Yamana Gold Provides 2021-2023 Guidance and Ten-Year Overview

TORONTO, Jan. 25, 2021 (GLOBE NEWSWIRE) -- YAMANA GOLD INC. (TSX:YRI; NYSE:AUY; LSE:AUY) (“Yamana” or the “Company”) herein provides 2021, 2022, and 2023 production guidance, 2021 cost guidance, and its 10-year production overview.

The following table presents the Company's total gold, silver and gold equivalent ounces ("GEO") production expectations in 2021, 2022 and 2023. The Company notes that it guides on GEO production and costs based on a particular assumption of gold and silver prices. Although underlying gold and silver production does not change with the fluctuation in gold and silver prices, the change in the GEO ratio from such fluctuations may result in a different GEO production than that guided.

The Company looks at production within a normal range of +/- 3%, and the guidance values noted below reflect the mid-point of this production range for the 2021-2023 period.

The production profile for 2021 to 2023 shows sequential growth in gold production. Several growth opportunities are available, and in the near and medium-term the Company remains focused on optimizing the existing portfolio of five operating mines while also advancing studies for various expansion projects and longer term development assets.

The Company expects to continue its established trend of delivering stronger production in the second half of the year, with approximately 53% of production slated for the second half, along with quarterly sequential increases in production.

| (000's ounces) | 2020 Actual | 2021 Guidance | 2022 Guidance | 2023 Guidance |

| Total gold production (i) | 780 | 862 | 870 | 889 |

| Total silver production | 10,366 | 10,000 | 9,360 | 8,000 |

| Total GEO production (i) | 901 | 1,000 | 1,000 | 1,000 |

(i) GEO assumes gold ounces plus the equivalent of silver ounces using a ratio of 72:1 for 2021, 2022 and 2023. Included in full year 2020 production figures are 18,929 gold ounces of pre-commercial production, related to the Company's 50% interest in the Canadian Malartic mine's Barnat deposit. Pre-commercial production ounces are excluded from sales figures, although pre-commercial production ounces that were sold during their respective period of production had the corresponding revenues and cost of sales capitalized to mineral properties.

The following table presents mine-by-mine production results for Yamana Mines for 2020 and expectations for 2021.

| (000's ounces) | Gold | Silver | GEO | |||

| 2020 Actual (ii) | 2021 Guidance | 2020 Actual | 2021 Guidance | 2020 Actual | 2021 Guidance | |

| Canadian Malartic (50%) (i) | 284 | 350 | - | - | 284 | 350 |

| Jacobina | 178 | 175 | - | - | 178 | 175 |

| Cerro Moro | 67 | 90 | 5,449 | 5,500 | 132 | 166 |

| El Peñón | 161 | 160 | 4,917 | 4,500 | 217 | 222 |

| Minera Florida | 90 | 87 | - | - | 90 | 87 |

| Yamana Mines | 780 | 862 | 10,366 | 10,000 | 901 | 1,000 |

(ii) Included in full year 2020 production figures are 18,929 gold ounces of pre-commercial production, related to the Company's 50% interest in the Canadian Malartic mine's Barnat deposit. Pre-commercial production ounces are excluded from sales figures, although pre-commercial production ounces that were sold during their respective period of production had the corresponding revenues and cost of sales capitalized to mineral properties.

Cost Outlook

The Company anticipates that it will continue to incur some costs in relation to COVID-19 in the near future. Current expectation of pandemic related costs is that those costs will continue to be incurred during the first half of the year and begin to decrease in the second half of the year with a rollout of vaccinations expected in most countries in which the Company operates. With increasing numbers of the population receiving the vaccine, the Company would expect to see increasing immunity and decreasing caseloads, allowing for gradual easing of our COVID-related controls and associated costs toward the second half of 2021 as noted. Total costs are not expected to exceed approximately $20 million for the year. Similarly to 2020, COVID-19 costs are disclosed as part of mine operating earnings as temporary suspension, standby and other incremental COVID-19 costs and are excluded from cash costs and all-in sustaining costs (“AISC”).

The expected decline in COVID-19 costs throughout the upcoming year also corresponds to the Company’s customary lower second half of the year costs, associated with higher production levels.

The following table presents guidance ranges for 2021.

| (In US dollars) | Cash costs per GEO sold (iii) 2021 Guidance | AISC per GEO sold (iii) (iv) 2021 Guidance |

| Canadian Malartic (50%) (i) | 635 - 675 | 850 - 885 |

| Jacobina | 565 - 600 | 735 – 765 |

| Cerro Moro | 790 - 835 | 1,175 – 1,225 |

| El Peñón | 620 - 660 | 835 - 870 |

| Minera Florida | 740 - 785 | 1,065 – 1,105 |

| Yamana Mines | 655 - 695 | 980 – 1,020 |

(iii) A cautionary note regarding non-GAAP financial measures and additional subtotals in financial statements are included in Section 12: Non-GAAP Performance Measures of this MD&A. Total cost of sales per GEO sold will be provided in conjunction with the Company’s annual results.

(iv) Mine site AISC includes cash costs, mine site general and administrative expense, sustaining capital, capitalized exploration and expensed exploration. Consolidated AISC incorporates additional non-mine site costs including corporate general and administrative expense.

The following table presents expansionary capital, sustaining capital and exploration spend expectations by mine for 2021:

| (In millions of US Dollars) | Expansionary capital 2021 Guidance | Sustaining capital 2021 Guidance | Total exploration 2021 Guidance | |||

| Canadian Malartic (50%) | $ | 17.0 | $ | 73.0 | $ | 15.0 |

| Jacobina | 29.0 | 19.0 | 12.0 | |||

| Cerro Moro | 1.0 | 40.0 | 18.0 | |||

| El Peñón | 1.0 | 31.0 | 18.0 | |||

| Minera Florida | 17.0 | 19.0 | 11.0 | |||

| Other capital | 1.0 | 1.0 | - | |||

| MARA (i) | 15.0 | - | - | |||

| Wasamac | 5.0 | - | 11.0 | |||

| Generative exploration | - | - | 18.0 | |||

| Other exploration and overhead | - | - | 7.0 | |||

| Total | $ | 86.0 | $ | 183.0 | $ | 110.0 |

(i) Related to Yamana’s ownership in MARA of 56.25%

Approximately 70% of the Company’s expected exploration spend is capital in nature.

Capital expenditure values for 2021 do not include the cost to add to long-term ore stockpile balances at Canadian Malartic. These costs are estimated at $15.0 million for 2021 compared to $5.9 million for 2020, both on a 50% basis.

The following table presents other expenditure expectations for 2021:

| (In millions of US Dollars) | 2021 Guidance | |

| Total DDA | $ | 470.0 – 500.0 |

| Cash based G&A | $ | 72.0 |

| Cash income taxes paid (i) | $ | 180.0 –200.0 |

(i) 2021 guidance for cash taxes paid is based on metal prices per the guidance assumption table. Further, cash taxes paid consider payments made in relation to prior years, as in certain jurisdictions, payments and true-ups related to a fiscal year’s taxes are settled in the next fiscal year.

Guidance Assumptions

Key assumptions, in relation to the above guidance, are presented in the table below.

2021 Sensitivity Impact

| 2020 Actual (i) | 2021 Guidance | Change | AISC/GEO | EBITDA ($Ms) | Change in Cash ($Ms) | |||||

| GEO Ratio | 88.86 | 72.00 | ||||||||

| Gold | $ | 1,770 | $ | 1,800 | $50 | $5 | 41.0 | 34.0 | ||

| Silver | $ | 20.51 | $ | 25.00 | $1.00 | ($6 | ) | 10.0 | 8.0 | |

| USD-CAD | 1.34 | 1.28 | 5% | ($6 | ) | 2.0 | 7.0 | |||

| USD-BRL | 5.16 | 5.25 | 5% | ($2 | ) | 1.0 | 3.0 | |||

| USD-ARS | 70.65 | 108.00 | 5% | ($2 | ) | 1.0 | 2.0 | |||

| USD-CLP | 792 | 725 | 5% | ($4 | ) | 3.0 | 4.0 | |||

(i) Actual metal prices and exchange rates shown in the table above are the average metal prices and exchange rates for the year ended December 31, 2020.

The Company may enter into forward contracts or other risk management strategies, from time to time, to hedge against the risk of an increase in the value of foreign currencies in the jurisdictions in which the Company operates. Please refer to the Foreign Exchange Hedging Section of this release for further details.

MINE BY MINE NEAR-TERM OUTLOOK

Canadian Malartic (50%)

Canadian Malartic exceeded its revised 2020 guidance, producing 284,000 ounces of gold. Production last year was impacted by COVID-19 related restrictions on mining in Quebec and is forecast to increase in 2021 to 350,000 ounces, with AISC projected to decline to $850-$885 per ounce from $945 per ounce in 2020. Mining is transitioning from the Canadian Malartic pit to the Barnat pit, which is now in commercial production, and 70% of the total tonnes mined in 2021 are expected to come from Barnat. The Canadian Malartic pit will be depleted in the first half of 2023, and waste rock and tailings will be deposited into the pit beginning in 2023.

The operation continues to advance the underground project, which consists of the East Gouldie, Odyssey, and East Malartic zones, (collectively known as the Odyssey project). Key development milestones over the next three years include the development of a ramp into the Odyssey, East Malartic, and East Gouldie zones, which will allow for tighter definition drilling to further expand the mineral resource base, along with headframe construction and shaft sinking. First production from Odyssey is expected in 2023. These milestones are included in the production and cost outlooks provided above. A preliminary economic assessment for the project is expected to be completed in February 2021.

Jacobina

The Jacobina mine continues to be a standout performer, consistently exceeding expectations. Production in 2021 is forecast to be in a similar range to the all-time high recorded in 2020 at low AISC of $735-$765 per ounce. The operation exceeded the targeted throughput rate of 6,500 tonnes per day (“tpd”) for the Phase 1 expansion, and it continues to identify and implement additional processing plant optimizations to further increase throughput, improve recoveries, and reduce costs. Beyond further optimizations, the Feasibility Study for Jacobina’s Phase 2 expansion plans to increase throughput to 8,500 tpd and raise annual production to 230,000 ounces remains on track for mid-2021.

In a separate initiative, Jacobina is evaluating the installation of a backfill plant that would allow up to 2,000 tpd of tailings to be deposited in underground voids. In addition to reducing the mine’s environmental footprint, a backfill plant would extend the life of the mine’s existing tailings storage facility and improve mining recovery, resulting in increased conversion of mineral resources to mineral reserves.

El Peñón

Overall GEO production in 2021 is forecast to be in line with production in 2020, but improvements to cost structure are expected to be realized in 2021, with cash costs expected to range between $620-$660 per GEO and AISC(1) forecast at between $835-$870 per GEO. The mine’s current production rate—the result of the right-sizing of the operation initiated in late 2016—increased cash flow while ensuring the long-term sustainability of the mine. Exploration successes over the last two years has resulted in an increase in mineral reserves, unlocking opportunities to incrementally increase production by leveraging excess processing capacity at El Peñón. The operation can process approximately 4,200 tpd, which represents upside of 20-30% above currently budgeted levels, with no additional capital expenditures required.

1. Refers to a non-GAAP financial measure.

Minera Florida

Minera Florida exceeded its full year production guidance, posting its highest production level since 2010 and the second highest since entering production in 1986.(1) Gold production is forecast to be at a similar level in 2021. The strategy at Minera Florida is to extend mine life and unlock opportunities for increased annual gold production following an approach similar to the approach taken at Jacobina. This includes focusing on mineral reserve development and generating an inventory of prepared mining areas to increase operational flexibility. The short-term focus is to achieve consistent throughput of 74,500 tonnes per month (“tpm”) from the underground mine while continuing improvements in the mine that will increase feed grade to align with mineral reserve grade and set the stage for further expansions.

1. Excluding gold production from the reclamation of historic tailings.

Cerro Moro

Production and costs in 2020 at Cerro Moro were significantly impacted by COVID-19 related restrictions on travel and work rosters. The mine and processing plant are currently running at full capacity, though COVID-19 continues to present a risk of further disruptions, particularly during the first half of the year. Exploration drilling and underground capital development were also delayed by COVID-19 in 2020. Hence, Cerro Moro is planning higher production in 2021, but will ramp-up gradually throughout the year as it mines new underground levels. Exploration drilling continues in the core mine area at Cerro Moro with positive results and opportunities to convert mineral resources into mineral reserves and generate new high-grade discoveries. The operation is evaluating construction of a heap leach operation, a lower-cost processing alternative that would allow for the processing of lower-grade mineral reserves, potentially extending mine life. The evaluation is in the early stages with a preliminary study completed and metallurgical lab testing currently underway.

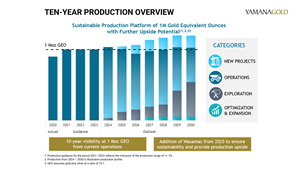

TEN-YEAR PRODUCTION OVERVIEW

A graphic accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/4e5ea3bd-e322-4966-b94e-7c8baf50adfa

1. Production guidance for the period 2021 – 2023 reflects the mid-point of the production range of +/- 3%.

2. Production from 2024 – 2030 is illustrative production profile.

3. GEO assumes gold plus silver at a ratio of 72:1.

Base Case

Yamana has a strong 10-year base case outlook with a sustainable production platform of 1 million GEO per year through 2030. Production will be underpinned by continued operational success at the Company’s existing operations, which have consistently replaced mineral reserves above depletion.

Robust exploration results are expected to drive incremental production growth at Minera Florida, which has a low-cost opportunity to increase capacity at its existing processing plant. The long-term strategy at Minera Florida is to increase monthly throughput from 74,500 tpm to 100,000 tpm with a corresponding production increase of up to 120,000 ounces of gold per year at AISC below $1,000 per ounce.

At El Peñón, which recently completed its twenty-first year of production, the Company has a high degree of confidence that it will continue to replace mineral reserves through new discoveries and infill drilling on several major veins, thereby maintaining mine life visibility for at least another 10 years. The operation is targeting annual production of 260,000 GEO at AISC below $900 per GEO, with the production increase to be supported by the mine’s existing processing capacity of up to 4,200 tpd and no additional capital spending required.

The base case assumes continuing exploration success at Cerro Moro, which will support a mine life extension. The Company is investing in exploration drilling on its large mine property and surrounding area, which together exceed 300,000 hectares, with efforts currently focusing on both the core mine area and new mineralized zones close to existing mineral reserves. Further upside is available from significant mineralization that has been identified at below current mineral reserve cut-off grades that could potentially be mined economically using lower-cost heap leach processing that would occur in parallel with the existing processing plant.

The base case also includes the Canadian Malartic underground project, which represents the next evolution for Canada’s largest gold mine. First production is expected in 2023 from the Odyssey South zone with the Upper East Gouldie zone expected to come online in 2027. The most recent underground mineral resource for the project, which was published in February 2020, showed more than 10 million ounces of gold (100% basis), including 9,596,000 ounces of inferred mineral resources (100% basis) and 830,000 ounces of indicated mineral resources (100% basis). In the interim, exploration results have been exceptional, improving economics and increasing confidence that the underground project will be a multi-hundred thousand ounce annual producer for decades. The Company will provide an updated mineral resource and further details on the development for the underground project when it reports its fourth quarter and full year results on February 11, 2021.

The base case scenario also includes the Jacobina Phase 2 expansion, which will increase throughput to 8,500 tpd and raise annual production to 230,000 ounces, a 28% increase from current levels. In addition, the Company plans to implement a Phase 3 expansion at Jacobina which, for a modest cost, would increase throughput to 10,000 tpd without the need for additional grinding capacity and raise annual production to 270,000 ounces by approximately 2027.

The Company is well-positioned to fund all exploration, expansions, projects and opportunities identified in its guidance and decade-long outlook using available cash and cash flow from operations. Based on current forecasts, annual expansionary capital expenditures are expected to be in the range of $100 million and $125 million, on average, over the next four years, the result of which is that the Company will be well-positioned to manage all its capital allocation priorities, objectives and plans, including payment and increases in dividends. The Company forecasts that it should be able to sustain its dividend at the current rate even if the price of gold were to decline to significantly lower levels, and should be able to support and increase its dividend at the current price of gold as its cash balances increase. The Company notes that in addition to its cash balances and cash flows, it also has interests in securities, instruments and assets that can and, over time, will likely be monetized, which will further increase cash balances for redeployment to the Company’s capital allocation priorities, objectives and plans.

Upside Case

The Company’s upside case is for annual production to trend above 1 million GEO by mid-decade, reaching 1.2 million GEO by approximately 2028. The upside case is underpinned primarily by the newly acquired Wasamac project—a future underground mine located in Quebec’s Abitibi region just 100 kilometres away from Canadian Malartic. The project, which is expected to enter production in 2025, currently has a mineral reserve base of 1.8 million ounces of gold. Based on the 2018 Feasibility Study conducted by Wasamac’s previous owner, Monarch Gold, production is projected at 160,000 ounces of gold per year at a low AISC of $635 per ounce. Yamana believes there is considerable upside for future exploration success and mineral resource conversion, with the deposit remaining open at depth and along strike. The Company will target increasing the mineral inventory and perform optimizations to enhance the project’s value, advance engineering, and de-risk execution, leveraging the Company’s technical expertise and adhering to its disciplined capital approach.

Additional Long-Term Upside

The Company has a number of compelling development and exploration stage projects in its pipeline with the potential to drive significant long-term production upside towards the end of the current decade and beyond. These include the MARA project, one of the largest copper-gold projects in the world; the Suyai Project, a large gold project in Chubut Province, Argentina, that is projected to reach production of up to 250,000 ounces annually in its first eight years; and a number of advanced exploration projects in the Company’s generative exploration program, including Lavra Velha, Monument Bay, Jacobina Norte, and Borborema. Assuming just two of these projects, MARA and Suyai, are constructed within the next 10 years, annual production would almost double.

FOREIGN EXCHANGE HEDGING

As at December 31, 2020, the Company had zero-cost collar contracts, which allow the Company to participate in exchange rate movements between two strikes, as follows:

| Average call price (i) | Average put strike price (i) | Total (ii) | |

| Brazilian Real to USD | |||

| January 2021 to June 2021 | R$3.85 | R$4.31 | R$ 93.0 million |

(i) R$ = Brazilian Reais

(ii) Evenly split by month.

In addition, as at December 31, 2020, the Company had forward contracts as follows:

| Average forward price (i) | Total (ii) | |

| Brazilian Real to USD | ||

| January 2021 to June 2021 | R$4.07 | R$ 93.0 million |

(i) R$ = Brazilian Reais

(ii) Evenly split by month.

Subsequent to December 31, 2020, the Company entered into new zero-cost collar contracts, which allow the Company to participate in exchange rate movements between two strikes, as follows:

| Average call price (i) | Average put strike price (i) | Total (ii) | |

| Brazilian Real to USD | |||

| July 2021 to December 2022 | R$5.25 | R$5.71 | R$ 288.0 million |

(i) R$ = Brazilian Reais

(ii) Evenly split by month.

Additionally, the Company entered into new forward contracts as follows:

| Average forward price (i) | Total (ii) | |

| Brazilian Real to USD | ||

| July 2021 to December 2022 | R$5.49 | R$ 288.0 million |

| Chilean Peso to USD | ||

| February 2021 to December 2021 | CLP 736.80 | CLP 102.3 billion |

| Canadian Dollar to USD | ||

| February 2021 to December 2021 | C$1.27 | C$220.0 million |

(i) R$ = Brazilian Reais, CLP = Chilean Pesos, C$ = Canadian Dollars

(ii) Evenly split by month.

CORPORATE UPDATE CALL AND WEBCAST

The Company will provide a corporate update webcast on Tuesday, January 26, 2021, from 10:00 am-12:00 pm ET (3:00-5:00 pm GMT) during which it will expand on its guidance and decade-long outlook, share its strategic priorities, and provide an operational update. The event will be accessible via conference call or webcast with further details below. Analysts and investors who intend to attend or who may not be able to attend the webcast are advised that a detailed presentation which will be relied upon for the webcast is available and can be accessed on the Company’s website at www.yamana.com.

| Details of Corporate Update Conference Call: | |

| Toll Free (North America): | 1-800-898-3989 |

| Toronto Local and International: | 416-406-0743 |

| Toll Free (UK) Passcode: Webcast: | 00-80042228835 7015536# www.yamana.com |

| Conference Call Replay | |

| Toll Free (North America): | 1-800-408-3053 |

| Toronto Local and International: | 905-694-9451 |

| Toll Free (UK) Passcode: | 00-80033663052 4698827# |

The conference call replay will be available from January 26, 2021, until 11:59 p.m. ET (5:00 am GMT) on February 26, 2021.

About Yamana

Yamana Gold Inc. is a Canadian-based precious metals producer with significant gold and silver production, development stage properties, exploration properties, and land positions throughout the Americas, including Canada, Brazil, Chile and Argentina. Yamana plans to continue to build on this base through expansion and optimization initiatives at existing operating mines, development of new mines, the advancement of its exploration properties and, at times, by targeting other consolidation opportunities with a primary focus in the Americas.

FOR FURTHER INFORMATION PLEASE CONTACT:

Investor Relations

416-815-0220

1-888-809-0925

Email: investor@yamana.com

FTI Consulting (UK Public Relations)

Sara Powell / Ben Brewerton

+44 203 727 1000

Email: Yamana.gold@fticonsulting.com

Credit Suisse (Joint UK Corporate Broker)

Ben Lawrence / David Nangle

Telephone: +44 (0) 20 7888 8888

Joh. Berenberg Gossler & Co. KG (Joint UK Corporate Broker)

Matthew Armitt / Jennifer Wyllie / Detlir Elezi

Telephone: +44 (0) 20 3207 7800

Peel Hunt LLP (Joint UK Corporate Broker)

Ross Allister / David McKeown / Alexander Allen

Telephone: +44 (0) 20 7418 8900

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This news release contains or incorporates by reference “forward-looking statements” and “forward-looking information” under applicable Canadian securities legislation and within the meaning of the United States Private Securities Litigation Reform Act of 1995. Forward-looking information includes, but is not limited to information with respect to the Company’s strategy, plans or future financial or operating performance, changes to its dividend policy and dividend reporting, the implementation of a cash reserve fund in order to sustain dividend level independent of gold prices, the Company’s expectation that it will continue to generate cash flow and execute on monetization initiatives, some of which will support the cash reserve fund, or updates regarding mineral reserves and mineral resources. Forward-looking statements are characterized by words such as “plan", “expect”, “budget”, “target”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include unforeseen impacts on cash flow, monetization initiatives, and available residual cash, an inability to maintain a cash reserve fund balance that can support current or future dividend increases, the outcome of various planned technical studies, production and exploration, development, optimizations and expansion plans at the Company's projects, changes in national and local government legislation, taxation, controls or regulations and/or change in the administration of laws, policies and practices, and the impact of general business and economic conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, silver and zinc), currency exchange rates (such as the Brazilian Real, the Chilean Peso and the Argentine Peso versus the United States Dollar), the impact of inflation, possible variations in ore grade or recovery rates, changes in the Company’s hedging program, changes in accounting policies, changes in mineral resources and mineral reserves, risks related to asset dispositions, risks related to metal purchase agreements, risks related to acquisitions, changes in project parameters as plans continue to be refined, changes in project development, unanticipated costs and expenses, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting timelines, government regulation and the risk of government expropriation or nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, risks relating to joint venture or jointly owned operations, title disputes or claims, limitations on insurance coverage, timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, as well as those risk factors discussed or referred to herein and in the Company's Annual Information Form filed with the securities regulatory authorities in all provinces of Canada and available at www.sedar.com, and the Company’s Annual Report on Form 40-F filed with the United States Securities and Exchange Commission. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is presented for the purpose of assisting investors in understanding the Company’s expected financial and operational performance and results as at and for the periods ended on the dates presented in the Company’s plans and objectives and may not be appropriate for other purposes.

![]()

TEN-YEAR PRODUCTION OVERVIEW