From Trumped Equities to Gold / Commodities / Gold and Silver 2018

Despite misguided economic policies and risinggeopolitical tensions, the long market expansion has prevailed. But times maybe changing.

Despite misguided economic policies and risinggeopolitical tensions, the long market expansion has prevailed. But times maybe changing.

With the Trump fiscal policies and rearmament, America is takingmore debt than in decades, even though its sovereign debt now exceeds $21.2trillion, or 106 percent of the GDP. As fiscal stimulus kicks in (read: Trump’stax cuts), the deficit will widen.

The US is now the only major advanced economy that’s expected tosee a rise in the debt-to-GDP ratio over the next 5 years (almost 10%!). Thehuge leverage relies on the continued willingness of other countries to financeAmerica’s imbalances, even as US debt held by other countries already hoversaround $6.4 trillion.

Meanwhile, the Sino-US bilateral friction continues, along withtalks on the North American Free Trade Agreement (NAFTA) with Canada andMexico, and on tariffs with the EU. In Europe, political winds are rising,despite cyclical recovery. In Germany, Chancellor Merkel’s rule is moreconstrained politically. Italy is heading to elections in which the old centerhas been played out. In France, May riots indicate Macron’s liabilities. Andvolatility is escalating in the post-Brexit UK.

Multiple international geopolitical flashpoints - from the newCold War against Russia, the unilateral effort to “renew” Iran sanctions, theescalation of violence from Gaza to Syria, the nuclear talks in the KoreanPeninsula, and so on - will ensure that geopolitical risks will prevail, alongwith brickering about the Mueller investigation and mid-term elections in thefall.

And yet, US dollar has strengthened, while Dow Jones remainsover 24,200. Is the market mispricing the risks, once again?

Uneasy markets - and gold

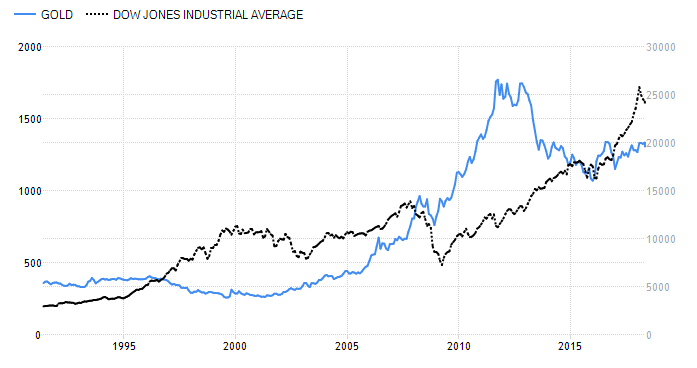

Since the Cold War, there have been several conjecture points asinvestor optimism and booming markets have given way to pessimist sentimentsand bear markets, as evidenced by two decades of Dow Jones and gold prices.

In the Clinton and Bush years markets boomed as investoroptimism was fueled by the technology bubble, speculation in real estate andfinance until 2008. That’s when markets plunged and gold soared until it reached record highs ofalmost $1,900 inSeptember 2011.

As central bankers in major advanced economies resorted toultra-low interest rates and rounds of quantitative easing, a new market boomtook off with President Trump’s arrival in late 2016 (Figure).

But does this mean that markets have a lot of potential toclimb, while gold will remain subdued in the coming years?

Figure Market Booms andBusts via Dow Jones and Gold, 1991-2018

Subdued gold in the short-term

Such views seem to be supported by the World Gold Council'sfirst quarter data, which suggests that gold demand had a soft start, mainlybecause of a fall in investment demand for gold bars and gold-backed ETFs. Yet,jewellery demand was steady as growth in China and the US covered for weakerIndian demand. Moreover, central banks bought 117 ton of gold (42% increaseyear-on-year) and technology demand extended its upward trend.

Gold is again beginning to attract investors, especially thosethat build on secular trends rather than short-term fluctuations. Some believethat gold prices have broken their downtrend line, but others think that thesefluctuations reflect longer-term secular trends.

In long term, secular stagnation is broadening across the majoradvanced economies, which cannot be disguised by monetary injections, hugeleverage and overpriced markets. While the Fed is tightening, central banks inEurope and Japan continue quantitative easing and record-low interest rates.Historically, periods of low rates - or negative rates - tend to correlate withgold returns that are significantly higher than their long-term average.

With increasing global jitters, investors are seeking outtraditional havens from geopolitical risks. Yet, Treasuries are no longer theobvious choice as central banks have turned the bond market into a bubbleterritory.

... While secular trends support gold

Several emerging economies, which today fuel most of globalgrowth prospects, are intrigued by the idea of re-coupling gold with amultilateral currency basket to avoid excessive exposure to US denominatedenergy and commodity markets. As the China-supported One Belt One Road (OBOR)initiatives advance, new arrangements are bypassing US dollar.

While advanced economies, such as the US (8,134 tons) andGermany (3,374 tons), still own most global gold reserves, they are eitherkeeping their current levels of gold or reducing reserves. In contrast, whilethe large emerging economies, including Russia (1,858 tons) and China (1,843tons), own less gold, they are increasing their gold reserves far, farfaster.

In the past decade, the US has increased its gold holdings byonly some 0.5 ton, while Germany has cut its reserves by almost 50 tons. Incontrast, China has tripled its reserves, while Russia has nearly quintupled its gold, despite rounds of sanctions.

As some 90 percent of the physical demand for gold comes fromoutside the US, gold is on the right side of the future.

Dr Steinbock is thefounder of the Difference Group and has served as the research director at theIndia, China, and America Institute (USA) and a visiting fellow at the ShanghaiInstitutes for International Studies (China) and the EU Center (Singapore). Formore information, see http://www.differencegroup.net/

© 2018 Copyright DanSteinbock- All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2018 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.