February 07, 2026

A Critical Minerals Opportunity of the Decade

Contents

- An Overlooked “Copper Kingdom”

- Midnight Sun’s (MMA.V, MDNGF) IMMEDIATE Value Proposition

- The Imminent Catalyst for Midnight Sun

- Dumbwa’s Economic Potential Could Exceed Its MASSIVE Neighbor

- Key to a Great Deposit: Mineralization Starts Right at Surface

- A Clear Vision for a Profitable Endgame

- Optionality at Play

- The Midnight Sun Thesis

The global trade war continues. And it has been pushing commodity prices higher and higher.

Gold and silver are trading at all-time highs. Critical minerals such as copper have joined this once-in-a-generation bull market.

Investors can choose how they want to play it.

They can go the common way and get exposure to commodities through ETFs. It’s easy to do, but ETFs have a limited upside.

If you want to give your portfolio an extra boost, there are only a few options available outside of the junior resource space.

World’s wealthiest people, such as Amazon’s founder Jeff Bezos and Microsoft’s Bill Gates, chose a different path. They are investing in a private junior resource company working in this specific country… Zambia.

A company linked to the United Arab Emirates, the global oil leader, has invested over USD 1.1 billion in a Zambian mine in 2025.

And these billionaires and wealthy investment funds have chosen copper as their investment of preference.

Now, there are many copper companies operating in the world… even in Zambia.

The problem here is that it’s not easy to tell future winners from potential losers.

This is why here at Canadian Mining Report, we bring our investors opportunities that they don’t learn about anywhere else.

The resource junior we will discuss in a moment works in the copper space, owns projects in Zambia, and it has one of the most distinguished geologists on its team.

He was Exploration Manager in the region for one of the world’s largest copper producers, and has many deposits to his credit. He led the team that transformed Barrick’s Lumwana deposit in Zambia into a 1.62 billion-tonne monster. Lumwana was part of a CAD7.3 billion acquisition 20 years prior, when copper was only $1.50 per pound.

And now, he is working to advance a project that looks the same geologically, only with a larger footprint on strike, at surface.

Same commodity, same country… but a much better copper price environment.

We believe that the company on our radar today, Midnight Sun (MMA.V, MDNGF), is one of the rare “right place, right time” situations.

Let’s start with the “place” part…

An Overlooked “Copper Kingdom”

Few investors have Zambia as their top-of-mind copper jurisdiction. Yet they should.

The country has been one of the world’s top copper producers for over 100 years. Its geology created large and scalable copper deposits billions of years ago… yet it takes a specific kind of expertise to find them.

Zambia remains a world-class copper producer and hosts some of the largest mining companies, such as First Quantum, Barrick (and its Lumwana mine, which Midnight Sun’s geologist helped discover), Ivanhoe, Rio Tinto, Anglo American and others.

The country takes mining seriously. The industry represents 75% of its exports. Zambia’s government has an ambitious goal of tripling its copper output between 2025 and 2031.

It is also a stable and predictable mining jurisdiction.

And investment has been flowing in. For example, the United States and the European Union plan to build a multibillion-dollar Lobito railway that would start in Eastern Zambia, connecting a North-South rail line with an East-West one and linking the four key Zambian copper mines with a port in Angola.

First Quantum, one of the global mining giants working in Zambia, is building its own 371-kilometre route to cut transit times for its operations. The company expects the upgrade to be ready within two years.

First Quantum and Barrick are pouring billions of dollars into Zambia. First Quantum is working on a USD1.25-billion production expansion at its Kansanshi mine, and Barrick is investing USD2 billion in Lumwana.

China, the United States, and the European Union have earmarked billions of dollars to improve the country’s infrastructure and get its copper to the international markets as quickly as possible.

One resource junior looks poised to benefit from this investment frenzy, regardless of which global superpower comes out first.

Midnight Sun’s (MMA.V, MDNGF) IMMEDIATE Value Proposition

Before the Zambian copper rush began, Midnight Sun realized that it could get positioned in one of the most prolific copper regions in the world—and potentially create billions of dollars in shareholder value.

The company’s CEO, Al Fabbro, who has over 45 years of experience in mining and finance, has been implementing a strategy of focusing on projects with ultra-large-scale potential.

Dumbwa, Midnight Sun’s flagship deposit, has the potential to reach the same size and scale as the neighboring Lumwana deposit, the largest in the Zambian copper belt…

This, in a nutshell, is what Midnight Sun is on to. The company has started exploration at Dumbwa, and the early drill results have delivered excellent progress. (More on that in a moment.) The market has noticed the company’s progress, too… Over the past 12 months, Midnight Sun’s share price has soared by 135%.

But, most likely, this is just the beginning of the Midnight Sun story. Here’s why…

The Imminent Catalyst for Midnight Sun

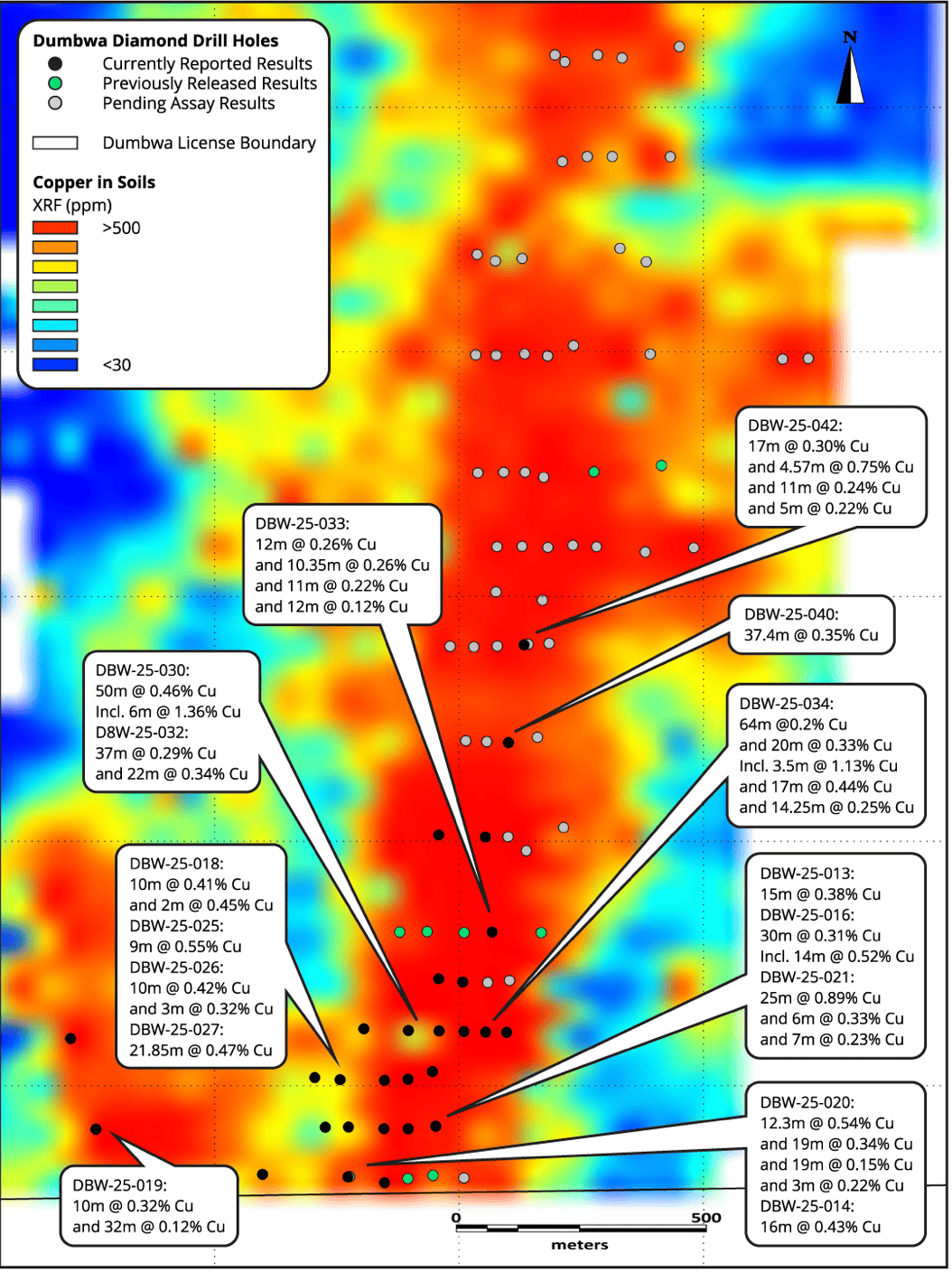

The company has reported the results of just 29 of the 155 holes it has drilled so far at Dumbwa. The rest are being cut, prepped and assayed, to be ready for release.

And here’s why it matters…

The soil anomaly at Dumbwa that Midnight Sun is currently drilling out appears to continue unbroken for 20 kilometers… Representing potential for a vast copper deposit.

And so far, Dumbwa has proven to be highly consistent. Management is targeting a large-tonnage, near-surface deposit with a goal of over one billion tonnes at a grade of around 0.5% copper.

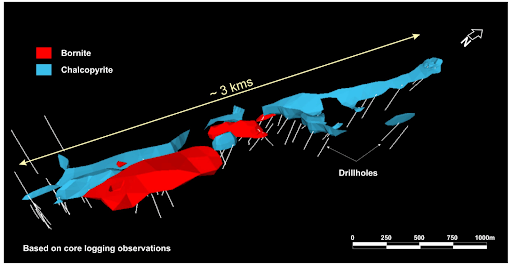

The graphic below shows how consistent the deposit really is over the 3.6-kilometer stretch that the company has already delineated with drilling.

Dumbwa is a new near-surface sulphide copper deposit, with Midnight Sun targeting +one billion tonnes in volume with similar grade potential to surrounding mines.

Dumbwa Could Become the Next Major Copper Deposit in the Zambian Copper Belt

As to the grades and widths that the company has seen so far… they are very similar to those of the Lumwana mine located just 20 kilometers away.

Lumwana is operated by Barrick Mining Corp., one of the world’s leading resource companies.

The widths and grades at Lumwana are in the range of 10-40 meters of 0.3–0.6% copper. The assays that Midnight Sun has received so far show intervals with similar widths and grades. The image below shows a snapshot of some of the results seen to-date.

Midnight Sun expects that drill results with similar lengths and grades could continue for at least another 8 kilometers, and if surface geochemistry is correct, up to 20 kilometres in total.

Even without the high-grade sub-intervals (red bars in the image below), the longer and lower-grade intervals that contain them are comparable to the ones economically mined at Lumwana. For example:

Hole DBW-007: 136 meters of 0.26% copper, starting from four meters down hole;

Hole DBW-009: 60 meters of 0.40% copper, starting from 119 meters down hole;

Hole DBW-010: 80 meters of 0.36% copper, starting from 42 meters down hole.

This tells investors that the company has defined what could be the newest major Zambian copper deposit in the belt.

And it may not take too long for Midnight’s neighbor Barrick to notice… In fact, Midnight Sun’s geologist, Dr. Kevin Bonel, was Exploration Manager at the Lumwana mine and Freeport McMoRan, another copper major.

While working as Exploration Manager for Barrick at Lumwana, Dr. Bonel and his team transitioned the project from about 900 million tonnes at 0.5% copper to 1.6 billion tonnes at 0.5% copper.

He and his team almost doubled Lumwana’s tonnage while keeping its grade intact. With that they added 62 years of mine life to the project and nearly 9 million tonnes of contained copper.

Of course, we cannot predict which strategic investors may get as excited about Dumbwa as the company’s team already is, but we know that majors are starved of new discoveries… and Dumbwa has started looking like a major one.

And the company has enough liquidity to continue its exploration effort. Midnight Sun has about CAD38 million in its treasury.

The company's plan for 2026 is ambitious, and it could change the way the market perceives Midnight Sun. Management says that it plans to drill 10,000 meters per month until the end of the year.

Just by the third quarter of this year, the company plans to drill the first 11.8 kilometers of the projected 20 kilometre expected strike length. If mineralization at Dumbwa remains consistent, this campaign could quickly triple… and Midnight Sun will have about CAD15 million left in the bank to continue advancing Dumbwa and its other assets.

Management pointed out that, on average, the company spends about CAD160 per meter of drilling. This is one of the lowest numbers we have seen. In other words, Midnight Sun can do much more work with the capital it has than some of its rivals, who face higher costs.

This benefits investors who see their money going toward getting more work done—and potentially creating more shareholder value in the process.

Key to a Great Deposit: Mineralization Starts Right at Surface

The best thing about these drill results is how close to the surface they are. Usually, if a deposit lies deep in the ground, it is expensive to mine. An operator would need to remove a lot of “waste,” or non-economic material, before it gets to the good stuff.

In the case of Dumbwa, as the company’s recent drill results show, the good stuff starts almost at the surface. This is fantastic news for the project’s potential economics.

Another advantage that Dumbwa has is its potential low strip ratio… in other words, the ratio of economic-looking ore to waste.

In fact, Dumbwa’s low strip ratio, as estimated by its geological team, is similar to that of Barrick’s Lumwana mine. Lumwana is scheduled to produce 240,000 tonnes of copper per year starting in 2028. It’s a massive mine with a life of over 60 years.

A Clear Vision for a Profitable Endgame

A lot of resource juniors don’t have an exit scenario. They plan to deliver the next batch of assay results or an economic study and see what happens.

Often, nothing does.

Midnight Sun has its eyes on a potential acquisition by a mining major. The company expects that Dumbwa will be too large to ignore by the biggest players in the mining space.

Management makes a comparison to Lumwana, which we mentioned above. It was purchased 20 years ago for CAD7.3 billion. At the time of acquisition, it had about 900 million tonnes of ore at 0.5% copper. If Midnight Sun outlines a mineralized zone over 12 or more kilometers, Dumbwa could potentially have a similar size and grade.

Plus, copper was trading at USD1.50–1.80 when Lumwana was purchased. For reference, as of this writing, copper has closed at USD5.70–5.90, which is over three times higher.

In other words, Midnight Sun might have a similar deposit available for purchase in a much better copper price environment than what Lumwana’s previous owners had to work with. Investors should make their own conclusions about where Dumbwa’s acquisition value might stand.

On top of that, early testing indicates that Dumbwa doesn’t appear to have any “deleterious,” or bad, elements in its mineralization. Lumwana, which was purchased for CAD7.3 billion, did. But Midnight Sun’s team have seen no uranium, cadmium, talc or arsenic present at this stage in delineation.

This, among other features, shows Dumbwa’s advantage over its neighbor, owned by the multi-billion-dollar mining major.

Plus, Dumbwa’s mineralization is copper-only. This makes it easier to work with than would be the case with a polymetallic deposit. Copper could be trickier and costlier to extract from one, damaging project economics. Dumbwa’s mineralization is straightforward and should be easy to process once the project reaches its production stage.

Optionality at Play

Even though Dumbwa could shape up to be a multi-billion-dollar deposit, the company has other assets in its portfolio.

For example, the near-surface Kazhiba copper deposit, which is also in Zambia.

The company has recently announced a mineral resource estimate for Kazhiba. It outlined a NI43-101-compliant Indicated resource of 2.3 million tonnes at 1.41% copper. The deposit contains 72.3 million pounds of copper.

The resource was modeled to a depth of just 30 meters, meaning that its strip ratio will likely be near zero.. Kazhiba also has access to excellent infrastructure.

Midnight Sun plans to monetize Kazhiba by selling the high-grade acid soluble material, and using its future cash flow to finance exploration and development at Dumbwa, the company’s crown jewel.

This plan, when executed, could allow Midnight Sun to continue advancing Dumbwa without the need to raise funds through private placements. This could protect existing shareholders against potential dilution.

In other words, Midnight Sun has developed a non-dilutive plan to bring a brand new Zambian copper deposit to the stage where it may be nearly impossible for the world’s largest mining companies and potential acquirers to resist.

The Midnight Sun Thesis

The trade war continues raging. America’s latest salvo, the threat to take over Greenland, tells investors everything they need to know to understand how serious the Trump administration is about taking control of mineral resources.

China, the United States’ archrival, is doing everything it can to get hold of critical minerals all over the world, too.

The two superpowers have their eyes on Zambia and its vast copper resources.

Access to the country’s critical minerals is so valuable that the world’s most powerful political players and its richest people compete to take control of Zambia’s copper wealth.

Donald Trump, Xi Jinping, Jeff Bezos, Bill Gates, and others have invested billions of dollars in Zambian copper projects and the country’s transport infrastructure.

Meanwhile, established players such as the multibillion-dollar First Quantum, Barrick, Ivanhoe, BHP Anglo American and more look for growth opportunities in Zambia.

Midnight Sun (MMA.V, MDNGF) has positioned itself to benefit from this competition.

The company is advancing a project that could potentially rival the largest copper mines in the country.

It has discovered a consistent, near-surface sulphide copper-bearing deposit that is already nearly four kilometers long… and it can potentially increase its size by almost five times.

Midnight Sun (MMA.V, MDNGF) plans a massive +80,000-meter drill campaign through the end of the year, and the company is fully funded to execute it.

New drill results will be coming in shortly… and so far, they have confirmed management’s geologic theory. Dumbwa, the company’s flagship property, may indeed be a monster-sized near-surface deposit located close to one of the copper majors’ mining infrastructure.

Sophisticated investors have noticed, and the company had no problems raising tens of millions of dollars from them.

It received a vote of confidence from some of the “smartest” money in the business.

But the Midnight Sun (MMA.V, MDNGF) story is still in its earliest stages. If the company continues delivering consistent and economic drill results, its market value may change.

And the company has one of the best executive and technical teams in the industry, perfectly matched to the task at hand.

As we said earlier, this is one of the “right place, right time” situations. And, we would argue, the right time to pay attention to this story is now. This once-a-decade opportunity should be at the top of every resource investor’s watch list.

MUST WATCH: Investment Round Table Discussion on Midnight Sun Mining

Sign up to receive our future articles and updates.

Disclaimer

The material in this article should not under any circumstances be construed as an offering, recommendation, or a solicitation of an offer to buy or sell the securities mentioned or discussed, and is to be used for informational purposes only. Neither Canadian Mining Report (the "Publisher", "we", "us", or "our"), nor any of its principals, directors, officers, employees, or consultants ("Publisher Personnel"), are registered investment advisers or broker-dealers with any agencies in any jurisdictions. Canadian Mining Report ("Canadian Mining Report", "Us", "Our" and/or "We") is a Canadian based media company that typically works with publicly traded companies and provides digital marketing strategies and services.

At most, this communication should serve only as a starting point to do your own research and consult with a licensed professional regarding the companies profiled and discussed. Conduct your own research. We do not provide personalized or individualized investment advice or advice that is tailored to the needs of any particular recipient.

Read More