]()

Figure 1