Gold It's All About Real Interest Rates Not the US Dollar / Commodities / Gold & Silver 2019

TheFederal Reserve’s recent need to supply $100’s of billions in new credit forthe overnight repo market underscores the condition of dollar scarcity in the globalfinancial system. This dearth of dollars and its concomitant strength has left mostmarket watchers baffled.

TheFederal Reserve’s recent need to supply $100’s of billions in new credit forthe overnight repo market underscores the condition of dollar scarcity in the globalfinancial system. This dearth of dollars and its concomitant strength has left mostmarket watchers baffled.

Since2008, the Fed has printed $3.8 trillion (with a “T”) of new dollars in aneffort to weaken the currency and boost asset prices--one would then think theworld should now be awash in dollar liquidity. Yet, surprisingly, there is stillan insatiable demand for the greenback, leading many to wonder what is causing itsstrength. And importantly for preciousmetals investors, there is a need to understand why this dreaded dollar strengthhas not served to undermine the bull market for gold.

Theprimary drivers for dollar strength are growth and interest rate differentials.The Federal Reserve was able to raise overnight lending rates to nearly 2.5%and end its QE program, before its recent retreat from a hawkish monetarypolicy to one that is more dovish. The Fed Funds Rate now stands at 1.75-2.0%.However, the ECB and BOJ both have negative deposit rates and are currentlyengaged in QE. Not only this, but the extra income investors can receive owninga US 10-year Treasury Note compared to those of Japan and Germany are 175bpsand 200 bps, respectively. In addition, year over year GDP growth in the EU wasjust 1.4% in Q2 of 2019; and Japan’s growth registered a paltry 1.0%. Growth inthe US was 2.3% y/y. While that is not earth-an shattering rate of growth, itis still better than our major trading partners.

Withsub-par growth and little hope for improvement on the horizon, the ECB and BOJ havedecided to continue with ZIRP and QE in a futile attempt to spur growth. Nevertheless,their economies are still stagnating.

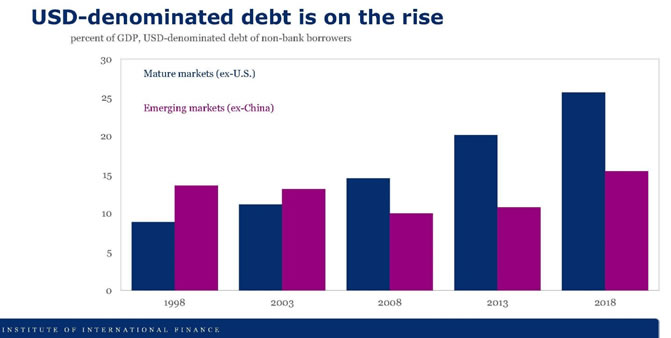

TheUS central bank is now being forced to lower rates once again. This is primarilydue to the strengthening dollar that is hurting foreign holders of USD-denominateddebt--of which there are a lot.

TheBIS estimates that foreign USD-based debt now exceeds $11.5 trillion.

Arising US dollar puts further stress on these dollar-based foreign loans andmakes them harder to service. In effect, this creates a squeeze on dollarshorts. When you add in the Fed’s burning of nearly $800 billion worth of basemoney during its Quantitative Tightening (QT) Program, you can clearly see thereasons for dollar strength.

Butthose who believed the US dollar would increase its buying power against goldhave been dead wrong. This is because the primary driver behind the dollarprice of gold is the direction of real interest rates.

Therefore,it is imperative not to measure the US dollar’s real strength by measuring it againstother flawed fiat currencies that are backed by even more reckless centralbanks. Instead, the genuine value of the dollar should be weighed against realmoney…gold.

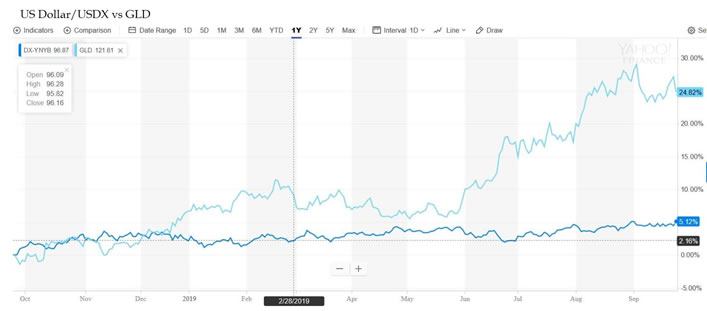

Conventionalwisdom would tell you that the dollar and gold have a reciprocal relationship. Whenthe dollar decreases in value, gold increases and vice versa. However, recently,the dollar and gold have both been strengthening in tandem. Just look at a chart of the dollar index vsthe GLD.

Again,the primary driver of gold isn’t the direction of the dollar but the directionof real interest rates. Hence, if US growth is accelerating in anon-inflationary environment, gold should suffer regardless of the direction ofthe US dollar. Conversely, the USD dollar can be in a bull market against abasket of fiat currencies—as it has been for the past year—and yet can stilllose significant ground against gold as long as nominal interest rates arefalling in an environment of rising inflation.

Theyear-over-year change in core CPI increased 2.4% in August, which was thehighest level in a year. All the while the US 10-year Note yield was crashingfrom nearly 3% to 1.6% over the past 12 months. Therefore, real yields havebeen crashing as gold has been rising.

Thesefalling real yields were rocket fuel for gold, and this was in spite of the USD’sbull market against the euro and yen. The price of gold increased by doubledigits even though the Dollar Index has also increased by nearly 5% in the last12 months. But still, for those of us who love gold it can be a love/haterelationship. It is still down 20% from the highs made in 2011, and the miningshares have crashed by 60%; underscoring the need to know how to trade the cyclesof this sector.

Thequestions for gold investors now are: have nominal yields stopped dropping andwhat is the direction for the rate of inflation? In the short-run, the answerto that question can be found in the trade talks scheduled for October 10thand 11th. The reason for this is, the boy has cried wolf once too often,and it is now time to poop or get off the pot when it comes to reaching anagreement with China on trade. And yes, that boy is Donald Trump. Wall Streetand international corporations cannot do business under this cloud ofuncertainty any longer; where one day tariffs go up, and the next day they arecoming down.

Since early 2017,investors and the C suite have dealt with a perpetual series of dizzying trade warescalations and treaties. Just this September alone, Trump raised duties onChina on the1st of the month. Then onthe 11th he announced a list of exemptions to those very same tariffs. Then, onthe 25th he attacked China viciously at his UN speech, saying: “"Fordecades the international trading system has been easily exploited by nationsacting in very bad faith. Not only has China declined to adopt promisedreforms, it has embraced an economic model dependent on massive marketbarriers, heavy state subsidies, currency manipulation, product dumping, forcedtechnology transfers and the theft of intellectual property and also tradesecrets on a grand scale,"

Thevery next day, Trump said that a deal with China could come "much soonerthan most think." Then, on September 27th, Bloomberg reportedthat the White House threatened to ban the listing of Chinese companies on USexchanges. Businesses simply cannot adequately plan capital expenditures undersuch unstable circumstances.

TheUS and China meet on October 10th &11th to decide the future of tradebetween the two nations. Tariffs are set to increase on Oct.15th on $250billion worth of Chinese goods to 30%, from the current 25%. There is noappetite on Wall Street for the continued ambiguity of this trade war any longer.Therefore, on October the 11th, I expect President Trump to announcethe most wonderful trade deal in history has occurred since we purchased Manhattanfrom the Indians. Such an announcement should provide a temporary boost in the majoraverages and could also cause a sharp selloff in gold. This is because such adeal should put a temporary hold on the Fed’s rate-cutting cycle.

TheFed’s broken models have caused it to fail to grasp the debt-disabled conditionof the developed world. China can no longer boost global GDP because it cannotsignificantly add to its $40 trillion debt pile without cratering the yuan.Also, fiscal and monetary policies are already extremely stretched and areunable to easily pull the economy out of its malaise.

Globalgrowth is faltering, and US GDP growth has shrunk from over 4% last year, tounder 2% in Q3, according to the Atlanta Fed. The most important part of theyield curve remains inverted. There is illiquidity in the Repo market. D.C. is in utter turmoil and annual deficitshave vaulted over the trillion dollar mark. The Q3 earnings report card isabout to arrive, and it will receive an “F.” And global central banks arevirtually out of ammo. Meanwhile, the stock market sits at all-time record highvaluations.

Thepressure on Mr. Trump is now immense. A trade deal must be reached in a matterof days that abrogates future tariffs and rescinds most, if not all, existingduties on China. Any other type of agreement will not be nearly enough to turnthe global economy around or fool Wall Street any longer into thinking that itwill.

Thesad truth is, even a comprehensive trade deal won’t fix the massive debt andasset bubble imbalances that must inevitably implode. Which means, realinterest rates should be setting record lows in the near future.

Michael Pento produces the weekly podcast “The Mid-week Reality Check”,is the President and Founder of PentoPortfolio Strategies and Author of the book “TheComing Bond Market Collapse.”

Respectfully,

MichaelPento

President

PentoPortfolio Strategies

www.pentoport.com

mpento@pentoport.com

(O)732-203-1333

(M)732- 213-1295

MichaelPento is the President and Founder of Pento Portfolio Strategies (PPS). PPS isa Registered Investment Advisory Firm that provides money management services andresearch for individual and institutional clients.

Michaelis a well-established specialist in markets and economics and a regular gueston CNBC, CNN, Bloomberg, FOX Business News and other international mediaoutlets. His market analysis can also be read in most major financialpublications, including the Wall Street Journal. He also acts as a FinancialColumnist for Forbes, Contributor to thestreet.com and is a blogger at theHuffington Post.Prior to starting PPS, Michael served as a senior economist and vice presidentof the managed products division of Euro Pacific Capital. There, he also led anexternal sales division that marketed their managed products to outsidebroker-dealers and registered investment advisors.

Additionally, Michael has worked at an investment advisory firm where he helpedcreate ETFs and UITs that were sold throughout Wall Street. Earlier inhis career he spent two years on the floor of the New York Stock Exchange. He has carried series 7, 63, 65, 55 and Life and Health Insurance www.earthoflight.caLicenses.Michael Pento graduated from Rowan University in 1991.

© 2019 Copyright Michael Pento - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Michael Pento Archive |

© 2005-2019 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.