Banking on Diamonds

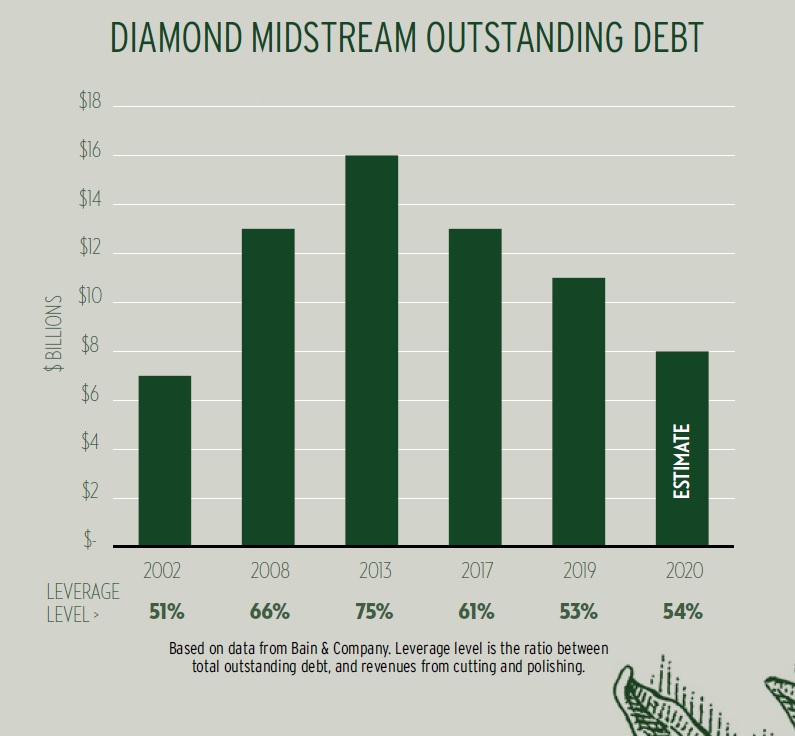

RAPAPORT... In both financial and diamond industry terms, 2017 seems like an eternity ago. Bankers at the Dubai Diamond Conference in October of that year gave a stark warning to the diamond sector: The trade is over-financed, insufficiently transparent, not profitable enough, and altogether too risky. This was their unanimous observation, to the discomfort of the audience. With bank credit amounting to an estimated $13 billion at the time, lenders claimed the industry could function sufficiently on just $8 billion. Bankers were already reducing their exposure to the trade's risks, and many had closed their diamond units altogether. Today, bank credit has reached that $8 billion level, according to estimates from Bain & Company (see graph). Meanwhile, the diamond industry appears to have enhanced its stature among lenders. In an unexpected twist, the midstream radically improved its liquidity position during the challenging pandemic period. "We're seeing that our clients had much better profitability in 2020 than 2019," reports Davy Blommaert, head of diamond lending at the Dubai-based National Bank of Fujairah (NBF). Because supply was limited, he explains, diamond value went up during the pandemic, whereas 2019 was a tough year that saw an excess of polished on the market. As factories closed and rough buying froze during the lockdowns of 2020's second quarter, diamond cutters were able to reduce the inventory that had been weighing on their businesses. The lack of new polished meant other suppliers, too, could focus on selling old stock that had been difficult to move. Unlike in previous years, when the decline in financing was due to banks' reluctance to take on the risks the industry carried, last year's dramatic drop resulted from lower demand for funding. When banks finance a diamond company, they look at its assets, which are typically inventory and receivables - the outstanding payments that clients owe the company - explains Blommaert. Less inventory means companies are more liquid, he says, and the more liquid they are, the more they want to buy for cash rather than on credit terms, since they have sufficient funds and can get a discount with cash.Currently, inventory and receivables are both low, meaning diamantaires are holding fewer assets that need financing, Blommaert observes, adding that he personally has "never known leverage in our industry to be so low."

RAPAPORT... In both financial and diamond industry terms, 2017 seems like an eternity ago. Bankers at the Dubai Diamond Conference in October of that year gave a stark warning to the diamond sector: The trade is over-financed, insufficiently transparent, not profitable enough, and altogether too risky. This was their unanimous observation, to the discomfort of the audience. With bank credit amounting to an estimated $13 billion at the time, lenders claimed the industry could function sufficiently on just $8 billion. Bankers were already reducing their exposure to the trade's risks, and many had closed their diamond units altogether. Today, bank credit has reached that $8 billion level, according to estimates from Bain & Company (see graph). Meanwhile, the diamond industry appears to have enhanced its stature among lenders. In an unexpected twist, the midstream radically improved its liquidity position during the challenging pandemic period. "We're seeing that our clients had much better profitability in 2020 than 2019," reports Davy Blommaert, head of diamond lending at the Dubai-based National Bank of Fujairah (NBF). Because supply was limited, he explains, diamond value went up during the pandemic, whereas 2019 was a tough year that saw an excess of polished on the market. As factories closed and rough buying froze during the lockdowns of 2020's second quarter, diamond cutters were able to reduce the inventory that had been weighing on their businesses. The lack of new polished meant other suppliers, too, could focus on selling old stock that had been difficult to move. Unlike in previous years, when the decline in financing was due to banks' reluctance to take on the risks the industry carried, last year's dramatic drop resulted from lower demand for funding. When banks finance a diamond company, they look at its assets, which are typically inventory and receivables - the outstanding payments that clients owe the company - explains Blommaert. Less inventory means companies are more liquid, he says, and the more liquid they are, the more they want to buy for cash rather than on credit terms, since they have sufficient funds and can get a discount with cash.Currently, inventory and receivables are both low, meaning diamantaires are holding fewer assets that need financing, Blommaert observes, adding that he personally has "never known leverage in our industry to be so low." Profitable roughMany credit De Beers and Alrosa with the improvement, as they allowed greater flexibility in their rough sales during the crisis. The two miners - which combined account for about half of global rough production - let clients refuse goods between March and September, thereby reducing supply while keeping prices stable.As a result, there was less need for financing, since the banks usually fund those rough purchases, explains Olya Linde, a partner with Bain & Company's energy and natural resources division, as well as coauthor of Bain's annual diamond report.Meanwhile, prices at rough auctions and tenders fell 20% to 30% as smaller miners that needed liquidity were forced to sell. Many in the trade took advantage of that, Linde notes - and Blommaert says they are reaping the benefits today, since both rough and polished prices have recovered.Before Covid-19, rough from a given mine would sell at around $100 per carat, but that dropped to about $73 during the pandemic, Blommaert elaborates. While it has since gone back up to around $110, those who bought at the lower rate are now enjoying increased profitability. Manufacturers usually achieve a margin of some 3%, he says, but if their cost was $73 and they are selling polished at the same price as before, they'll suddenly see significant gains.Improving the risk profileAll of the banking and industry professionals Rapaport Magazine interviewed agree that 2020 was healthy for the midstream, which improved its profits despite the challenging conditions."[The trade] embraced technology and the changes that were forced upon it," says Linde. "And it was able to clean up its inventory due to the disruptions in the supply chain."Importantly, there were very few reports of bankruptcies in the manufacturing and trading centers. That has raised banks' tolerance for the industry, according to one India-based banker who has requested anonymity."When the pandemic and lockdowns were declared, there was some resistance from banks to extend finance, as they thought the trade would face more risk, challenges and stress," says Colin Shah, chairman of India's Gem & Jewellery Export Promotion Council (GJEPC). "After one year, the trade has come back strong, standing on its own feet, and operating with near-normal capacity. So the earlier concerns perceived by the banks are no longer relevant."Even before Covid-19, the industry was slowly improving its risk profile among lenders. That was largely because banks were steadily leaving the industry or taking steps to protect themselves from its hazards. Antwerp Diamond Bank, Standard Chartered Bank and Israel's Bank Leumi all stopped funding the sector in the last six years, resulting in more than $2 billion worth of credit leaving the trade.Just as significantly, ABN Amro - one of the largest lenders to the industry - reduced its credit facility for rough buying, influencing others to do the same. Diamantaires were forced to self-finance a portion of their rough purchases. This served the trade well during the pandemic, says Blommaert, as traders have learned how to work with less reliance on the banks.Transparency mattersAnother thing contributing to the industry's improved profile in recent years has been the shift to more corporate structures. De Beers' program to ensure that sightholders comply with International Financial Reporting Standards (IFRS) has helped the market a lot. The wider adoption of measures such as IFRS accounting guidelines has facilitated greater financing opportunities, according to Hilmar Hauer, head of debt products at Channel Capital, which provides securitized financing tothe diamond trade. "For the global capital markets, the improved transparency is a really important factor when we analyze companies," he comments. The anonymous Indian banker agrees that "the industry is becoming more transparent and bringing in better corporate governance."The industry has also made some strides in improving its reputation among consumers, according to Erik Jens, founder of LuxuryFintech and former head of ABN Amro's diamond and jewelry client division.The trade has become increasingly focused on doing the right thing, with initiatives such as Diamonds Do Good, the Responsible Jewellery Council (RJC) and the World Jewellery Confederation (CIBJO) working to raise the industry's corporate social responsibility (CSR) standards, he notes. Jens foresees this opening up new financing avenues for the sector.He also points to a trend in which banks are tying their loans to a company's sustainability platform. In April, jewelry brand Pandora secured a new EUR 950 million ($1.15 billion) credit facility that links the borrowing costs to the progress the company makes toward its environmental goals. These goals include becoming carbon-neutral and using only recycled silver and gold in its products.A juicy pastReputational risk factors are important to regulators such as the central banks, which set compliance standards for the banking sector. Guided by the Basel Accords - which require lenders, and consequently their customers, to have a minimum amount of equity and liquidity - those standards continue to tighten. This has implications for the diamond trade, Jens points out."When the regulators say an industry is [an] increased risk, it creates a portfolio decision for credit committees, boards and management teams," he explains. "They have to decide if they want to finance the business or not, [taking into account any stringencies the industry has put in place to mitigate the risks]."Banks would still rather lose money on a real estate firm or coffee trader than on a diamond company, given that the latter sector garners a lot more press than others, he says. "There was a mystery about the diamond trade, and these [negative stories] have been very juicy in the past." That said, diamonds performed better than many other asset classes during the pandemic, Blommaert notes.Supportive measuresBlommaert, Hauer and the Indian banker all stress that they are comfortable with the industry's current risk profile. Furthermore, lenders and governments provided significant support for the trade during the pandemic.As Covid-19 spread, the Reserve Bank of India revised its lending guidelines to let companies realign their working capital and get extensions on their loans, Shah reports. The Indian government also guaranteed loans to micro, small and medium enterprises - which included many diamond companies - amounting to INR 3 trillion (about $41 billion).In Israel, 300 diamantaires received loans of between NIS 250,000 ($75,000) and NIS 4 million ($1.2 million), reports Yoram Dvash, president of the World Federation of Diamond Bourses (WFDB), who recently stepped down as president of the Israel Diamond Exchange (IDE). The government guaranteed 85% of the loans, and the banks covered the rest, waiving repayment and interest during the first year, he adds.Meanwhile, Belgium introduced emergency financial concessions to help companies survive the downturn, offering businesses extra time to repay loans and meet tax obligations. The country's parliament also passed a law entitling diamond companies to open bank accounts - a great relief to diamantaires who have suffered repeated rejections from lenders in recent years, according to Chaim Pluczenik, president of the Antwerp World Diamond Centre (AWDC).Finding alternativesWhile the Belgian law was supposed to go into effect on May 1, its implementation has been postponed, to the frustration of Antwerp-based dealers. For years, the country's banks have shunned the industry, and diamantaires have struggled to open even a personal account because they are associated with the trade. Many turned to fintech for banking solutions, or simply to ensure they could receive and make payments on a deal. While one such platform, Ebury, was discontinued after failing to meet compliance standards - temporarily freezing its clients' funds in the process - other options are available. More non-bank institutions are becoming interested in the industry, according to an Antwerp-based sightholder who has requested anonymity.Various initiatives targeting smaller diamond companies have launched in recent years, with peer-to-peer financing gaining traction, notes Bain's annual report on the diamond industry. However, the majority of non-bank lending goes to larger manufacturers via asset-backed securitization - a financial instrument that uses a company's assets, such as debt, inventory or equity, as collateral. In it for the long term Providers such as Channel Capital Advisors and Guggenheim Securities use asset-backed securitization for a limited number of clients - those that have sufficient scale and can withstand the necessary scrutiny. Manufacturer Rosy Blue, for instance, has a credit facility with Channel, while fellow manufacturers Pluczenik Diamond Company and Diarough have deals with Guggenheim. While the existence of those arrangements is public knowledge, most deals are private, in keeping with the nature of some parts of the diamond industry, Channel's Hauer says. These types of deals are also subject to tremendous scrutiny by the lender. Channel does in-depth due diligence in vetting its clients, working to understand their businesses and ensure they have the requisite corporate governance structures in place, Hauer affirms. To qualify, companies must have the revenue flow to pay back the loan over the agreed term - typically three to five years.The advantage of this arrangement for diamond companies is that it provides secure long-term funding. Whereas with typical working capital lines, a bank may pull its credit facility on short notice, debt providers such as Channel and Guggenheim are committed for the long haul. As long as the company continues to comply with the loan terms, the financing cannot be withdrawn. As part of those terms, the diamond companies agree to utilize the full sum available to them for the duration of the loan period.Hauer notes a rise in diamond companies' interest in non-bank financing, and has found that more securitization management firms, in turn, are willing to work with the diamond sector. Banks' continued exit from diamond financing has contributed to those trends, as has the trade's solid performance within the securitization system, he says.Building goodwillStill, the bulk of lending is done by the banks, and their response to the pandemic signaled that the working relationship between diamantaires and their lenders was beginning to thaw. "The industry was always complaining about the banks, and the banks were complaining about the industry," Jens says. "But I think those pain points have been reduced a lot. The relationship has become more normalized."That changing dynamic will be important, as the need for financing is likely to rise along with trading activity in 2021. Already, a spike in rough demand since the beginning of the year has caused some concern about overdue payments, says Pluczenik. De Beers' rough sales for January through April more than doubled year on year to $2.04 billion in total, and rough prices have largely returned to pre-pandemic levels.However, few expect such high demand to persist for the rest of the year. Furthermore, De Beers and Alrosa arebeing careful not to oversupply the market - thus keeping demand for financing in check, Blommaert says.No pressureDiamantaires should not take the current availability of financing for granted, warn Blommaert and Jens. Because receivables declined and businesses didn't use their full credit lines in 2020, banks may decide to reduce those facilities.If a bank provides credit with a limit of $50 million, for example, and the diamantaire only uses $20 million, the bank still has to carry capital reserves for the $50 million, Jens explains. "They're not making money on it, and they have to pay."The banks are waiting to see how the market evolves before making any decisions about raising or lowering their diamond clients' credit. While there is optimism about consumer demand in the US and China, there are also concerns that the pandemic will linger through 2022, as Bain expects. The recent spike in infection rates in India has fueled concerns about supply disruptions, as well as fears that the full recovery might take longer than expected. Manufacturing in India declined an estimated 30% to 40% in April and May due to high worker absenteeism and limitations resulting from the pandemic. Meanwhile, the Gemological Institute of America (GIA) is reporting a backlog of over a month at its Mumbai and Surat labs. For now, however, the diamond industry is confident that it has sufficient liquidity to see it through any setbacks, and that it has built up enough goodwill to sustain its newfound favor with the banking sector."I don't think there is business that people are not able to do because they don't have the funding," says the anonymous Indian banker. Liquidity has remained stable despite the disruptions from the new Covid-19 wave in India, since demand continues, he stresses. "People have liquidity that is fueling their business at the moment," agrees Dvash. "Business is moving, and turnover is very quick when you buy. I don't feel there is pressure from the banks on the trade - neither in Israel,Belgium or India."This article first appeared in the June 2021 issue of Rapaport Magazine.

Profitable roughMany credit De Beers and Alrosa with the improvement, as they allowed greater flexibility in their rough sales during the crisis. The two miners - which combined account for about half of global rough production - let clients refuse goods between March and September, thereby reducing supply while keeping prices stable.As a result, there was less need for financing, since the banks usually fund those rough purchases, explains Olya Linde, a partner with Bain & Company's energy and natural resources division, as well as coauthor of Bain's annual diamond report.Meanwhile, prices at rough auctions and tenders fell 20% to 30% as smaller miners that needed liquidity were forced to sell. Many in the trade took advantage of that, Linde notes - and Blommaert says they are reaping the benefits today, since both rough and polished prices have recovered.Before Covid-19, rough from a given mine would sell at around $100 per carat, but that dropped to about $73 during the pandemic, Blommaert elaborates. While it has since gone back up to around $110, those who bought at the lower rate are now enjoying increased profitability. Manufacturers usually achieve a margin of some 3%, he says, but if their cost was $73 and they are selling polished at the same price as before, they'll suddenly see significant gains.Improving the risk profileAll of the banking and industry professionals Rapaport Magazine interviewed agree that 2020 was healthy for the midstream, which improved its profits despite the challenging conditions."[The trade] embraced technology and the changes that were forced upon it," says Linde. "And it was able to clean up its inventory due to the disruptions in the supply chain."Importantly, there were very few reports of bankruptcies in the manufacturing and trading centers. That has raised banks' tolerance for the industry, according to one India-based banker who has requested anonymity."When the pandemic and lockdowns were declared, there was some resistance from banks to extend finance, as they thought the trade would face more risk, challenges and stress," says Colin Shah, chairman of India's Gem & Jewellery Export Promotion Council (GJEPC). "After one year, the trade has come back strong, standing on its own feet, and operating with near-normal capacity. So the earlier concerns perceived by the banks are no longer relevant."Even before Covid-19, the industry was slowly improving its risk profile among lenders. That was largely because banks were steadily leaving the industry or taking steps to protect themselves from its hazards. Antwerp Diamond Bank, Standard Chartered Bank and Israel's Bank Leumi all stopped funding the sector in the last six years, resulting in more than $2 billion worth of credit leaving the trade.Just as significantly, ABN Amro - one of the largest lenders to the industry - reduced its credit facility for rough buying, influencing others to do the same. Diamantaires were forced to self-finance a portion of their rough purchases. This served the trade well during the pandemic, says Blommaert, as traders have learned how to work with less reliance on the banks.Transparency mattersAnother thing contributing to the industry's improved profile in recent years has been the shift to more corporate structures. De Beers' program to ensure that sightholders comply with International Financial Reporting Standards (IFRS) has helped the market a lot. The wider adoption of measures such as IFRS accounting guidelines has facilitated greater financing opportunities, according to Hilmar Hauer, head of debt products at Channel Capital, which provides securitized financing tothe diamond trade. "For the global capital markets, the improved transparency is a really important factor when we analyze companies," he comments. The anonymous Indian banker agrees that "the industry is becoming more transparent and bringing in better corporate governance."The industry has also made some strides in improving its reputation among consumers, according to Erik Jens, founder of LuxuryFintech and former head of ABN Amro's diamond and jewelry client division.The trade has become increasingly focused on doing the right thing, with initiatives such as Diamonds Do Good, the Responsible Jewellery Council (RJC) and the World Jewellery Confederation (CIBJO) working to raise the industry's corporate social responsibility (CSR) standards, he notes. Jens foresees this opening up new financing avenues for the sector.He also points to a trend in which banks are tying their loans to a company's sustainability platform. In April, jewelry brand Pandora secured a new EUR 950 million ($1.15 billion) credit facility that links the borrowing costs to the progress the company makes toward its environmental goals. These goals include becoming carbon-neutral and using only recycled silver and gold in its products.A juicy pastReputational risk factors are important to regulators such as the central banks, which set compliance standards for the banking sector. Guided by the Basel Accords - which require lenders, and consequently their customers, to have a minimum amount of equity and liquidity - those standards continue to tighten. This has implications for the diamond trade, Jens points out."When the regulators say an industry is [an] increased risk, it creates a portfolio decision for credit committees, boards and management teams," he explains. "They have to decide if they want to finance the business or not, [taking into account any stringencies the industry has put in place to mitigate the risks]."Banks would still rather lose money on a real estate firm or coffee trader than on a diamond company, given that the latter sector garners a lot more press than others, he says. "There was a mystery about the diamond trade, and these [negative stories] have been very juicy in the past." That said, diamonds performed better than many other asset classes during the pandemic, Blommaert notes.Supportive measuresBlommaert, Hauer and the Indian banker all stress that they are comfortable with the industry's current risk profile. Furthermore, lenders and governments provided significant support for the trade during the pandemic.As Covid-19 spread, the Reserve Bank of India revised its lending guidelines to let companies realign their working capital and get extensions on their loans, Shah reports. The Indian government also guaranteed loans to micro, small and medium enterprises - which included many diamond companies - amounting to INR 3 trillion (about $41 billion).In Israel, 300 diamantaires received loans of between NIS 250,000 ($75,000) and NIS 4 million ($1.2 million), reports Yoram Dvash, president of the World Federation of Diamond Bourses (WFDB), who recently stepped down as president of the Israel Diamond Exchange (IDE). The government guaranteed 85% of the loans, and the banks covered the rest, waiving repayment and interest during the first year, he adds.Meanwhile, Belgium introduced emergency financial concessions to help companies survive the downturn, offering businesses extra time to repay loans and meet tax obligations. The country's parliament also passed a law entitling diamond companies to open bank accounts - a great relief to diamantaires who have suffered repeated rejections from lenders in recent years, according to Chaim Pluczenik, president of the Antwerp World Diamond Centre (AWDC).Finding alternativesWhile the Belgian law was supposed to go into effect on May 1, its implementation has been postponed, to the frustration of Antwerp-based dealers. For years, the country's banks have shunned the industry, and diamantaires have struggled to open even a personal account because they are associated with the trade. Many turned to fintech for banking solutions, or simply to ensure they could receive and make payments on a deal. While one such platform, Ebury, was discontinued after failing to meet compliance standards - temporarily freezing its clients' funds in the process - other options are available. More non-bank institutions are becoming interested in the industry, according to an Antwerp-based sightholder who has requested anonymity.Various initiatives targeting smaller diamond companies have launched in recent years, with peer-to-peer financing gaining traction, notes Bain's annual report on the diamond industry. However, the majority of non-bank lending goes to larger manufacturers via asset-backed securitization - a financial instrument that uses a company's assets, such as debt, inventory or equity, as collateral. In it for the long term Providers such as Channel Capital Advisors and Guggenheim Securities use asset-backed securitization for a limited number of clients - those that have sufficient scale and can withstand the necessary scrutiny. Manufacturer Rosy Blue, for instance, has a credit facility with Channel, while fellow manufacturers Pluczenik Diamond Company and Diarough have deals with Guggenheim. While the existence of those arrangements is public knowledge, most deals are private, in keeping with the nature of some parts of the diamond industry, Channel's Hauer says. These types of deals are also subject to tremendous scrutiny by the lender. Channel does in-depth due diligence in vetting its clients, working to understand their businesses and ensure they have the requisite corporate governance structures in place, Hauer affirms. To qualify, companies must have the revenue flow to pay back the loan over the agreed term - typically three to five years.The advantage of this arrangement for diamond companies is that it provides secure long-term funding. Whereas with typical working capital lines, a bank may pull its credit facility on short notice, debt providers such as Channel and Guggenheim are committed for the long haul. As long as the company continues to comply with the loan terms, the financing cannot be withdrawn. As part of those terms, the diamond companies agree to utilize the full sum available to them for the duration of the loan period.Hauer notes a rise in diamond companies' interest in non-bank financing, and has found that more securitization management firms, in turn, are willing to work with the diamond sector. Banks' continued exit from diamond financing has contributed to those trends, as has the trade's solid performance within the securitization system, he says.Building goodwillStill, the bulk of lending is done by the banks, and their response to the pandemic signaled that the working relationship between diamantaires and their lenders was beginning to thaw. "The industry was always complaining about the banks, and the banks were complaining about the industry," Jens says. "But I think those pain points have been reduced a lot. The relationship has become more normalized."That changing dynamic will be important, as the need for financing is likely to rise along with trading activity in 2021. Already, a spike in rough demand since the beginning of the year has caused some concern about overdue payments, says Pluczenik. De Beers' rough sales for January through April more than doubled year on year to $2.04 billion in total, and rough prices have largely returned to pre-pandemic levels.However, few expect such high demand to persist for the rest of the year. Furthermore, De Beers and Alrosa arebeing careful not to oversupply the market - thus keeping demand for financing in check, Blommaert says.No pressureDiamantaires should not take the current availability of financing for granted, warn Blommaert and Jens. Because receivables declined and businesses didn't use their full credit lines in 2020, banks may decide to reduce those facilities.If a bank provides credit with a limit of $50 million, for example, and the diamantaire only uses $20 million, the bank still has to carry capital reserves for the $50 million, Jens explains. "They're not making money on it, and they have to pay."The banks are waiting to see how the market evolves before making any decisions about raising or lowering their diamond clients' credit. While there is optimism about consumer demand in the US and China, there are also concerns that the pandemic will linger through 2022, as Bain expects. The recent spike in infection rates in India has fueled concerns about supply disruptions, as well as fears that the full recovery might take longer than expected. Manufacturing in India declined an estimated 30% to 40% in April and May due to high worker absenteeism and limitations resulting from the pandemic. Meanwhile, the Gemological Institute of America (GIA) is reporting a backlog of over a month at its Mumbai and Surat labs. For now, however, the diamond industry is confident that it has sufficient liquidity to see it through any setbacks, and that it has built up enough goodwill to sustain its newfound favor with the banking sector."I don't think there is business that people are not able to do because they don't have the funding," says the anonymous Indian banker. Liquidity has remained stable despite the disruptions from the new Covid-19 wave in India, since demand continues, he stresses. "People have liquidity that is fueling their business at the moment," agrees Dvash. "Business is moving, and turnover is very quick when you buy. I don't feel there is pressure from the banks on the trade - neither in Israel,Belgium or India."This article first appeared in the June 2021 issue of Rapaport Magazine.