Yamana Gold Reports Strong Fourth Quarter and Full Year 2020 Results; Impressive Technical Study Results Delivered for the Odyssey Underground Project at Canadian Malartic With Construction Decision Approved; Adopts Climate Change Strategy

TORONTO, Feb. 11, 2021 (GLOBE NEWSWIRE) -- YAMANA GOLD INC. (TSX:YRI; NYSE:AUY; LSE:AUY) (“Yamana” or “the Company”) is herein reporting its financial and operational results for the fourth quarter and full year 2020, providing three-year mine-by-mine guidance, and updating mineral reserve and mineral resource estimates as at December 31, 2020.

The Company is also announcing a positive construction decision for the Odyssey underground project at the Canadian Malartic mine following the impressive results of the technical study, which outlines robust economics, a significant increase in mineral resources, and a mine life extension to at least 2039.

Further, as a continuation of Yamana’s climate change actions, the Company today is also announcing that it has formally adopted a climate strategy, approved by the Board of Directors, to demonstrate the Company’s commitment to the transition to a low-carbon future. The strategy is underpinned by adoption of two targets: a 2° C science-based target (“SBT”) and an aspirational net-zero 2050 target.

FOURTH QUARTER AND FULL YEAR HIGHLIGHTS

Financial Results - Strong Earnings and Cash Flows Further Strengthening Cash Balances and Balance Sheet

- Fourth quarter net earnings were $103.0 million or $0.11 per share basic and diluted compared to net earnings of $14.6 million or $0.02 per share basic and diluted a year earlier.

- Adjusted net earnings(2) were $107.7 million or $0.11 per share basic and diluted.

- Fourth quarter cash flows from operating activities were $181.5 million and net free cash flow(2) was $118.9 million, exceeding the averages of the preceding three quarters by 25% and 6%, respectively.

- Fourth quarter cash flows from operating activities before net change in working capital were $207.4 million, and free cash flow before dividends and debt repayments(2) was $61.7 million.

- Net debt(2) decreased by an additional $53.4 million in the fourth quarter as a result of increased cash balances largely due the significant increase in free cash flow.

- For the full year, net debt(2) fell by $323.4 million to $565.7 million. The Company has achieved its financial management objective of a leverage ratio of net debt to EBITDA(2) of below 1.0x when assuming a bottom-of-cycle gold price of $1,350 per ounce, underscoring the Company's significant financial flexibility.

- As expected and planned, capital expenditures during the fourth quarter were higher than the third quarter as the result of timing delays caused by COVID-19, and interest was paid, as interest payments are customarily made in the second and fourth quarters. Further, a working capital outflow occurred due to the timing delays of collection of recoverable indirect tax credits, payments associated with prepaid expenditures and advances, and an inventory buildup due to production exceeding sales that will normalize in 2021.

- During the fourth quarter, the Company announced a further 50% increase to its annual dividend to $0.105 per share, driven by strong free cash flow generation.

(See end notes near end of release.)

| Three months ended December 31 | ||||||

| (In millions of United States Dollars) | 2020 | 2019 | ||||

| Net Free Cash Flow (2) | $ | 118.9 | $ | 123.2 | ||

| Free Cash Flow before Dividends and Debt Repayments (2) | $ | 61.7 | $ | 73.3 | ||

| Decrease in Net Debt (2) | $ | 53.4 | $ | 59.8 | ||

Fourth Quarter Operational Results

- Fourth quarter Gold Equivalent Ounce ("GEO")(1) production was 255,361 GEO(1) including gold and silver production of 221,659 ounces and 2.59 million ounces, respectively. The strong gold production followed standout performances from Jacobina and Minera Florida, and silver production was underpinned by an exceptionally strong performance from El Peñón.

- Full year GEO(1) production of 901,155 GEO(1), including 779,810 ounces of gold and 10.37 million ounces of silver, exceeded original guidance for the year of 890,000 GEO, and was within the plus or minus three per cent variance range of the Company's revised guidance. GEO(1) production for the year at Jacobina, El Peñón, Canadian Malartic, and Minera Florida were all well above plan. The entire difference was attributable to further changes to COVID-19 restrictions imposed in Argentina near the end of the year which impacted production at Cerro Moro.

Costs Offset by Margin Generated from Barnat Pre-Commercial Production

- Cash costs(2) for the quarter and full year were $675 and $701 per GEO(1), respectively, and all-in sustaining costs ("AISC")(2) for the quarter and full year were $1,076 and $1,080 per GEO(1), respectively.

- Full year cash costs(2) and AISC(2) were modestly higher than previously forecast, mostly impacted by lower production at Cerro Moro resulting from the re-imposition of national safety measures in Argentina in December. The Company had also anticipated that more production from Barnat at Canadian Malartic would be classified as commercial production, and as costs for such production were expected to be lower than the Company's average, overall costs would have been positively impacted. With more pre-commercial production from Barnat, costs were not positively impacted, but the margin generated from Barnat’s pre-commercial production was treated as a reduction to expansionary capital. This significant cash flow benefit resulted in the reduction of expansionary capital for the year by a further $14 million compared with plan. The net results of the modestly higher costs and lower expansionary capital was neutral, and consequently had little impact to overall generation of cash flows for the year.

Increased Gold Mineral Reserves and Mineral Resources

- Replaced mineral reserve depletion on a consolidated basis at operating mines.

- Significant increase in mineral resources:

- Notable increase in East Gouldie at Canadian Malartic of 1.84 million ounces (at 50%) of inferred mineral resources.

- Further, through the acquisition of the Wasamac project the Company has been able to increase its mineral inventory at a very advantageous purchase price.

- Lastly, inventory from the MARA project, which has generally been shown outside of the Company's subtotals has been added to inventory in the current year, given its advanced stage in the development process and the completion of the integration of the Agua Rica project and Minera Alumbrera plant and infrastructure.

MARA Project Integration

- On December 17, 2020, the Company completed the integration of the Agua Rica project with the Minera Alumbrera plant and infrastructure. Going forward, the integrated project will be known as the MARA project.

- Under the agreement, Yamana, as the sole owner of Agua Rica, and the partners of Alumbrera have created a new Joint Venture pursuant to which Yamana holds a controlling ownership interest in the MARA Project at 56.25%. Glencore holds a 25.00% interest and Newmont holds an 18.75% interest. Yamana will be the operator of the Joint Venture and will continue to lead the engagement with local, provincial, and national stakeholders, and completion of the Feasibility Study and Environmental Impact Assessment for the project.

- The integration creates significant synergies by combining existing substantive infrastructure that was formerly used to process ore from the Alumbrera mine during its mine life, including processing facilities; a fully permitted tailings storage facility; pipeline; logistical installations; ancillary buildings, and other infrastructure, with the future open pit Agua Rica mine.

Acquisition of Wasamac Property and Camflo Property and Mill (Acquisition of Monarch Gold)

- During the quarter, the Company announced the acquisition of the Wasamac property and the Camflo property and mill through the acquisition of all of the outstanding shares of Monarch Gold not owned by Yamana. The Company completed the acquisition on January 21, 2021.

- The Wasamac project, which has existing proven and probable mineral reserves of 1.8 million ounces of gold at 2.56 grams per tonne and excellent potential for future exploration success, further solidifies the Company’s long-term growth profile with a top-tier gold project in Quebec’s Abitibi region, where the Company has deep operational and technical experience and expertise.

Other Financial Updates: Impairment and Reversal of Impairment

- During the fourth quarter, the Company had a positive non-cash impact related to a net impairment of $191 million on a pre-tax basis, or approximately $37.6 million after-tax. The Company believes that its overall net asset value is also further enhanced by the acquisition of the Wasamac project and by the MARA project.

- After indicators of impairment reversal were noted at the El Peñón mine in Chile, the Company observed an increase in the recoverable amount of the unit, which resulted in a reversal of impairment of $560.0 million pre-tax, or $386.3 million after tax. This reversal was partially offset by a calculated pre-tax impairment of $369.0 million, or $348.7 million after tax, in respect of Cerro Moro, at which indicators of impairment were identified. For additional details, please refer to 'Section 3: Review of Financial Results' in the Company's Management Discussion & Analysis for the year ended December 31, 2020, available at www.yamana.com and on SEDAR.

CLIMATE CHANGE ACTION

As a continuation of Yamana’s climate change actions, the Company has formally adopted a climate strategy, approved by the Board of Directors, to demonstrate the Company’s commitment to the transition to a low-carbon future. The strategy is underpinned by adoption of two targets: a 2° C SBT and an aspirational net-zero 2050 target. The targets are supported by foundational work to be performed in 2021 to establish a multi-disciplinary Climate Working Group, determine our emissions baseline, develop the Greenhouse Gas (“GHG”) abatement pathways required to achieve the 2° C SBT and establish preliminary, operations-specific roadmaps that describe abatement projects, estimated costs and schedules. These actions will help ensure that our long-range GHG reduction efforts are supported by practical and operationally focused short, medium and long-term actions to achieve the targets.

Summary of Certain Non-Cash and Other Items Included in Net Earnings

| (In millions of United States Dollars, except per share amounts, totals may not add due to rounding) | Three Months Ended December 31 | Year Ended December 31, | ||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Non-cash unrealized foreign exchange losses | $ | 21.9 | $ | 0.6 | $ | 21.6 | $ | 29.0 | ||||||||

| Share-based payments/mark-to-market of deferred share units | 3.4 | 3.2 | 31.5 | 15.0 | ||||||||||||

| Mark-to-market (gains) losses on derivative contracts, investments and other assets | (5.8 | ) | (0.9 | ) | (6.9 | ) | 0.1 | |||||||||

| Gain on sale of subsidiaries, investments and other assets | (3.0 | ) | — | (1.4 | ) | (284.6 | ) | |||||||||

| Gain on discontinuation of the equity method of accounting | — | — | (21.3 | ) | — | |||||||||||

| Temporary suspension and standby costs | 2.2 | — | 18.4 | — | ||||||||||||

| Other incremental COVID-19 costs | 7.0 | — | 22.1 | — | ||||||||||||

| Share of one-off provision recorded against deferred income tax assets of associate | — | — | — | 13.0 | ||||||||||||

| Net reversal of impairment of mining properties | (191.0 | ) | — | (191.0 | ) | — | ||||||||||

| Financing costs paid on early note redemption | — | — | — | 35.0 | ||||||||||||

| Other provisions, write-downs and adjustments | 6.7 | 7.5 | 17.9 | 42.0 | ||||||||||||

| Non-cash tax on unrealized foreign exchange losses | 1.8 | (3.9 | ) | 52.8 | 17.9 | |||||||||||

| Income tax effect of adjustments | (2.4 | ) | (0.2 | ) | (19.7 | ) | (0.5 | ) | ||||||||

| One-time tax adjustments | 163.9 | 5.8 | 183.6 | 26.9 | ||||||||||||

| Total adjustments (i) | $ | 4.7 | $ | 12.1 | $ | 107.6 | $ | (106.2 | ) | |||||||

| Total adjustments - increase (decrease) to earnings per share attributable to Yamana equity holders | $ | — | $ | 0.01 | $ | 0.11 | $ | (0.11 | ) | |||||||

(i) For the three months ended December 31, 2020, net earnings attributable to Yamana equity holders would be adjusted by an increase of $4.7 million (2019 - increase of $12.1 million). For the year ended December 31, 2020, net earnings attributable to Yamana equity holders would be adjusted by an increase of $107.6 million (2019 - decrease of $106.2 million).

IMPRESSIVE TECHNICAL STUDY RESULTS FOR THE ODYSSEY UNDERGROUND PROJECT AT CANADIAN MALARTIC DRIVES APPROVAL OF CONSTRUCTION DECISION

Yamana and Agnico Eagle Mines Ltd., who each hold a 50% interest in the Canadian Malartic General Partnership, owner and operator of the Canadian Malartic mine, have approved construction of the Odyssey underground project. The decision reflects positive technical study results and confirms the Odyssey project as the next phase in the evolution of mining at Canadian Malartic, which has served as an economic beacon in Quebec’s Abitibi District for generations and will continue to do so for decades to come. An NI 43-101 technical report for the Canadian Malartic operation is expected to be filed in March 2021 and will include a summary of the Odyssey underground project.

The construction decision is a milestone in the ongoing evolution of the Canadian Malartic operation and is the culmination of several years of exploration, mineral resource development, and technical evaluation. It marks the transition point of the Odyssey underground project from the project definition phase to the construction and ramp-up phase, which will extend to 2028. From 2029 to 2039, the underground operation will be in full production, producing an expected 500,000 to 600,000 ounces per year. This represents an increase over the Company's initial estimate for an annual production platform of approximately 450,000 ounces. Further extension of the mine life beyond 2039 provides additional upside, with several opportunities under evaluation.

Odyssey Project Production Profile (100% basis)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/861adaad-1fb4-422b-888c-714ccda69ba4

About the Odyssey Project

Canadian Malartic has been a prolific mining operation for decades. Since 2011, it has been an open pit mine, but it has also been a successful underground operation in previous iterations. One of the strategic rationales behind Yamana's decision to jointly acquire Canadian Malartic from Osisko Mining in 2014 was the potential to significantly extend mine life by transitioning the operation to a future underground mine. Initial underground exploration drilling generated promising results, with the discovery of the East Gouldie zone in 2018 confirming the strong potential for a multi-hundred thousand ounce annual production operation with a decades-long mine life. As of year-end 2020, underground mineral resources have grown to approximately 14.4 million ounces of gold (100% basis) in just six years, including an increase of 4 million ounces from year-end 2019.

The Odyssey project hosts three main underground-mineralized zones, which are East Gouldie, East Malartic, and Odyssey, the latter of which is sub-divided into the Odyssey North, Odyssey South and Odyssey Internal zones. For the purpose of the technical study, mineable stope shapes were generated using a gold price of $1,250 per ounce, consistent with the price used for estimating Canadian Malartic open pit mineral reserves. Mineral resources at East Malartic below 600 metres from surface are not currently included in the technical study. A breakdown of the mineral resources used in the technical study, after dilution and mining recovery, is presented in the table below. Further details on the mineral resources are set out in the mineral reserve and mineral resource section of this news release.

Mineral Resources Included in Odyssey Project Technical Study as of December 31, 2020

| Zone | Indicated Mineral Resources | Inferred Mineral Resources | ||||||||||

| Tonnes (millions) | Grade (g/t Au) | Contained oz. (millions) | Tonnes (millions) | Grade (g/t Au) | Contained oz. (millions) | |||||||

| East Gouldie | — | — | — | 51.95 | 3.14 | 5.24 | ||||||

| East Malartic | 4.59 | 2.13 | 0.31 | 7.84 | 2.15 | 0.56 | ||||||

| Odyssey | 1.52 | 1.89 | 0.10 | 15.19 | 2.11 | 1.08 | ||||||

| Total | 6.18 | 2.00 | 0.41 | 75.90 | 2.82 | 6.88 | ||||||

The shallow mineralized zones located above 600 metres below surface will be mined using a ramp from surface. The deeper mineralized zones below 600 metres from surface will be mined with a production shaft.

In December 2020, ramp development was started on the Odyssey project in order to facilitate underground conversion drilling in 2021 and provide access to the Odyssey and East Malartic deposits. At year-end 2020, the ramp had progressed 102 metres, and an additional 2,850 metres of development is planned in 2021, of which 1,500 metres is in the ramp.

The conceptual mine design in the technical study includes a 1.8-kilometre deep production-services shaft equipped with a Blair hoist for production, a single drum hoist for services, and an auxiliary cage. The hoisting capacity is expected to be approximately 20,000 tpd. The project will also benefit from the existing infrastructure on site such as the tailing storage facilities, the process plant, and the maintenance facilities.

The preliminary mining concept is based on a sublevel open stoping mining method with paste backfill. Longitudinal retreat and transverse primary-secondary mining methods will also be used dependent on mineralization geometry and stope design criteria.

The Odyssey project is expected to be one of the most modernized electric underground mines. All major mobile production equipment (such as trucks, scoop trams, jumbos, bolters, and longhole drill rigs will be electric powered), greatly reducing carbon footprint. On the two main levels with loading pockets, trucks and hammers would be remotely operated 24 hours a day, 7 days a week from a surface control room, greatly increasing equipment utilization.

Production via the ramp is expected to begin at Odyssey South in late 2023, increasing to up to 3,500 tpd in 2024. Collaring of the shaft and installation of the headframe is expected to commence in the second quarter of 2021, with shaft sinking activities expected to begin in late 2022. The shaft will have an estimated depth of 1,800 metres and the first loading station should be commissioned in 2027 with modest production from East Gouldie. The East Malartic shallow area and Odyssey North zones are scheduled to enter production in 2029 and 2030, respectively.

The project is expected to mine 19,000 tpd from the underground from four different mining zones:

- East Gouldie – 12,500 tpd

- Stope production starts in 2027;

- Three-year ramp up (2027-2029);

- Full stope production in 2030 to 2038.

- Odyssey North – 3,500 tpd

- Stope production starts in 2030;

- Full stope production in 2031-2038.

- Odyssey South and East Malartic – 3,500 and 3,200 tpd, respectively

- Odyssey South stope production starts in 2023;

- Odyssey South full stope production in 2024 to 2027 (3,500 tpd);

- East Malartic stope production starts in 2028;

- East Malartic full stope production in 2030 to 2039 (3,200 tpd).

Run-of–mine ore from the open pit will start to decrease in 2023, as the ore production from the underground starts at a rate of 3,000 tpd. The underground should reach full production of about 19,000 tpd by 2031.

Robust Project Economics

Initial expansionary capital of $1.14 billion is expected to be spent over a period of eight years (100% basis), with capital requirements in any given year manageable and fully funded using the Company's cash on hand and free cash flow generation. Additionally, other growth capital expenditures and modest sustainable capital during the construction period total $191.4 million. Gold production during the 2021 to 2028 construction period is expected at 932,000 ounces (on a 100% basis) at cash costs of $800 per ounce. The net proceeds from the sale of these ounces would significantly reduce the external cash requirements for the construction of the project which, assuming the gold price used in the financial analysis for the project, would reduce the projected capital requirements in half.

Average annual payable production is expected to be approximately 545,400 ounces (100% basis) from 2029 to 2039, with total cash costs per ounce of approximately $630 per ounce. Sustaining capital is expected to gradually decline from 2029 to 2039, with an expected average of approximately $55.8 million per year.

The production profile is based on a ramp-up period of six years (2023-2028) followed by 11 years of full production (2029-2039), for a total of 82.1 million tonnes of underground ore processed (100% basis) at an average gold grade of 2.76 g/t, representing approximately 50% of the contained mineral resource gold ounces. On this basis, the after-tax net present value (“NPV”) (at a 5% discount rate) and after-tax internal rate of return (“IRR”) of the Odyssey project are shown at various gold price assumptions in the table below. The cut-off grade used to estimate the mineable inventory is based on a gold price of $1,250 per ounce, while the financial model uses a base case gold price assumption of $1,550 per ounce. Costs are estimated using a Canadian to U.S. dollar foreign exchange rate assumption of 1.30.

Odyssey Project Technical Study Sensitives to Gold Price (100% Basis)

| Gold Price (USD/oz) | $1,085 | $1,250 | $1,395 | $1,550 | $1,705 | $1,860 | $2,015 | |||||||

| NPV 5% (USD millions, after-tax) | $82 | $481 | $801 | $1,143 | $1,494 | $1,853 | $2,212 | |||||||

| IRR (%, after-tax) | 6% | 11% | 14% | 17.5% | 20% | 23% | 26% |

These results demonstrate the expected returns of the Odyssey project after the first decade at full production, highlighting Odyssey as a robust project with significant leverage to higher gold prices and thus supporting the approval for project construction. The results are not intended to reflect the full value of the Odyssey project and extension of mine life beyond 2039 represents significant further upside.

Given the strong underground mining experience of the partners and the experience gained from operating the Canadian Malartic mine since 2014, there is a high degree of confidence in many of the cost assumptions used for the project. While the technical study is considered at a preliminary economic assessment level, the partnership believes that estimates for such things as underground development and mining costs, processing costs, and equipment procurement are more advanced than what would typically be estimated in a preliminary economic assessment level study for a project of this scope. The capital allocation and classification of costs will continue to be refined as the project advances. A preliminary economic assessment is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and, therefore, there is no certainty that the preliminary economic assessment will be realized.

The East Gouldie mineralization is the largest and most profitable deposit due to higher grade and tonnage with more than 70% of the total ounces produced. Exploration drilling at East Gouldie in 2020 totalled 97,000 metres (100% basis), including 25,600 metres in the fourth quarter with multiple mother holes and wedge cuts that resulted in 25 new pierce points in the zone, plus several more in the Odyssey related zones. The intensive drilling program in 2020 has allowed the partnership to increase the inferred mineral resource of the East Gouldie zone by 134% to 6.4 million ounces of gold (100% basis), compared to the initial inferred mineral resource declared at year-end 2019, with an average grade of 3.17 g/t.

The focus of the ongoing diamond drilling campaign from surface is to further define high quality mineral resources by the beginning of 2023 with a drill hole spacing of 75 metres. Improving the geological confidence of the mineral resources is expected to further de-risk future production. With further exploration the Company believes that additional mineralization will come into the mine plan in the coming years.

| Odyssey Project Summary | |||

| (All numbers are approximate and on a 100% basis) | |||

| Estimated Total Production | 6,932 | thousands of gold ounces | |

| Average metallurgical recovery | ~95.2% | gold | |

| Average Annual gold production | |||

| 2023 | 46,600 oz | (825 k. tonnes, 1.84g/t gold) | |

| 2024 to 2026 (average per year) | 81,500 oz | (1,344 k. tonnes, 1.98g/t gold) | |

| 2027 | 256,200 oz | (2,810 k. tonnes, 2.98g/t gold) | |

| 2028 | 384,600 oz | (3,333 k. tonnes, 3.79g/t gold) | |

| 2029 to 2039 (average per year) | 545,400 oz | (6,463 k. tonnes, 2.76g/t gold) | |

| Minesite costs per tonne | |||

| 2023 | $93.0 | C$/t | |

| 2024 to 2026 (average per year) | $77.0 | C$/t | |

| 2027 | $79.0 | C$/t | |

| 2028 | $79.0 | C$/t | |

| 2029 to 2039 (average per year) | $61.0 | C$/t | |

| Average total cash costs on a by-product basis (including royalty and refining costs) | |||

| 2023 to 2028 | 800 | US$/oz | |

| 2029 to 2039 | 630 | US$/oz | |

| Royalty | 5.5% | NSR | |

| Mine life | 17 | years | |

| Capital Expenditures | |||

| Initial capital Expenditures | $1,143.7 | million US$ (2021 to 2028) | |

| Gold production | 932.0 | thousand ounces (2021 to 2028) | |

| Sustaining CAPEX | $55.8 | million US$ (2029 - 2039 average per year) | |

| Breakdown of Capital Expenditures by year | |||

| 2021 | $113.8 | million US$ | |

| 2022 | $204.0 | million US$ | |

| 2023 | $136.8 | million US$ | |

| 2024 to 2026 (average per year) | $163.8 | million US$ | |

| 2027 | $209.0 | million US$ | |

| 2028 | $180.3 | million US$ | |

| Breakdown of Capital Expenditures by category | |||

| Shaft & Surface | $478.4 | million US$ | |

| Mining Equipment | $162.7 | million US$ | |

| U/G Development & Construction | $502.6 | million US$ | |

| Subtotal of Initial Capital Expenditures | $1,143.7 | million US$ | |

| Other Growth Capital Expenditures | $191.4 | million US$ | |

| Reclamation Costs | $3.9 | million US$ for Odyssey Project only | |

The aforementioned costs do not include any offsetting net proceeds from pre-commercial production. Historically, any net proceeds from pre-commercial production were deducted from development capital expenditures; however, due to amendments to the relevant accounting standard that become effective from 2022, this treatment will not be permitted when accounting for the Odyssey project. Specifically, in May 2020, the International Accounting Standards Board ("IASB") issued Property, Plant and Equipment: Proceeds before Intended Use (Amendments to IAS 16), which prohibits entities from deducting amounts received from selling items produced from the cost of property, plant and equipment while the Company is preparing the asset for its intended use. Instead, sales proceeds and the cost of producing these items will be recognized in the consolidated statements of operations.

Permits for Odyssey North and South were granted in 2020 to allow the first phase of the project to begin. At this time, the Certificate of Authorization (“CofA”) for the shaft has not yet been obtained and the CofA for the waste rock management needs to be modified.

A request for a decree amendment, including permits to develop the East Gouldie and East Malartic zones will be sent to the Quebec Ministry of Environment and the Fight Against Climate Change in the first quarter of 2021. If there are no serious hurdles, the project could obtain the necessary approvals from provincial regulators in approximately 12 months. The project team has received a letter confirming that mining the additional zones at the project does not trigger any additional Federal permitting requirements.

Facilitating the Transition from Open Pit Mining

Currently, in the open pit, mining is transitioning from the Canadian Malartic pit to the Barnat pit, which is now in commercial production. Seventy percent of the total tonnes mined in 2021 are expected to come from Barnat. The Canadian Malartic pit will be depleted in the first half of 2023 and waste rock and tailings will be deposited into the pit beginning in 2023.

The operation will progressively shift from open pit to underground mining between 2023 to 2028. To help facilitate this transition, the Company optimized the design of the Barnat pit, adding 290,000 ounces to mineral reserves (100% basis), which will help fill the production gap between 2026 and 2029 as the operation completes the transition to underground mining.

The Partnership is evaluating an additional opportunity to increase production during the transition period by processing low-grade stockpile that is not currently included in mineral reserves. This stockpile is economic at current gold prices and would add an extra 170,000 ounces to planned production on a 100% basis.

Odyssey and Wasamac Increase Company’s Presence in Quebec’s Prolific Abitibi Region

The development of the Odyssey project coupled with the recently acquired Wasamac project will significantly enhance the Company’s long-term production profile and further expand its presence in the Abitibi District, a prolific mining district in which Yamana has extensive experience and expertise. The Wasamac project, located 100 kilometres west of Canadian Malartic, has existing proven and probable mineral reserves of 1.8 million ounces of gold at 2.56 grams per tonne and possesses many parallels to the Odyssey project. There is excellent potential for significant future exploration success and mineral resource conversion at Wasamac, with the deposit remaining open at depth and along strike.

2021 - 2023 PRODUCTION GUIDANCE

The following table presents the Company's total gold, silver and gold equivalent ounces ("GEO") production expectations in 2021, 2022 and 2023. Actual production for the year-ended December 31, 2020 includes comparative operations, which comprise those mines in the Company's portfolio as of December 31, 2020. The Company notes that it guides on GEO production and costs based on a particular assumption of gold and silver prices. Although underlying gold and silver production does not change with the fluctuation in gold and silver prices, the change in the GEO ratio from such fluctuations may result in a different GEO production than that guided.

The production profile for 2021 to 2023 shows sequential growth in gold production. Several growth opportunities are available, and in the near and medium-term the Company remains focused on optimizing the existing portfolio of five operating mines while also advancing studies for various expansion projects and longer term development assets.

Production guidance for 2021 is slightly below the Company's guidance for 2021 from last year, entirely related to Cerro Moro. A more conservative production risk adjustment has been applied to Cerro Moro during 2021 to reflect the continued impact of Covid-19 related restrictions, as experienced in December. Costs for the mine have also been commensurately risk-adjusted.

The Company expects to continue its established trend of delivering stronger production in the second half of the year, with approximately 53% of production slated for the second half, along with quarterly sequential increases in production.

The Company looks at production within a normal range of +/- 3%, and the guidance values reflect both the mid-point and the range for the 2021-2023 period. With improved mine plans, the Company is also providing its maiden three-year guidance by mine as follows:

| (000's ounces) | 2020 Actual | 2021 Guidance | 2022 Guidance | 2023 Guidance | |||

| Mid-Point | Range | Mid-Point | Range | Mid-Point | Range | ||

| Total gold production (3) | 780 | 862 | 836 - 888 | 870 | 844 - 896 | 889 | 862 - 916 |

| Total silver production | 10,366 | 10,000 | 9,700 - 10,300 | 9,400 | 9,118 - 9,682 | 8,000 | 7,760 - 8,240 |

| Total GEO production (i) | 901 | 1,000 | 970 - 1,030 | 1,000 | 970 - 1,030 | 1,000 | 970 - 1,030 |

(i) GEO assumes gold ounces plus the equivalent of silver ounces using a ratio of 88.86 for 2020, and a ratio of 72.00 for 2021, 2022 and 2023.

The following table presents mine-by-mine production results for Yamana Mines for 2020 and updates guidance provided on January 25, 2021, as the Company is now providing mine-by-mine guidance for the next three years:

| (000's ounces) | Gold | ||||||

| 2020 Actual | 2021 Guidance | 2022 Guidance | 2023 Guidance | ||||

| Mid-Point | Range | Mid-Point | Range | Mid-Point | Range | ||

| Canadian Malartic (50%)(3) | 284 | 350 | 340 - 361 | 330 | 320 - 340 | 350 | 340 - 361 |

| Jacobina | 178 | 175 | 170 - 180 | 180 | 175 - 186 | 185 | 179 - 191 |

| Cerro Moro | 67 | 90 | 87 - 93 | 100 | 97 - 103 | 90 | 87 - 93 |

| El Peñón | 161 | 160 | 155 - 165 | 165 | 160 - 170 | 165 | 160 - 170 |

| Minera Florida | 90 | 87 | 84 - 90 | 95 | 92 - 98 | 99 | 96 - 102 |

| Total | 780 | 862 | 836 - 889 | 870 | 844 - 897 | 889 | 862 - 916 |

| (000's ounces) | Silver | ||||||

| 2020 Actual | 2021 Guidance | 2022 Guidance | 2023 Guidance | ||||

| Mid-Point | Range | Mid-Point | Range | Mid-Point | Range | ||

| Cerro Moro | 5,449 | 5,500 | 5,335 - 5,665 | 5,000 | 4,850 - 5,150 | 3,500 | 3,395 - 3,605 |

| El Peñón | 4,917 | 4,500 | 4,365 - 4,635 | 4,400 | 4,268 - 4,532 | 4,500 | 4,365 - 4,635 |

| Total | 10,366 | 10,000 | 9,700 - 10,300 | 9,400 | 9,118 - 9,682 | 8,000 | 7,760 - 8,240 |

| (000's ounces) | GEO | ||||||

| 2020 Actual | 2021 Guidance | 2022 Guidance | 2023 Guidance | ||||

| Mid-Point | Range | Mid-Point | Range | Mid-Point | Range | ||

| Canadian Malartic (50%)(3) | 284 | 350 | 340 - 361 | 330 | 320 - 340 | 350 | 340 - 361 |

| Jacobina | 178 | 175 | 170 - 180 | 180 | 175 - 186 | 185 | 179 - 191 |

| Cerro Moro | 132 | 166 | 161 - 171 | 169 | 164 - 174 | 138 | 134 - 142 |

| El Peñón | 217 | 222 | 215 - 229 | 226 | 219 - 233 | 228 | 221 - 235 |

| Minera Florida | 90 | 87 | 84 - 90 | 95 | 92 - 98 | 99 | 96 - 102 |

| Total | 901 | 1,000 | 970 - 1,030 | 1,000 | 970 - 1,030 | 1,000 | 970 - 1,030 |

Cost Outlook

The Company anticipates that it will continue to incur some costs in relation to COVID-19 in the near future. Current expectation of pandemic related costs is that those costs will continue to be incurred during the first half of the year and begin to decrease in the second half of the year with a rollout of vaccinations expected in most countries in which the Company operates. With increasing numbers of the population receiving the vaccine, we would expect to see increasing immunity and decreasing caseloads, allowing for gradual easing of our COVID-related controls and associated costs toward the second half of 2021 as noted. Total costs are expected to not exceed approximately $20 million for the year. Similar to 2020, COVID-19 costs are disclosed as part of mine operating earnings as temporary suspension, standby and other incremental COVID-19 costs and are excluded from cash costs and all-in sustaining costs (“AISC”).

The expected decline in COVID-19 costs throughout the upcoming year also corresponds to the Company’s customary lower second half of the year costs, associated with higher production levels.

The following table presents cost of sales, cash costs and AISC results in 2020 and guidance ranges for 2021.

| (In US dollars) | Total cost of sales per GEO sold | Cash costs per GEO sold (2) | AISC per GEO sold (2) (i) | |||||||||

| 2020 Actual | 2021 Guidance | 2020 Actual | 2021 Guidance | 2020 Actual | 2021 Guidance | |||||||

| Canadian Malartic (50%) (i) | $ | 1,207 | 1,100-1,145 | $ | 702 | 635-675 | $ | 945 | 850-885 | |||

| Jacobina | $ | 844 | 850-885 | $ | 544 | 565-600 | $ | 746 | 735-765 | |||

| Cerro Moro | $ | 1,513 | 1,450-1,510 | $ | 868 | 790-835 | $ | 1,280 | 1,175-1,225 | |||

| El Peñón | $ | 980 | 1,140-1,180 | $ | 657 | 620-660 | $ | 922 | 835-870 | |||

| Minera Florida | $ | 1,366 | 1,170-1,220 | $ | 862 | 740-785 | $ | 1,152 | 1,065-1,105 | |||

| Total | $ | 1,151 | 1,140-1,190 | $ | 701 | 655-695 | $ | 1,080 | 980-1,020 | |||

(i) Mine site AISC includes cash costs, mine site general and administrative expense, sustaining capital, capitalized exploration and expensed exploration. Consolidated AISC incorporates additional non-mine site costs including corporate general and administrative expense.

The following table presents expansionary capital, sustaining capital, and total exploration spend results for 2020 and expectations by mine for 2021:

| Expansionary capital | Sustaining capital | Total exploration | ||||||||||||||||

| (In millions of US Dollars) | 2020 Actual | 2021 Guidance | 2020 Actual | 2021 Guidance | 2020 Actual | 2021 Guidance | ||||||||||||

| Canadian Malartic (50%) (i) | $ | 12.2 | $ | 63.0 | $ | 52.5 | $ | 73.0 | $ | 10.1 | $ | 15.0 | ||||||

| Jacobina | 15.8 | 29.0 | 21.6 | 19.0 | 6.0 | 12.0 | ||||||||||||

| Cerro Moro | 6.9 | 1.0 | 29.5 | 40.0 | 12.5 | 18.0 | ||||||||||||

| El Peñón | 0.5 | 1.0 | 31.4 | 31.0 | 15.9 | 18.0 | ||||||||||||

| Minera Florida | 19.9 | 17.0 | 12.6 | 19.0 | 7.0 | 11.0 | ||||||||||||

| MARA | 8.0 | 15.0 | — | — | — | — | ||||||||||||

| Wasamac | — | 5.0 | — | — | — | 11.0 | ||||||||||||

| Other capital | 3.5 | 1.0 | 1.7 | 1.0 | — | — | ||||||||||||

| Generative exploration (expensed) | — | — | — | — | 15.1 | 18.0 | ||||||||||||

| Other exploration and overhead | — | — | — | — | 6.1 | 7.0 | ||||||||||||

| Total | $ | 66.8 | $ | 132.0 | $ | 149.3 | $ | 183.0 | $ | 72.7 | $ | 110.0 | ||||||

(i) 2021 guided Expansionary Capital has been revised to reflect the positive construction decision on Odyssey at Canadian Malartic.

Approximately 70% of the Company’s expected exploration spend is capital in nature.

Capital expenditure values for 2021 do not include the cost to add to long-term ore stockpile balances at Canadian Malartic. These costs are estimated at $15.0 million for 2021 compared to $5.9 million for 2020, both on a 50% basis.

The following table presents other expenditure results in 2020 and expectations for 2021:

| (In millions of US Dollars) | 2020 Actual | 2021 Guidance | ||||

| Total DDA | $ | 395.0 | $ | 470.0-500.0 | ||

| Cash based G&A | $ | 65.8 | $ | 72.0 | ||

| Cash income taxes paid (i) | $ | 99.3 | $ | 180.0-200.0 | ||

(i) Cash taxes paid consider payments made in relation to withholding tax and prior years, as in certain jurisdictions, final payments related to a fiscal year’s taxes are settled in the next fiscal year.

Guidance Assumptions

Key assumptions, in relation to the above guidance, are presented in the table below.

| 2020 Actual (i) | 2021 Guidance | |||||

| GEO Ratio | 88.86 | 72.00 | ||||

| Gold | $ | 1,770 | $ | 1,800 | ||

| Silver | $ | 20.51 | $ | 25.00 | ||

| USD-CAD | 1.34 | 1.28 | ||||

| USD-BRL | 5.16 | 5.25 | ||||

| USD-CLP | 792.17 | 725.00 | ||||

| USD-ARS | 70.65 | 108.00 | ||||

(i) Metal prices and exchange rates shown in the table above are the average metal prices and exchange rates for the year ended December 31, 2020.

10-YEAR OUTLOOK: ADDITIONAL INFORMATION

The Company recently announced its 10-year outlook, highlighting a strong and sustainable production platform of at least 1 million GEO per year through 2030. As noted, production will be underpinned by continued operational success at the Company’s existing operations, which have consistently replaced mineral reserves above depletion, including in 2020. In addition, production will be driven by the now approved Odyssey underground project at Canadian Malartic, incremental production growth at Minera Florida, further expansions at Jacobina, and continued exploration success and mine life extension at Cerro Moro.

The Company reiterates this outlook and, with the benefit of its now completed mineral reserve and mineral resource update, provides this additional information.

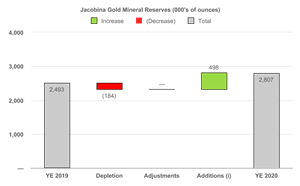

Jacobina replaced 2020 depletion of gold mineral reserves and added approximately 300,000 ounces of additional reserves, based on positive infill drilling results at all mines and especially at Canavieiras Central, where drilling has added indicated mineral resources in the high grade LUT reef and lower grade parallel reefs. Average mineral reserve grade has modestly decreased as a result of such parallel reefs that are considered economical to mine. Operational costs will consequently not be affected by the change in reserve grade. In the short term, the Company expects to continue processing at a grade higher than average mineral reserves grade, as reflected in the 2020 average feed grade of 2.36 g/t. These lower grade mineral reserves also provide opportunities for incremental lower-cost mill feed in excess of the planned throughput rates, in the event that the processing plant optimizations and expansions exceed targeted throughput rates. Measured and indicated mineral resources and inferred mineral resources both increased from year end 2019, with total gold mineral resources and mineral reserves increasing by 823,000 ounces. The continued mineral reserve and mineral resource growth establishes Jacobina as a multi-decade operation and supports the ongoing production growth trend towards 230,000 ounces of gold per year after the implementation of the Phase 2 expansion project. As a result of the exploration success, the Company is now considering further growth opportunities including a potential Phase 3 expansion to 10,000 tpd.

At El Peñón, which recently completed its twenty-first year of production, the Company has a high degree of confidence that it will continue to replace mineral reserves through new discoveries and infill drilling on several major veins, thereby maintaining mine life visibility for at least another 10 years.

The Company further clarifies that El Peñón's outlook is fully supported by mineral reserves and mineral resources. Mineral resources are comprised of multiple veins at different grades. The Company plans to draw into inventory higher conviction mineral resources from veins which are at mineral reserve grade and close to the existing mine. The Company notes an increase in mineral reserve grade from 2019, highlighting that new ounces being converted to mineral reserves are higher than average mineral reserve grade. Moreover, the Company continues to make new discoveries of mineral inferred ounces that are also at better grades, as noted by an increase in mineral resource grade.

STRATEGIC DEVELOPMENTS

Jacobina, Brazil

The Phase 1 optimization project was completed in June. The project has exceeded expectations, with a higher than planned steady state of approximately 6,800 tpd achieved in both the second and third quarters. The Company has identified opportunities to further optimize the results and recoveries achieved in Phase 1 with a modest investment. Consequently, works commenced in the third quarter for the expansion of the gravity concentration circuit, with commissioning scheduled and on-track for mid-2021 and with an objective to optimize gold recovery at the higher throughput rate.

In addition to the incremental optimization of Phase 1, the Company is advancing the Phase 2 expansion at Jacobina, for an increase in throughput to 8,500 tpd. The Company is currently in the engineering phase, with permitting underway. Included in the mine's expansionary budget in 2021 of $29.0 million, is approximately $18.0 million for the procurement of long-lead items and expansionary development to support the higher throughput to the mill. The throughput increase will be achieved through the installation of an additional grinding line and incremental upgrades to the crushing and gravity circuits. The Phase 2 expansion is expected to increase annual gold production to approximately 230,000 ounces per year, representing a 28% increase from current levels, reduce costs, and generate significantly more cash flow and attractive returns. The Company expects to provide an update regarding capex and development schedule in mid-2021 once studies are finalized to conclude permitting.

The Company anticipates that the updated capital costs will not exceed the previously estimated and disclosed $57 million, and it has already begun to incur these costs for long-lead time items. The estimated capital costs of $57 million had been based on an assumed BRL:USD rate of 4.0. The BRL:USD foreign exchange rates are currently higher at over 5.0, and consequently, the Company anticipates that the weaker rates will provide capital cost and operating cost benefits.

Separately, Jacobina is studying the installation of a backfill plant to allow up to 2,000 tpd of tailings to be deposited in underground voids. A concept study was completed in the second quarter, with preliminary results indicating that the project would improve the way in which the Company manages the environment and environmental impact, extend the life of the existing tailings storage facility consequently decreasing future capital investment intensity, and improve mining recovery resulting in an increased conversion of mineral resources to mineral reserves. The placement of backfill in empty stopes would allow for greater recovery of mineralized pillars that otherwise would have been left behind to ensure ground stability. Backfill in strategic higher grade zones would increase mineral reserves with the recovery of those mineralized pillars. In addition, the improvement in ground stability would have a positive impact on dilution. The current backfill system design includes a tailings classification plant, located close to the existing processing plant, and two backfill preparation plants at the João Belo and Morro do Vento mines. The Company is advancing the backfill project to a feasibility study, to be completed by the end of the first quarter of 2021.

Lastly, the Company has also begun a conceptual study on a Phase 3 expansion, which would increase throughput to 10,000 tpd, utilize the existing grinding line, while expanding crushing and leaching circuits and adding additional mining equipment and infrastructure.

MARA Project (Agua Rica and Alumbrera Integration), Argentina

On December 17, 2020, the Company completed the project integration (the "Integration Transaction") with Glencore International AG and Newmont Corporation and a new partnership was formed to manage, develop and operate the project. The development will be pursuant to the plan contemplated in the agreement and by the partners, and the Agua Rica project will be developed and operated using the existing infrastructure and facilities of Alumbrera in the Catamarca Province of Argentina. Going forward, the integrated project will be known as the MARA Project.

Under the agreement, Yamana, as the sole owner of Agua Rica, and the partners of Alumbrera have created a new Joint Venture pursuant to which Yamana holds a controlling ownership interest in the MARA Project at 56.25%. Glencore holds a 25.00% interest and Newmont holds an 18.75% interest. Yamana will be the operator of the Joint Venture and will continue to lead the engagement with local, provincial, and national stakeholders, and completion of the Feasibility Study and Environmental Impact Assessment ("EIA") for the MARA project. A MARA Joint Venture Technical Committee has been formed and comprises representatives of the three companies.

The Integration Transaction creates significant synergies by combining existing substantive infrastructure which was formerly used to process ore from the Alumbrera mine during its mine life, including processing facilities, a fully permitted tailings storage facility, pipeline, logistical installations, ancillary buildings, and other infrastructure, with the future open pit Agua Rica mine. The result is a significantly de-risked project with a smaller environmental footprint and improved efficiencies, creating one of the lowest capital intensity projects in the world as measured by pound of copper produced and in-situ copper mineral reserves.

The Pre-feasibility Study ("PFS") for the Integrated Project considers the Agua Rica deposit mined via a conventional high tonnage truck and shovel open pit operation. Average life of mine material moved is expected to be approximately 108 million tonnes per year, with ore feed of 40 million tonnes per year and average life of mine strip ratio of 1.66.

This PFS provides the framework for the preparation and submission of a new EIA to the authorities of the Catamarca Province and for the continued engagement with local stakeholders and communities. The Companies began the EIA process in 2019, given the level of significant detail in the PFS.

The Joint Venture Technical Committee advanced optimization studies in late 2019 and early 2020, and is now advancing a full Feasibility Study on the Integrated Project, with updated mineral reserve, production and project cost estimates. It has also obtained a provisional Permit for early exploration works from the local authorities in order to conduct field work for the Feasibility Study and collect additional information for the Integrated Project EIA. COVID-19 has introduced uncertainty into the timeline relating to the completion of the Feasibility Study, mainly due to environmental permit approvals and field work, although as the permit process is well advanced, work preparation has begun in anticipation of receiving necessary authorizations in normal course. Despite the aforementioned delays, Feasibility Study work is ongoing and key technical results are expected during 2021. While the Company continues to advance the Feasibility Study, it notes that a considerable amount of information in the PFS is already at Feasibility Study level mostly as a result of the Integration Transaction. The full Feasibility report and EIA completion are expected in 2022.

The most recent technical studies have confirmed that the processing facility at Alumbrera is capable of processing up to 44.0 million tonnes per year, with minor additional capital expenditures, which represents a significant upside to the PFS results. Further tests and studies are scheduled for the Feasibility Study stage in order to confirm and optimize the concentrate transportation capacity of the pipeline and the mining plan to support higher throughput. In addition, upside opportunities have already been identified by re-sequencing low grade stockpile, and are expected to provide significant further value for the integrated project. The estimated expenses for the Company to advance the project through the Feasibility Study and EIA are in the range of $20.0 million to $25.0 million for the next three years (Yamana's 56.25% interest), representing a manageable and modest investment in relation to the value creation of advancing the Integrate Project to the next phases of development.

After a strategic review, the Company has concluded that MARA represents an excellent development and growth project which the Company intends to continue to advance through the development process through the Company's controlling interest in the project.

The Company acquired cash and cash equivalents of $222.5 million in the acquisition of Alumbrera.

For further details on the Integration Transaction, critical accounting policies, and critical judgments, please refer to the Company's consolidated financial statements for the year ended December 31, 2020.

Acquisition of Wasamac Property and Camflo Property and Mill (Monarch Gold Acquisition)

On January 21, 2021, the Company completed its acquisition of the Wasamac property and the Camflo property and mill (the “Acquisition Properties”) through the acquisition of all of the outstanding shares of Monarch Gold Corporation (“Monarch”) not owned by Yamana. Yamana previously announced that it had entered into a definitive agreement with Monarch Gold on November 2, 2020, to acquire the properties, under a plan of arrangement.

The addition of the Wasamac project to Yamana’s portfolio further solidifies the Company’s long-term growth profile with a top-tier gold project in Quebec’s Abitibi region, a prolific mining district where Yamana has deep operational and technical expertise and experience. The geological characteristics of the Wasamac ore body suggest it holds the potential to be an underground mine with the potential to achieve the same scale, grade, production, and costs as Yamana’s successful Jacobina mine in Brazil, and it possesses many parallels to the underground project at Canadian Malartic.

Wasamac consists of a single, continuous shear zone with a consistent grade distribution and wide mining widths, making it amenable to simple, productive, and cost efficient underground bulk mining methods. The deposit has existing proven and probable mineral reserves of 21.45 million tonnes at 2.56 g/t for total proven and probable mineral reserves of 1.8 million ounces of gold. Mineral resources and proven and probable mineral reserves are supported by a Feasibility Study previously completed by Monarch in 2018 (the “Wasamac Feasibility Study”). The Wasamac Feasibility Study outlined a 6,000 tonnes per day operation with average gold production of 160,000 ounces per year. Costs are expected to be at the lower end of the Company’s profile, providing an improvement to consolidated costs.

There remains excellent potential for significant future exploration success and mineral resource conversion, with the Wasamac deposit remaining open at depth and along strike. Yamana plans to build on the ongoing permitting and social licensing effort carried out by Monarch, applying the Company’s strong ESG framework and best practices, and leveraging the Company’s extensive experience in permitting and proven track record of building strong, respectful, and mutually beneficial relationships with the communities and governments wherever it operates. Building off the work completed to date, Yamana plans to commence an exploration and infill drilling campaign and other studies to refine and expand upon the potential of Wasamac and its development alternatives, with an update on these plans to be provided by the third quarter of 2021.

Prior to closing the acquisition of Wasamac, in late 2020 the Company began the process of opening a regional office in the Abitibi region, and hiring personnel to manage the permitting process and related studies to update the Feasibility Study.

GENERATIVE EXPLORATION PROGRAM AND STRATEGY

The 2020 generative exploration program focused on finding higher quality ounces, improving mine grade, infill drilling to replace production by upgrading existing mineral resources, and exploring the Yamana property portfolio as well as several joint venture opportunities. The following are key elements and objectives of the program:

- Target the Company’s most advanced exploration projects while retaining the flexibility to prioritize other projects in the portfolio as and when merited by drill results.

- Add new inferred mineral resources of at least 1.5 million ounces of gold equivalent within the next three years to move at least one project towards a preliminary economic assessment.

- On a longer term basis, advance at least one project to a mineral inventory that is large enough to support a mine plan demonstrating positive economics with annual gold production of approximately 150,000 ounces for at least eight years.

- Advance both gold-only and copper-gold projects and, in the latter case, consider joint venture agreements aimed at increasing mineral resource and advancing the project to development while Yamana maintains an economic interest in the project.

During the fourth quarter, exploration drilling and other field activities continued to ramp up in most jurisdictions as responses to COVID-19 restrictions were managed. Drilling activities continued in Brazil at Ivolandia to expand the near surface oxide targets, and drilling was reinitiated at Lavra Velha and Borborema, as described in more detail below. Exploration drilling was also initiated at Jacobina Norte during the fourth quarter. Exploration in Chile in the fourth quarter included RC scout drill testing at several early-stage projects near the El Peñón mine. Exploration in Argentina was limited due to travel restrictions, but drilling in 2021 is planned to test breccia-related high-sulphidation epithermal gold targets on the Company’s Las Flechas property. At Monument Bay, Manitoba, an initial Phase I deep drilling program was completed, designed to test the down plunge projections of modeled, plunging high-grade zones at the Twin Lakes deposit.

The Company is budgeting $18.0 million of generative exploration expenses in 2021. The generative exploration program targets advanced and advancing exploration projects in Yamana's existing portfolio, particularly Canada and Brazil.

YEAR END MINERAL RESERVES AND MINERAL RESOURCES SUMMARY

As at December 31, 2020

| Proven and probable mineral reserves | |||||

| Tonnes (000's) | Grade (g/t) | Contained oz. (000's) | |||

| Gold | 765,505 | 0.56 | 13,803 | ||

| Silver | 633,832 | 5.5 | 112,780 | ||

| Measured and indicated mineral resources | |||||

| Tonnes (000's) | Grade (g/t) | Contained oz. (000's) | |||

| Gold | 485,681 | 0.94 | 14,604 | ||

| Silver | 165,889 | 9.2 | 49,004 | ||

| Inferred mineral resources | |||||

| Tonnes (000's) | Grade (g/t) | Contained oz. (000's) | |||

| Gold | 653,662 | 0.75 | 15,714 | ||

| Silver | 444,541 | 4.4 | 62,859 | ||

Additional details relating to the Company’s mineral reserve and mineral resource estimates as at December 31, 2020 are presented below.

Jacobina, Brazil

Jacobina replaced 2020 depletion of gold mineral reserves and added approximately 300,000 ounces of additional reserves, based on positive infill drilling results at all mines and especially at Canavieiras Central, where drilling has added indicated mineral resources in the high grade LUT reef and lower grade parallel reefs. Average mineral reserve grade has modestly decreased as a result of such parallel reefs that are considered economical to mine. Operational costs will consequently not be affected by the change in reserve grade. In the short term, the Company expects to continue processing at a grade higher than average mineral reserves grade, as reflected in the 2020 average feed grade of 2.36 g/t. These lower grade mineral reserves also provide opportunities for incremental lower-cost mill feed in excess of the planned throughput rates, in the event that the processing plant optimizations and expansions exceed targeted throughput rates. Measured and indicated mineral resources and inferred mineral resources both increased from year end 2019, with total gold mineral resources and mineral reserves increasing by 823,000 ounces. The continued mineral reserve and mineral resource growth establishes Jacobina as a multi-decade operation and supports the ongoing production growth trend towards 230,000 ounces of gold per year after the implementation of the Phase 2 expansion project. As a result of the exploration success, the Company is now considering further growth opportunities including a potential Phase 3 expansion to 10,000 tpd.

Jacobina Gold Mineral Reserves (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/c454ea0c-c2de-4314-8825-0a2203072603

(i) Additions from infill drilling and mine design optimization.

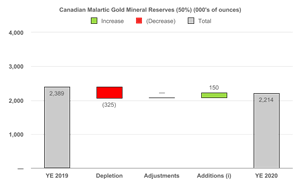

Canadian Malartic including Odyssey, Canada (50%)

At Canadian Malartic, an optimized design of the Barnat pit resulted in an increase in gold mineral reserves, which significantly reduced depletion resulting from production. On a 50% basis, while 325,000 ounces of mineral reserves were depleted through production, the optimized pit design resulted in an increase of approximately 150,000 ounces. This, combined with other small additions, resulted in net depletion of only 175,000 ounces. This allows for approximately half a year of additional mine life from the open pit operation. Underground inferred mineral resources at East Gouldie increased by 3.68 million ounces on a 100% basis as a result of the infill drilling program conducted throughout 2020, while the zone continues to expand at depth. On a 100% basis, the overall underground project has increased to more than 14,000,000 ounces of gold mineral resources, of which approximately 7,300,000 ounces are included in a Preliminary Economic Assessment completed in February 2021. The remaining mineral resources, together with the potential extension of East Gouldie at depth, represents further upside to extend mine life beyond 2040. Additional exploration in the underground project is planned for 2020, including the first drill holes from an underground drill bay off the exploration ramp which commenced in the fourth quarter of 2020.

Canadian Malartic Gold Mineral Reserves (50%) (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/a80eb164-2049-4cff-a0ca-5ee889755105

(i) Additions through pit design optimization.

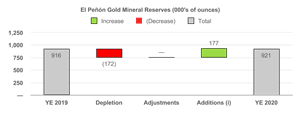

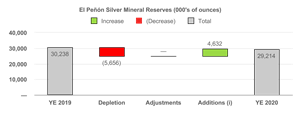

El Peñón, Chile

El Peñón's gold mineral reserves replaced 2020 depletion as the result of positive infill drilling. This is the third consecutive year that El Peñón gold mineral reserves have replaced depletion of mining, increasing from 764,000 ounces in year-end 2017 to 921,000 ounces in year-end 2020. Gold and silver measured and indicated mineral resources increased by 16% and 17% respectively, compared to the prior year, due to the positive infill drilling results, especially at La Paloma, Pampa Campamento, and Quebrada Colorada Sur, the latter of which is a new vein discovered in early 2020, converted to inferred and then indicated mineral resources throughout the year, and incorporated into the mine plan in 2021. Inferred gold mineral resources also increased by 16%, providing additional targets for infill drilling in 2021. A subset of these inferred mineral resources, subjected to the same economic and mining parameters as mineral reserves, are included in the Company’s 10-year production outlook for El Peñón. Although the average mineral resource grade is lower than mineral reserves grade, the subset of mineral resources included in the mine plan is of similar grades to mineral reserves. This process is demonstrated in the year-end mineral reserves, where the inferred mineral resources converted to mineral reserves in 2020 are higher than average reserves grade and the new inferred mineral resources added throughout the year are also higher than average grade. The ongoing exploration success and mineral reserves replacement at El Peñón continues to extend the mine life of the operation, which is entering its 22nd year of production, and unlocks opportunities for sustainable production growth with minimal capital investment.

El Peñón Gold Mineral Reserves (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/34ce6609-bea6-481c-a0cb-d9cdbcfa1189

El Peñón Silver Mineral Reserves (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/0d993d71-27ed-47c4-bd75-b4e085b18cfb

(i) Additions through infill drilling.

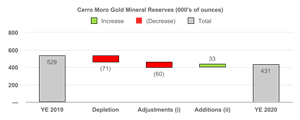

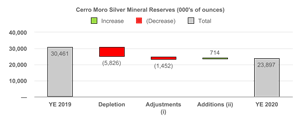

Cerro Moro, Argentina

At Cerro Moro, mineral reserves changed due to 2020 depletion and adjustments to the geological models, partly offset by new mineral reserves at Naty. The model adjustments, as an outcome of increased geological understanding gained from mining of the deposits, together with addition of new lower grade open pit mineral reserves, have resulted in a reduction of average mineral reserves grade. Higher grade intercepts at depth at Zoe and Escondida late in the year are not included in the year-end mineral reserves and mineral resources but will be followed up with drilling in 2021. Although COVID-19 related disruptions impacted the Company’s ability to add new inferred mineral resources in 2020, approximately 56,000 ounces of gold inferred mineral resources have been added as a potential heap leach inventory. Promising metallurgical testing results and conceptual level engineering completed in 2020 demonstrate the potential for a parallel heap leach operation to provide supplementary production to the existing plant and provides a lower cost processing alternative to reduce cut-off grade and convert the expanding inventory of lower grade mineralization that is sub-economic at the current mineral reserves parameters. Drilling will follow up on heap leach targets in 2021 with an objective to build inferred mineral resources.

Cerro Moro Gold Mineral Reserves (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/fba6d0a1-ddf5-4863-941b-29244afeb675

Cerro Moro Silver Mineral Reserves (000's of ounces)

A chart accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/875f0e97-64e1-4f7b-8c17-7bff3c54561e

(i) Adjustments to block models.

(ii) Additions through drilling.

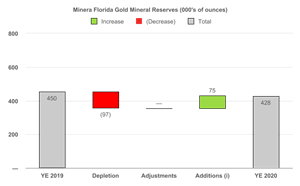

Minera Florida, Chile

At Minera Florida, mineral reserves changed due to depletion from mining, partially offset by additions as a result of positive drilling results at Pataguas and Don Leopoldo. Indicated and inferred mineral resources increased by 30,000 ounces and 9,000 ounces of gold respectively. Due to COVID-19 impacts, drilling of several zones that was planned for earlier in the year was postponed to the fourth quarter and is therefore not included in the year-end mineral resource and mineral reserves statements.

Minera Florida Gold Mineral Reserves (000's of ounces)

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/35f86b1f-a1e9-4ec7-a786-48170095a770

(i) Additions due to infill drilling.

KEY STATISTICS

Key operating and financial statistics for the fourth quarter and full year 2020 are outlined in the following tables.

Financial Summary

| (In millions of United States Dollars, except for per share and per unit amounts) | Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Revenue | $ | 461.8 | $ | 383.8 | $ | 1,561.0 | $ | 1,612.2 | ||||||||

| Cost of sales excluding depletion, depreciation and amortization | (166.8 | ) | (169.4 | ) | (614.1 | ) | (782.8 | ) | ||||||||

| Depletion, depreciation and amortization | (112.5 | ) | (119.0 | ) | (395.0 | ) | (471.7 | ) | ||||||||

| Total cost of sales | (279.3 | ) | (288.4 | ) | (1009.1 | ) | (1254.5 | ) | ||||||||

| Net reversal of impairment of mining properties | 191.0 | — | 191.0 | — | ||||||||||||

| Temporary suspension, standby and other incremental COVID-19 costs | (9.2 | ) | — | (40.5 | ) | — | ||||||||||

| Mine operating earnings | 364.3 | 95.4 | 702.4 | 357.7 | ||||||||||||

| General and administrative expenses | (23.4 | ) | (19.3 | ) | (85.9 | ) | (79.4 | ) | ||||||||

| Exploration and evaluation expenses | (6.0 | ) | (3.3 | ) | (15.1 | ) | (10.3 | ) | ||||||||

| Net earnings | 103.0 | 14.6 | 203.6 | 225.6 | ||||||||||||

| Net earnings per share - basic and diluted (i) | 0.11 | 0.02 | 0.21 | 0.24 | ||||||||||||

| Cash flow generated from operations after changes in non-cash working capital | 181.5 | 201.7 | 617.8 | 521.8 | ||||||||||||

| Cash flow from operations before changes in non-cash working capital (ii) | 207.4 | 176.6 | 688.7 | 590.5 | ||||||||||||

| Revenue per ounce of gold | 1,875 | 1,486 | 1,777 | 1,392 | ||||||||||||

| Revenue per ounce of silver | 24.02 | 17.55 | 21.11 | 16.39 | ||||||||||||

| Average realized gold price per ounce | $ | 1,875 | $ | 1,484 | $ | 1,777 | $ | 1,387 | ||||||||

| Average realized silver price per ounce | $ | 24.02 | $ | 17.50 | $ | 20.93 | $ | 16.26 | ||||||||

(i) For the three months and year ended December 31, 2020, the weighted average number of shares outstanding was 952,435 thousand (basic) and 954,565 thousand (diluted), and 951,818 thousand (basic) and 953,846 thousand (diluted), respectively.

(ii) Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion included at the end of this press release under the heading “Non-GAAP Financial Measures and Additional Line Items and Subtotals in Financial Statements”. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q42020 and in Section 12 of the Company’s Management’s Discussion & Analysis for the year ended December 31, 2020, which is available on the Company's website and on SEDAR.

Production, Financial and Operating Summary

| Costs | Three Months Ended December 31 | Year Ended December 31, | ||||||||||

| (In United States Dollars) | 2020 | 2019 | 2020 | 2019 | ||||||||

| Per GEO sold (1) | ||||||||||||

| Total cost of sales | $ | 1,131 | $ | 1,117 | $ | 1,151 | $ | 1,143 | ||||

| Cash Costs (2) | $ | 675 | $ | 656 | $ | 701 | $ | 679 | ||||

| AISC (2) | $ | 1,076 | $ | 1,011 | $ | 1,080 | $ | 999 | ||||

| Three Months Ended December 31 | Year Ended December 31, | |||||||||||

| Gold Ounces | 2020 | 2019 | 2020 | 2019 | ||||||||

| Canadian Malartic (50%) (3) | 86,371 | 85,042 | 284,317 | 334,596 | ||||||||

| Jacobina | 44,165 | 41,774 | 177,830 | 159,499 | ||||||||

| Cerro Moro | 21,259 | 26,568 | 66,995 | 120,802 | ||||||||

| El Peñón | 43,512 | 48,131 | 160,824 | 159,515 | ||||||||

| Minera Florida | 26,352 | 20,080 | 89,843 | 73,617 | ||||||||

| TOTAL | 221,659 | 221,595 | 779,809 | 848,029 | ||||||||

| Three Months Ended December 31 | Year Ended December 31, | |||||||

| Silver Ounces | 2020 | 2019 | 2020 | 2019 | ||||

| Cerro Moro | 1,663,708 | 1,584,904 | 5,448,561 | 6,322,864 | ||||

| El Peñón | 922,954 | 1,382,963 | 4,917,101 | 4,317,292 | ||||

| TOTAL | 2,586,662 | 2,967,867 | 10,365,662 | 10,640,156 | ||||

For a full discussion of Yamana’s operational and financial results and mineral reserve and mineral resource estimates, please refer to the Company’s Management’s Discussion & Analysis and Consolidated Financial Statements for the year ended December 31, 2020, which are available on the Company's website at www.yamana.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

MINERAL RESERVE AND MINERAL RESOURCE ESTIMATES

Mineral Reserves (Proven and Probable)

The following table sets forth the Mineral Reserve estimates for the Company’s mineral projects as at December 31, 2020.

| Gold | Proven Mineral Reserves | Probable Mineral Reserves | Total - Proven & Probable | |||||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | ||||||||||

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | ||||||||||

| Canadian Malartic, Barnat & Other Zones (50%) | 25,370 | 0.85 | 696 | 36,068 | 1.31 | 1,518 | 61,438 | 1.12 | 2,214 | |||||||||

| Canadian Malartic Underground (50%) | — | — | — | — | — | — | — | — | — | |||||||||

| Canadian Malartic (50%) | 25,370 | 0.85 | 696 | 36,068 | 1.31 | 1,518 | 61,438 | 1.12 | 2,214 | |||||||||

| Jacobina | 28,821 | 2.16 | 2,004 | 11,277 | 2.22 | 804 | 40,098 | 2.18 | 2,807 | |||||||||

| Cerro Moro | 328 | 6.58 | 69 | 1,338 | 8.40 | 361 | 1,666 | 8.04 | 431 | |||||||||

| El Peñón Ore | 368 | 5.73 | 68 | 5,121 | 5.02 | 827 | 5,489 | 5.07 | 895 | |||||||||

| El Peñón Stockpiles | 9 | 1.40 | — | 651 | 1.26 | 26 | 660 | 1.26 | 27 | |||||||||

| El Peñón Total | 377 | 5.63 | 68 | 5,772 | 4.60 | 853 | 6,149 | 4.66 | 921 | |||||||||

| Minera Florida Ore | 1,215 | 3.60 | 141 | 2,104 | 3.70 | 250 | 3,319 | 3.66 | 391 | |||||||||

| Minera Florida Tailings | — | — | — | 1,248 | 0.94 | 38 | 1,248 | 0.94 | 38 | |||||||||

| Minera Florida Total | 1,215 | 3.60 | 141 | 3,352 | 2.67 | 288 | 4,567 | 2.92 | 428 | |||||||||

| Yamana Operations Gold Mineral Reserves | 56,112 | 1.65 | 2,978 | 57,807 | 2.06 | 3,824 | 113,918 | 1.86 | 6,802 | |||||||||

| Jeronimo (57%) | 6,350 | 3.91 | 798 | 2,331 | 3.79 | 284 | 8,681 | 3.88 | 1,082 | |||||||||

| MARA Project (56.25%) | 330,300 | 0.25 | 2,655 | 291,150 | 0.16 | 1,498 | 621,450 | 0.21 | 4,152 | |||||||||

| Wasamac | 1,028 | 2.66 | 88 | 20,427 | 2.56 | 1,679 | 21,455 | 2.56 | 1,767 | |||||||||

| Total Gold Mineral Reserves | 393,790 | 0.51 | 6,519 | 371,715 | 0.61 | 7,285 | 765,505 | 0.56 | 13,803 | |||||||||

| Silver | Proven Mineral Reserves | Probable Mineral Reserves | Total - Proven & Probable | |||||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | ||||||||||

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | ||||||||||

| Cerro Moro | 328 | 390.0 | 4,109 | 1,338 | 460.0 | 19,788 | 1,666 | 446.3 | 23,897 | |||||||||

| El Peñón Ore | 368 | 213.4 | 2,526 | 5,121 | 160.2 | 26,378 | 5,489 | 163.8 | 28,904 | |||||||||

| El Peñón Stockpiles | 9 | 54.1 | 16 | 651 | 14.1 | 294 | 660 | 14.6 | 310 | |||||||||

| El Peñón Total | 377 | 209.5 | 2,542 | 5,772 | 143.7 | 26,672 | 6,149 | 147.8 | 29,214 | |||||||||

| Minera Florida Ore | 1,215 | 23.4 | 915 | 2,104 | 21.9 | 1,481 | 3,319 | 22.4 | 2,396 | |||||||||

| Minera Florida Tailings | — | — | — | 1,248 | 14.5 | 584 | 1,248 | 14.5 | 584 | |||||||||

| Minera Florida Total | 1,215 | 23.4 | 915 | 3,352 | 19.2 | 2,065 | 4,567 | 20.3 | 2,979 | |||||||||

| Yamana Operations Silver Mineral Reserves | 1,921 | 122.5 | 7,566 | 10,461 | 144.3 | 48,525 | 12,382 | 140.9 | 56,091 | |||||||||

| MARA Project (56.25%) | 330,300 | 3.0 | 32,070 | 291,150 | 2.6 | 24,618 | 621,450 | 2.8 | 56,689 | |||||||||

| Total Silver Mineral Reserves | 332,221 | 3.7 | 39,636 | 301,611 | 7.5 | 73,143 | 633,832 | 5.5 | 112,780 | |||||||||

| Copper | Proven Mineral Reserves | Probable Mineral Reserves | Total - Proven & Probable | ||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | |||||||

| (000's) | (% ) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | |||||||

| MARA Project (56.25%) | 330,300 | 0.57 | 4,151 | 291,150 | 0.39 | 2,503 | 621,450 | 0.49 | 6,654 | ||||||

| Total Copper Mineral Reserves | 330,300 | 0.57 | 4,151 | 291,150 | 0.39 | 2,503 | 621,450 | 0.49 | 6,654 | ||||||

| Zinc | Proven Mineral Reserves | Probable Mineral Reserves | Total - Proven & Probable | |||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | ||||||||

| (000's) | (% ) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | ||||||||

| Minera Florida Ore | 1,215 | 1.22 | 33 | 2,104 | 1.17 | 54 | 3,319 | 1.19 | 87 | |||||||

| Minera Florida Tailings | — | — | — | 1,248 | 0.58 | 16 | 1,248 | 0.58 | 16 | |||||||

| Minera Florida Total | 1,215 | 1.22 | 33 | 3,352 | 0.95 | 70 | 4,567 | 1.02 | 103 | |||||||

| Total Zinc Mineral Reserves | 1,215 | 1.22 | 33 | 3,352 | 0.95 | 70 | 4,567 | 1.02 | 103 | |||||||

| Molybdenum | Proven Mineral Reserves | Probable Mineral Reserves | Total - Proven & Probable | ||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | |||||||

| (000's) | (% ) | lbs (mm) | (000's) | (%) | lbs (mm) | (000's) | (%) | lbs (mm) | |||||||

| MARA Project (56.25%) | 330,300 | 0.030 | 218 | 291,150 | 0.030 | 192 | 621,450 | 0.030 | 411 | ||||||

| Total Molybdenum Mineral Reserves | 330,300 | 0.030 | 218 | 291,150 | 0.030 | 192 | 621,450 | 0.030 | 411 | ||||||

Mineral Resources (Measured, Indicated, and Inferred)

The following tables set forth the Mineral Resource estimates for the Company’s mineral projects as at December 31, 2020.

| Gold | Measured Mineral Resources | Indicated Mineral Resources | Total - Measured & Indicated | |||||||||||||||

| Tonnes | Grade | Contained | Tonnes | Grade | Contained | Tonnes | Grade | Contained | ||||||||||

| (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | (000's) | (g/t) | oz. (000's) | ||||||||||

| Canadian Malartic, Barnat & Other Zones (50%) | 149 | 0.55 | 3 | 2,566 | 1.24 | 103 | 2,715 | 1.21 | 105 | |||||||||

| Odyssey Underground (50%) | — | — | — | 1,000 | 1.90 | 61 | 1,000 | 1.90 | 61 | |||||||||

| East Malartic Underground (50%) | — | — | — | 5,658 | 2.03 | 368 | 5,658 | 2.03 | 368 | |||||||||

| East Gouldie Underground (50%) | — | — | — | — | — | — | — | — | — | |||||||||

| Canadian Malartic Total (50%) | 149 | 0.55 | 3 | 9,225 | 1.79 | 532 | 9,373 | 1.77 | 535 | |||||||||

| Jacobina | 28,777 | 2.44 | 2,257 | 17,070 | 2.29 | 1,257 | 45,847 | 2.38 | 3,514 | |||||||||

| Cerro Moro | 77 | 5.22 | 13 | 647 | 3.70 | 77 | 725 | 3.86 | 90 | |||||||||

| El Peñón Mine | 667 | 4.81 | 103 | 6,355 | 3.06 | 625 | 7,022 | 3.22 | 728 | |||||||||

| El Peñón Tailings | — | — | — | — | — | — | — | — | — | |||||||||

| El Peñón Stockpiles | — | — | — | 1,019 | 1.13 | 37 | 1,019 | 1.13 | 37 | |||||||||