2 Signs We're in a '90s Throwback Market

"One of the world's largest money managers says you should fear the lack of fear in markets. ...Pacific Investment Management Co. says now is the time for caution." (Jan. 17)

"Recent 'Odd' Market Moves May Be a Warning Sign for Stocks" (Jan. 21)

"Slowing Cash Flow Could Mean a 'Nasty Surprise' for U.S. Stocks" (Jan. 23)

"U.S. stocks are set for a correction of 5% or more this year after the longest stretch in history without one, said Bob Doll, chief equity strategist at $172 billion Nuveen Asset Management." (Jan. 23)

"Warning signs points to coming reversal, pain for popular trade... Canaccord Genuity Inc.'s Tony Dwyer noted a peak in the Citigroup Economic Surprise Index of forecast-beating data and a low in the Federal Reserve's Monetary Policy Uncertainty Index -- two points that historically precede incoming volatility and a reversal in investors' optimistic views." (Jan. 23)

"U.S. Stock Rally Sparks Longest 'Overbought' Streak in 21 Years" (Jan. 25)

"Biggest Stock Sell Signal Since 2013 Sparked by Record Inflows" (Jan. 26)

-- Bloomberg

"Trump's Trade Policies Could Spell Trouble for Stocks" (Jan. 26)

-- The Wall Street Journal

However, when analyzing the broad stock market, an individual equity, or other asset class, it is a mistake to use a price chart to assess the sentiment backdrop. You likely know where I'm going with this from the excerpts above, as I have been floored by the amount of caution that strategists have voiced coincident with the market powering higher this month.

Throughout the bull market, we have seen worries that range from fundamental (weak top-line earnings growth, and more recently, stretched valuations), to monetary (Fed policy -- interest rates, quantitative easing, and the unwinding of quantitative easing), to political (the election of Donald Trump), to geopolitical (Greece, Brexit, North Korea, terrorism), to technical (technicians tend to see the risk in a bearish "head and shoulders" pattern and are blind to the development of the reward in a bullish inverse head and shoulders pattern). Moreover, persistently low volatility has been a concern for months.

Might the latest worries expressed by money managers and strategists be those that we should pay attention to? Time will tell, but for now, the market is not confirming such fears. In other words, despite a litany of well-advertised concerns, the market continues to achieve record highs.

A summary of the "advertised" current risks remains long: a flattening yield curve; diminishing corporate cash flows; an incoming new Fed chair and shifting central bank policies; a peak in the number of positive surprises relative to expectations in economic data releases; fears of a potential flare-up in inflation; Trump's trade policies; a long "overbought" market; volatility (as measured by the CBOE Volatility Index) rising as the market rises; and fear that optimism has hit an extreme, setting the market up for a fall.

Short interest on $SPX components rose a sharp 5.9% in the first two weeks of '18.. SPX climbed 4.2% in the same period.. #ShortCoveringFuelRemains

- Todd Salamone (@toddsalamone) January 25, 2018The broad range of concerns suggests it's likely that the euphoria typically seen at market tops has not yet set in, and therefore, buying power remains. In fact, when the short interest data from mid-January was released last week, I was astonished to learn that SPX component short interest, or bets against each individual company's stock price, rose nearly 6% in the two-week period from the end of December. What I speculated last week may have been a short-covering rally to begin the year proved to be a rally against the headwinds of a short interest build. Given the SPX's price action in the second half of January, it is likely that many of these new short positions are already underwater.

As I said at the beginning of this commentary, there has indeed been an unwinding of extreme fear that has been supportive of stock prices, but it's doubtful that we're in the kind of euphoric stage that is typically coincident with a major market top. If you use the SPX component short interest chart since 2007 as a gauge of fear and optimism, note that on one hand, total short interest is 24% below its 2008 high -- but it's also 30% above its April 2012 low. For what it's worth, the April 2012 short interest low preceded a near-10% correction in the SPX and this metric's peak for the calendar year.Another interesting statistic as it pertains to the present is that the SPX is up 25% year-over-year, while SPX component short interest is up 13% from its 2017 low (set in February). In other words, there is more short-covering potential at present relative to this time last year, despite the market hitting new all-time highs last week.

After reading some of the current concerns being expressed by strategists last week, I couldn't help but think about the mid-1990s environment as it relates to the market's momentum and VIX/SPX interplay.

For example, one strategist mentioned that the market is vulnerable because of "odd" action in the CBOE Volatility index (VIX - 11.08), as it's been rising with stock prices (the VIX was up 33% from its Jan. 4 low to its Jan. 18 closing high). Typically, as the analyst suggested, the VIX will decline as stocks move higher, and spike when stocks move sharply lower.

But note that in 1995 a comparable disconnect occurred, as the VIX was similarly low and there were short-term periods in which the SPX and VIX rose simultaneously. The takeaway is that such "odd" behavior in the VIX was not a warning flag in 1995 and, if anything, proved to be a green light for stocks.

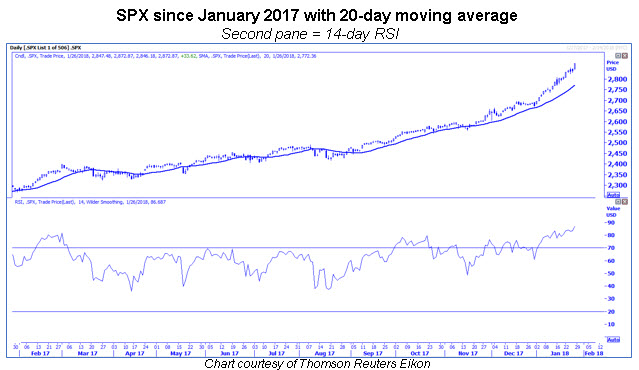

Another headline that took me back to the mid-1990s was the one describing the longest overbought streak in 21 years. On Friday, the SPX's 14-day Relative Strength Index (RSI) was above 70 for the 17th straight day. According to the Bloomberg article, the last time the index had an "overbought" streak like this was 18 days in November-December 1996.

A 15-day RSI streak above 70 occurred in February-March 2017, and after this indicator moved back below 70 on March 6, the SPX declined 2% over the next month. According to our data, another meaningful 15-day consecutive streak above 70 occurred last October. However, the ensuing RSI move back below 70 simply preceded three weeks of "flattish" action before the SPX renewed its uptrend.

This overbought streak may be worth watching in the days ahead, as a near 4% pullback occurred after the 1996 RSI streak above 70 ended after 18 days. This short-term pullback was around the same time that then-presiding Fed Chair Alan Greenspan uttered "irrational exuberance" in a speech. If you are using the 14-day RSI as an indicator to time a short-term pullback, it is perhaps best to await confirmation of an RSI move back below 70, at risk of fighting a runaway freight train.

Long-term investors should stay the bullish course, and short-term traders should continue to use calls to leverage the upside and manage risk in this "overbought" environment.

Continue reading:

Indicator of the Week: Why Stocks Could Rally 20% in 2018The Week Ahead: FAANG Earnings, Fed, and Payrolls Highlight Packed Week