B2Gold: Fekola Mine Seems To Be Firing On All Cylinders

BTG has delivered strong financial and operational performance during Q3.

Analysts' opinion and the technical chart also suggest more upside to the stock.

A positive development in the Fekola mine indicates a potential increase in shareholder value.

Increased FCFs are a support for the expansion of other mining properties.

Thesis:

During Q3 2018, B2Gold Corporation (BTG) reported revenue of ~$324 MM and EPS of $0.05 in line with guidance. BTG's Q4 revenue witnessed a healthy ~110% increase Y/Y. On the operational side, the company reported record production of ~242 Koz (read: thousands of ounces) of gold that was ~78% in excess of the gold production reported in Q3 2017. These favourable numbers indicate that BTG is on track to improve its financial and operational performance in the coming quarters.

Figure-1 (Source: FinancialsTrend)

Figure-1 (Source: FinancialsTrend)

In this article, I have briefly discussed the operational and financial performance during Q3 and the significant developments on BTG's major mining operations. The article discusses the resource potential of BTG's recently acquired flagship asset in Mali, namely the FM (read: Fekola mine). The FM has surprised us in terms of exploration results, gold production, and low-cost mining. With support from gold prices and positive production results from BTG's other mining assets, I see a great opportunity for BTG to witness share price growth, going forward.

Financial and operational performance at a glance:

During Q3, revenue stood at $324 MM (Q3 2017: $154 MM) from the sale of ~269,000 oz of gold (Q3 2017: 122,000 oz). The company produced ~242,000 oz and had to sell some of its existing gold inventories to pay the convertible notes on October 1st. The sales were partially affected by a decline in the average price of gold. In Q3 2018, BTG realized an average price of ~$1,206/oz of gold that was substantially lower than the average price realized in Q3 2017 (~$1,267/oz).

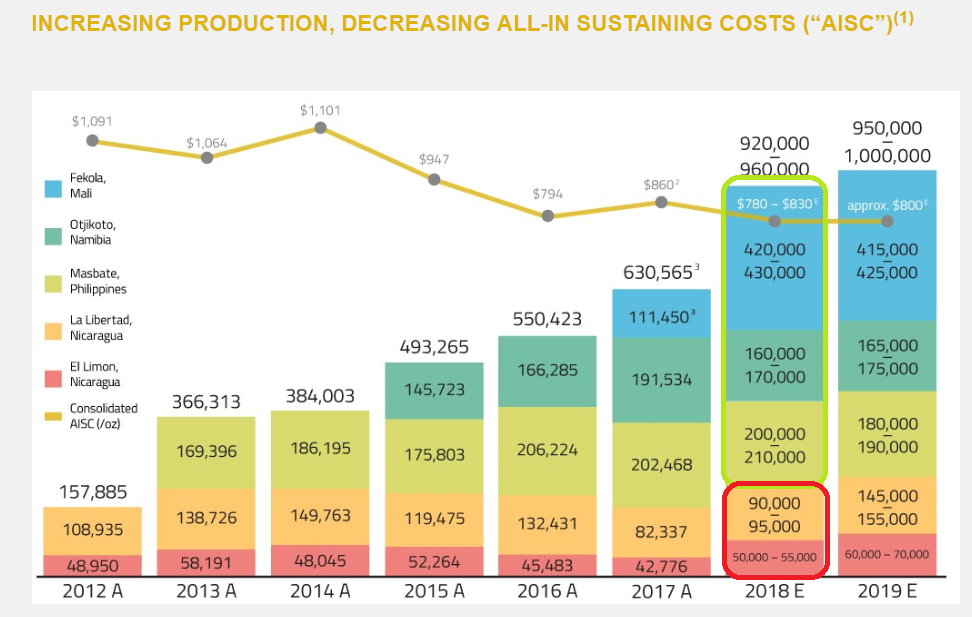

However, due to low-cost production from the FM (at ~$383/oz in cash costs), BTG has managed to reduce its AISC (read: All-In-Sustaining Cost) to a range of $780-830/oz and is inclined to bring it down towards the lower end of that range. Going forward, BTG is expected to bring down its AISC within the range of ~$800/oz in FY 2019 (Figure-2).

Figure-2 (Source: B2Gold-Investor Highlights)

Figure-2 (Source: B2Gold-Investor Highlights)

The strong production has helped transform the company's liquidity position. The company's cash from operations is estimated to be ~$450 MM by the end of FY 2018 (FY 2017: ~$155 MM). The strong liquidity will support BTG's exploration activities in the FM and will also support the company's other evaluation and exploration projects in Namibia, Burkina Faso, Columbia and Finland.

[Note: FM is a producing mine and it should not be confused with other exploration projects in the above-mentioned countries].

Out of the five producing mines in BTG's portfolio, the top 3 (encircled in green in Figure-2) are doing well with significant production potential. In contrast, BTG's mining operations in Nicaragua are partially affected by the unstable political situation in the country, and disruption in supply lines. Consequently, BTG suffers in terms of lower-than-budgeted production in these mines, at a cost that is higher than the budget. However, as shown in Figure-2, the annual production guidance from the Nicaraguan mines only accounts for ~16% of the total annual production guidance. Therefore, the impact of the problems in Nicaraguan operations is offset by the strong operating results from the FM (discussed in detail in a later section).

Technical analysis and analyst recommendation:

The technical price chart of BTG (Figure-3) indicates that the rally will continue for some time. Furthermore, the share has a 52-week range between $2.10 and $3.30, and we can see that the share lies near the midpoint of that range. Since the company has strong fundamentals and therefore attracts investor confidence, I believe these factors should also keep the momentum going.

Figure-3 (Source: Finviz)

Moreover, when we consider analysts' recommendations on this stock (Figure-4), we can see it rated as a 'buy' with a target price of ~$3.8 (?,?3.400 X $1.14/?,?).

Figure-4 (Source: Sharewise)

Figure-4 (Source: Sharewise)

A positive development in the FM indicates a potential increase in shareholder value:

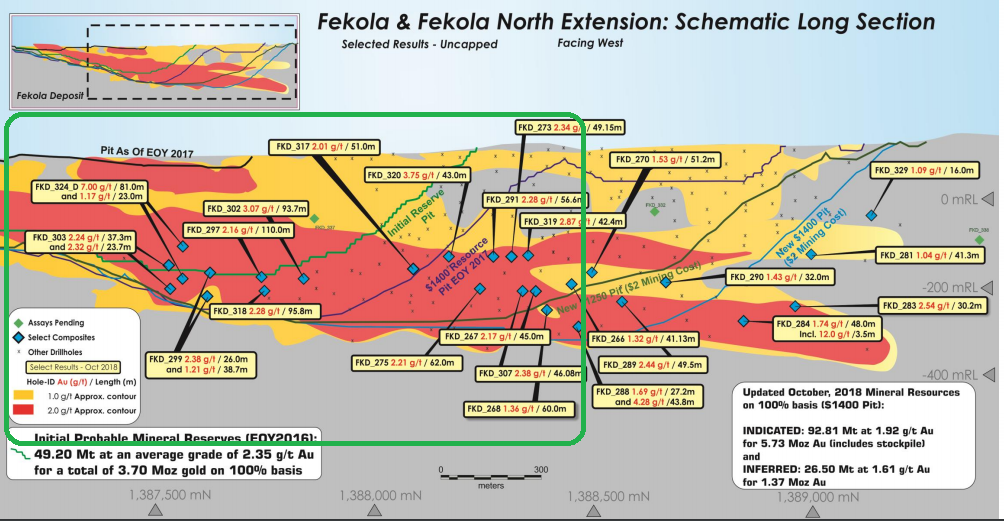

BTG's exploration drilling activities at the FM has yielded positive results and the company has updated the resource estimate. The updated Indicated resource is estimated at ~92.81 Mt at an average grade of ~1.92 g/t (which means resource potential of ~5.73 Moz of gold). Similarly, the Inferred resource is estimated at ~26.5 Mt at an average grade of ~1.61 g/t (which means resource potential of ~1.37 Moz of gold).

It should be noted that these updated gold resources are located towards the northern end of the Fekola mine as shown in Figure-5, and there is potential for further upward revision in the resource estimate, based on the results of additional drilling activity in the mine.

Figure-5 (Source: November Presentation)

Figure-5 (Source: November Presentation)

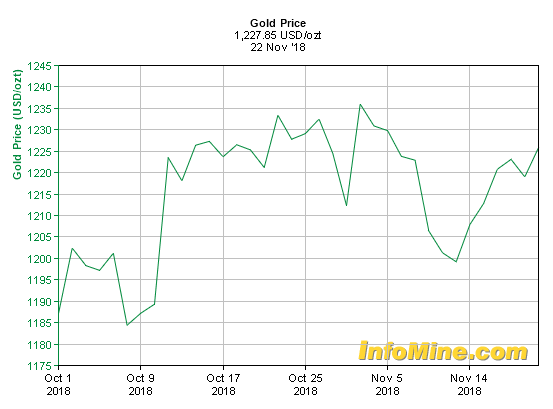

Gold prices: In deriving the above resource estimates, BTG has assumed a long-term gold price of ~$1,400/oz and this looks like an unreasonable price in the current gold market when physical gold is trading below the $1,300/oz mark at ~$1,222/oz (Figure-6). Nevertheless, gold prices have witnessed a general recovery during the past 30 days, and we may expect some stability in gold prices where gold may reach the $1,300/oz mark in the coming two or three quarters.

Figure-6 (Source: Infomine)

Figure-6 (Source: Infomine)

Increased FCFs are a support for the expansion of other mining properties:

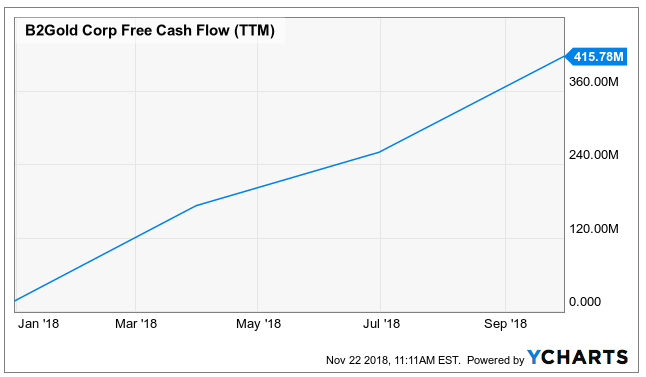

As shown in Figure-7, BTG is on track to increase its FCF (read: Free Cash Flows), and I believe it should help the company to incur CAPEX for the expansion/ exploration of its other mining properties.

Figure-7 (Source: YCharts)

Figure-7 (Source: YCharts)

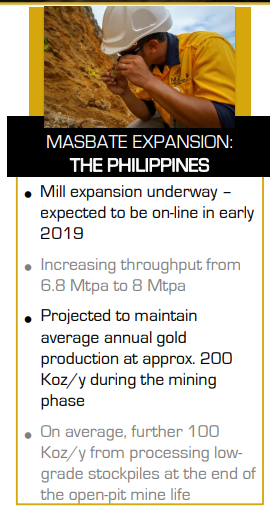

On that note, one should pay attention to the fact that BTG is on track to expand its mining properties. One such property is the Masbate mine in the Philippines (Figure-8). As noted in Figure-2, this mine is the second-largest producing mine in BTG's portfolio. Hence, we can expect that an expansion in this mine would noticeably enhance the company's production potential in future.

Figure-8 (Source: November Presentation)

Figure-8 (Source: November Presentation)

Conclusion:

BTG has updated its resource estimate for its flagship asset and is in the process of expanding the mining operations in other mining properties owned by it. The company has sufficient FCFs to support the expansion of mining operations/ exploration and drilling activities and is well-positioned to take advantage of an improvement in gold prices.

Moreover, the company has reported strong financial and operational performance during Q3, and the technical analysis also suggests that the rally may continue. Based on these facts, I believe that BTG presents an attractive investment opportunity in the gold mining space.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Follow Aitezaz Khan and get email alerts