Gold Weekly: Overlooked. Until When?

Gold witnessed only moderate upward pressure despite the recent equity rout.

Speculators slightly lifted net long positions in Comex gold in the week to October 23, the CFTC shows.

ETF investors bought just a small quantity of gold last week, according to Fastmarkets.

For now, investors are not overly worried about the "technical" sell-off in US equities. As such, the dollar acts as the ideal safe-haven asset.

I expect this narrative to change from 2019, which could lead gold to be viewed as the "ultimate hedge".

Overlooked sculpture, Daniel Johanning (Saatchi art)

Introduction

Welcome to my Gold Weekly.

In this report, I discuss mainly my views about the gold market through the GraniteShares Gold Trust ETF (BAR). BAR is directly impacted by the vagaries of gold spot prices because the fund physically holds gold bars in a London vault in the custody of ICBC Standard Bank.

To do so, I analyse the recent changes in speculative positions on the Comex (based on the CFTC) and ETF holdings (based on FastMarkets' estimates) in a bid to draw some interpretations about investor and speculator behavior. Then, I discuss my global macro view and the implications for monetary demand for gold. I conclude the report by sharing my trading positioning.

Speculative positions on the Comex

CFTC statistics are public and free. The CFTC publishes its Commitment of Traders report (COTR) every Friday, which covers data from the week ending the previous Tuesday. In this COTR, I analyze the speculative positioning; that is, the positions held by the speculative community, called "non-commercials" in the legacy COTR, which tracks data from 1986.

It is important to note that the changes in speculative positioning in gold futures contracts do not involve physical flows because it is very uncommon for speculators to take delivery on the futures contracts that they trade. Due to the use of leverage by speculators, the changes in speculative positions in gold futures contracts tend to be much greater than the changes in other components of gold demand like ETFs or jewellery.

As a result, the impact on gold spot prices tends to be relatively more important and volatile, which in turn affect the value of BAR because it physically holds the metal in vaults in London and therefore has a direct exposure to spot gold prices.

Gold ETF positions

The data about gold ETF holdings are from FastMarkets, an independent metals agency which tracks ETF holdings across the precious metals complex. FastMarkets tracks on a daily basis a total of 21 gold ETFs, which represent the majority of total gold ETF holdings. The largest gold ETFs tracked by FastMarkets are the SPDR (R) Gold Shares (NYSEARCA:GLD), whose holdings represent nearly 40% of total gold ETF holdings, and the iShares Gold Trust (IAU), whose holdings represent roughly 15% of total gold ETF holdings.

Speculative positioning

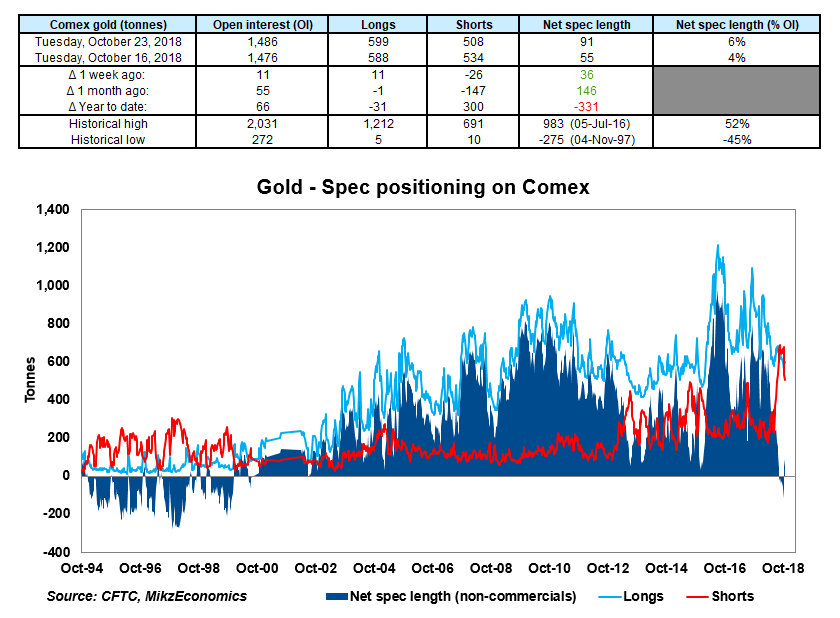

Source: CFTC

According to the latest Commitment of Traders report (COTR) provided by the CFTC, non-commercials were net Comex gold to the tune of 91 tonnes as of October 23, marking a second straight week of net long exposure to Comex gold.

Over the latest reporting period of October 16-23, non-commercials lifted their net long positions by 36 tonnes, reflecting some short-covering (26 tonnes) and long accumulation (11 tonnes).

The excessively negative spec positioning in Comex gold seems behind us. However, net long speculative positions in Comex gold remain extremely low by historical standards.

Accordingly, I expect the speculative community to assert more upside exposure to Comex gold in the coming weeks and months, barring a considerably negative macro backdrop where the dollar, US real rates, and US equities would move to the roof in symbiosis.

Bottom line: the spec normalization in the gold futures market has started since Q4-start. I expect substantial speculative buying in favour of Comex gold by year-end, which would produce a considerable increase in Comex spot gold prices, which in turn would lift significantly the value of GraniteShares Gold Trust ETF (BAR) higher.

Investment positioning

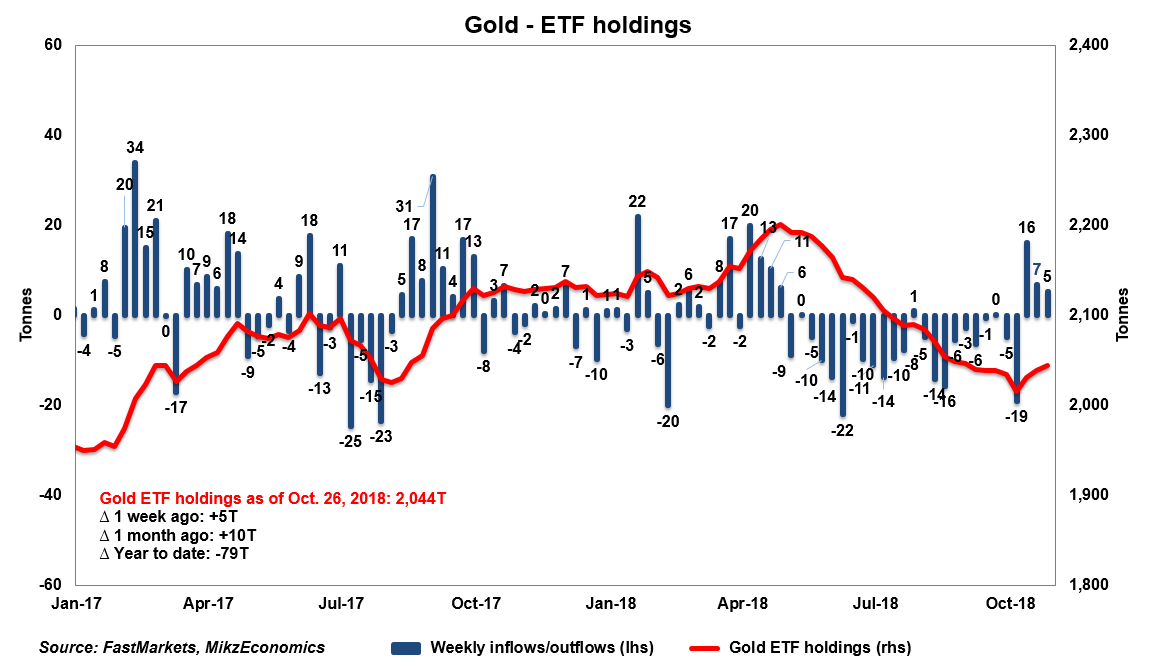

Source: FastMarkets

ETF investors held around 2,044 tonnes of gold across various ETFs as of October 26, according to Fastmarkets. Gold holdings held by ETF investors have rebounded by nearly 30 tonnes from mid-October lows.

Over the latest reporting period of October 19-25, ETF investors lifted by roughly 5 tonnes their gold holdings, marking a third straight week of inflows.

The pace of gold ETF inflows since the start of October is surprisingly small in light of the global equity rout. US equities (S&P 500: -4% w/w, -8% mtd) are on track to record their strongest monthly sell-off since February 2009. However, gold ETF holdings have increased by only 10 tonnes since the start of the month, a marginal increase of 0.5%.

In contrast, during the equity rout of February 2009, gold ETF holdings jumped by 233 tonnes or 18% during the month.

In February 2009, investors were in panic and ergo, rushed to gold because gold is often viewed as the "ultimate hedge" after everything collapses. Gold was the only place to hide. This year, it seems to me that investors are aware that the current equity sell-off is purely technical and as such, there is no need to panic and other assets (like the dollar) are preferred as haven.

Will the narrative change? Probably not in the immediate term but it will probably in the course of 2019. The Fed is fixated on the idea that the Fed funds rate needs to increase in the coming quarters as a result of robust macro data. But it is clear that investors increasingly struggle to adapt to the new environment in which US yields rise at an aggressive pace.

A deeper sell-off in US equities and dollar sell-off caused by the ballooning deficit could emerge at some point next year, which would change materially investor mood and induce market participants to see gold as the "ultimate hedge", such as what happened in the first half of 2009.

Bottom line: While I expect ETF investors to remain quiet in the near term as the dollar acts presently as the ideal hedge, the narrative is likely to change in 2019, which could lead to more substantial gold ETF inflows.

Trading positioning

To play a likely rally in spot gold prices, I have a long position in the GraniteShares Gold Trust ETF (NYSEARCA: BAR).

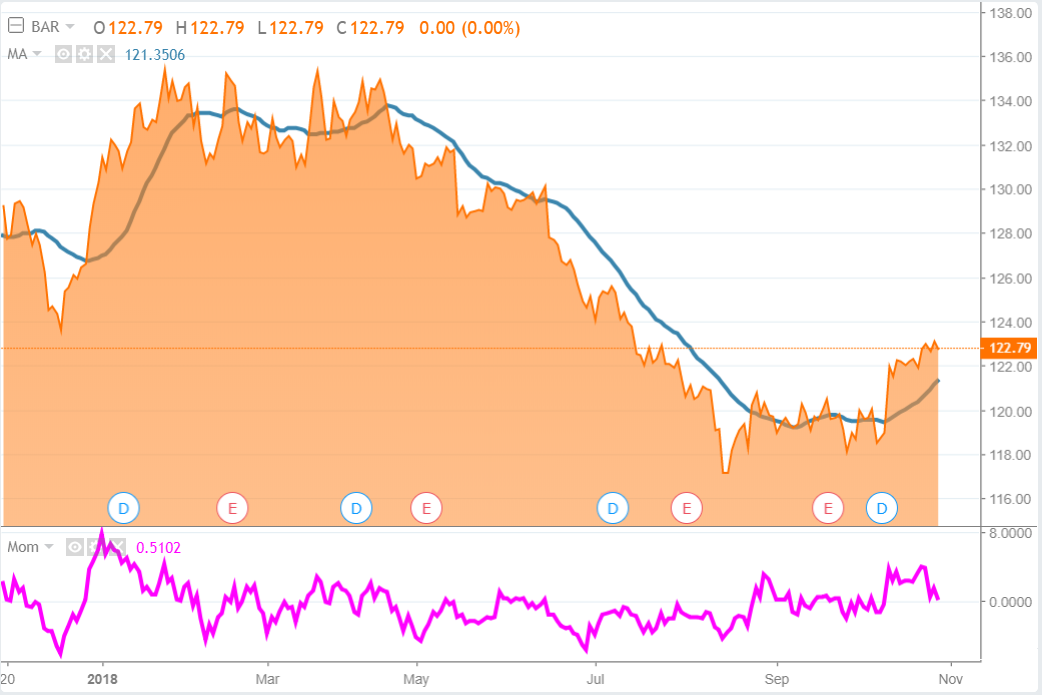

I took a long position in BAR on May 7, 2018 at $131.20, with a maximum risk of 3% of my Fund. With BAR currently trading at roughly $123 per share, my position is showing a loss. Still, I remain confident that it will ultimately show a profit because the macro backdrop is set to turn increasingly positive for the yellow metal.

Source: Seeking Alpha

From a technical vantage point, BAR is trading above its 20 daily moving average and the momentum indicator is in positive territory, thereby reflecting a bright sentiment.

I continue to believe that the 2018 low is behind us and that BAR will further appreciate in the months ahead.

BAR - GraniteShares - Review

BAR is directly impacted by the vagaries of gold spot prices because the Funds physically holds gold bars in a London vault and custodied by ICBC Standard Bank. The investment objective of the Fund is to replicate the performance of the price of gold, less trust expenses (0.20%), according to BAR's prospectus.

The physically-backed methodology prevents investors from getting hurt by the contango structure of the gold market, contrary to ETFs using futures contracts.

Also, the structure of a grantor trust protects investors since trustees cannot lend the gold bars.

BAR provides exposure which is identical to established competitors like GLD and IAU, which are nevertheless much more costly to hold over a long period of time. Indeed, BAR offers an expense ratio of just 0.20% while GLD and IAU have an expense ratio of 0.25% and 0.50%, respectively.

As of October 26, BAR traded at a slight premium of $0.03 per share or 0.02% to its net asset value, which has occurred around 25% of the time (in term of number of days) since its inception. This compares with a premium of $0.01 per share a week ago. I expect any deviation from the net asset value to narrow on the back of arbitrage opportunities.

BAR's average spread (over the past 60 trading days) is 0.02%, which is lower than that of its competitor IAU, at 0.09%, or SPDR Gold MiniShares Trust (GLDM), at 0.08%.

As a result, BAR offers the lowest total cost of ownership (expense ratio + spread) among gold ETFs.

BAR's average daily volume (over the past 45 trading days) is ~$2 million, which is much lower than that of IAU, at ~$126 million.

As of October 26, 2018, BAR's assets under management totalled $290 million, with 2.4 million shares. BAR's gold holdings were at 7.32 tonnes. In contrast, IAU's assets under management amounted to $10.295 billion, with 983.5 million shares. IAU's gold holdings were at around 270 tonnes.

For the sake of transparency, I will update my trading activity on my Twitter account.

Final note

Dear friends, if you enjoy reading my research, thank you for showing support by clicking the "Follow" button on the top of the page and sharing/liking/commenting this article. I look forward to reading your comments below and debating constructively on the gold market.

![]()

ETFs: GLD, GDX, NUGT, GDXJ, JNUG, GGN, DUST, IAU, PHYS, JDST, SGOL, JJC, GOEX, UGLD, SGDM, UGL, DGP, GLL, ASA, GTU, GLDI, OUNZ, RING, DZZ, SGDJ, DGL, DGLD, TGLDX, DGZ, CPER, PSAU, GOAU, GDXX, GYEN, BAR, GEUR, GDXS, GLDW, GHS, CUPM, UBG, QGLDX, GHE, MELT, IAUF

Disclosure: I am/we are long BAR.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Follow Boris Mikanikrezai and get email alerts