Gold Weekly: Bearish Speculators Vs. Bullish Investors

Gold is off to a stable start to the week.

Speculators turn more bearish, the CFTC shows.

ETF investors become more bullish, according to Fastmarkets.

The vagaries of the dollar will play a key role in gold's monetary demand.

The December FOMC meeting could mark a dollar peak and an acceleration in the gold rally.

Verus, Oxue ? 1/4 ?? 1/2 '? 1/2 " Moises Miranda Lopez (Saatchi Art)

Introduction

Welcome to my Gold Weekly.

In this report, I wish to discuss mainly my views about the gold market through the GraniteShares Gold Trust ETF (BAR). BAR is directly impacted by the vagaries of gold spot prices because the fund physically holds gold bars in a London vault in the custody of ICBC Standard Bank.

To do so, I analyse the recent changes in speculative positions on the Comex (based on the CFTC) and ETF holdings (based on FastMarkets' estimates) in a bid to draw some interpretations about investor and speculator behavior. Then, I discuss my global macro view and the implications for monetary demand for gold. I conclude the report by sharing my trading positioning.

Speculative positions on the Comex

The CFTC statistics are public and free. The CFTC publishes its Commitment of Traders report (COTR) every Friday, which covers data from the week ending the previous Tuesday. In this COTR, I analyze the speculative positioning, that is, the positions held by the speculative community, called "non-commercials" in the legacy COTR, which tracks data from 1986.

It is important to note that the changes in speculative positioning in the gold futures contracts do not involve physical flows because it is very uncommon for speculators to take delivery of physical on the futures contracts that they trade. Due to the use of leverage by speculators, the changes in speculative positions in gold futures contracts tend to be much greater than the changes in other components of gold demand like ETFs or jewellery.

As a result, the impact on gold spot prices tends to be relatively more important and volatile, which, in turn, affect the value of BAR because the latter physically holds the metal in vaults in London and, therefore, has a direct exposure to spot gold prices.

Gold ETF positions

The data about gold ETF holdings are from FastMarkets, an independent metals agency which tracks ETF holdings across the precious metals complex. FastMarkets tracks on a daily basis a total of 21 gold ETFs, which represent the majority of total gold ETF holdings. The largest gold ETFs tracked by FastMarkets are the SPDR (R) Gold Shares (NYSEARCA:GLD), whose holdings represent nearly 40% of total gold ETF holdings, and the iShares Gold Trust (IAU), whose holdings represent roughly 15% of total gold ETF holdings.

Speculative positioning

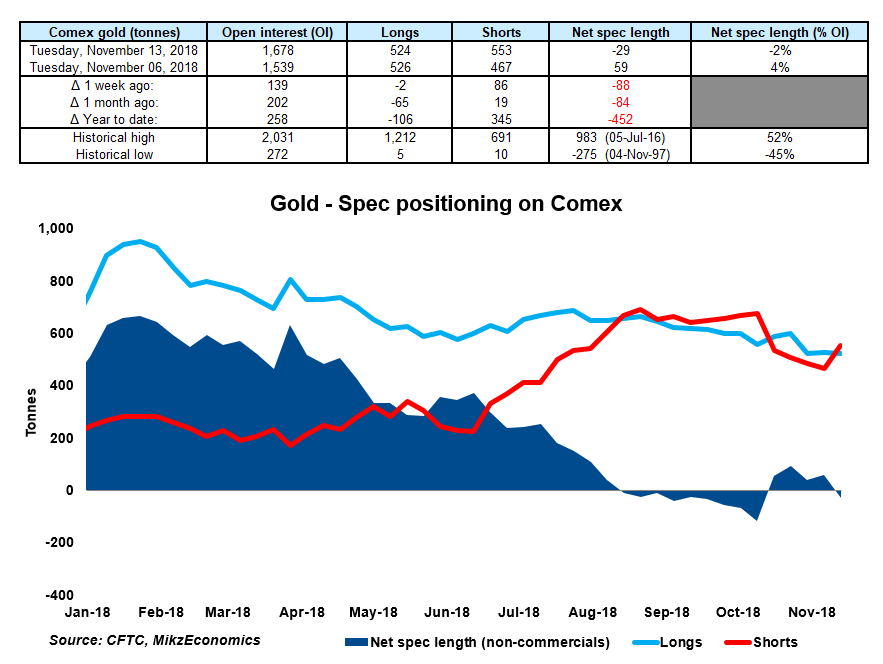

Source: CFTC

According to the latest Commitment of Traders report (COTR) provided by the CFTC, non-commercials turned net short Comex gold in the week to November 13, for the first time since early October.

The net spec length dropped by 88 tonnes, moving from +59 tonnes on November 6 to -29 tonnes on November 13. This was predominantly the result of fresh shorting (86 tonnes).

This was the largest weekly pace of net selling since the week to May 8, 2015 (-93 tonnes).

This year, the net spec length reached a low of -119 tonnes on October 9. The historical low was -275 tonnes, reached on November 4, 1997.

Clearly, speculative sentiment toward Comex gold has deteriorated substantially over the past week, which could suggest that the net spec length will revisit sooner rather than later its YTD low.

Nevertheless, this does not contradict my core view that the current spec positioning in Comex gold is excessively bearish and is due to normalize. Additional speculative selling will only make this unsustainable situation worse. However, it is hard to predict exactly when this normalization may take place. The macro backdrop, characterized by the dollar and US real rates, will play a key role.

Bottom line: Spec sentiment toward gold has deteriorated, judging by the substantial pace of fresh shorting over the past week. Still, I remain of the view that a normalization in gold's spec positioning is due to occur. Accordingly, a massive wave of speculative buying in favour of Comex gold is to be expected, resulting in considerable upward pressure on Comex spot gold prices, which in turn would lift the value of GraniteShares Gold Trust ETF.

Investment positioning

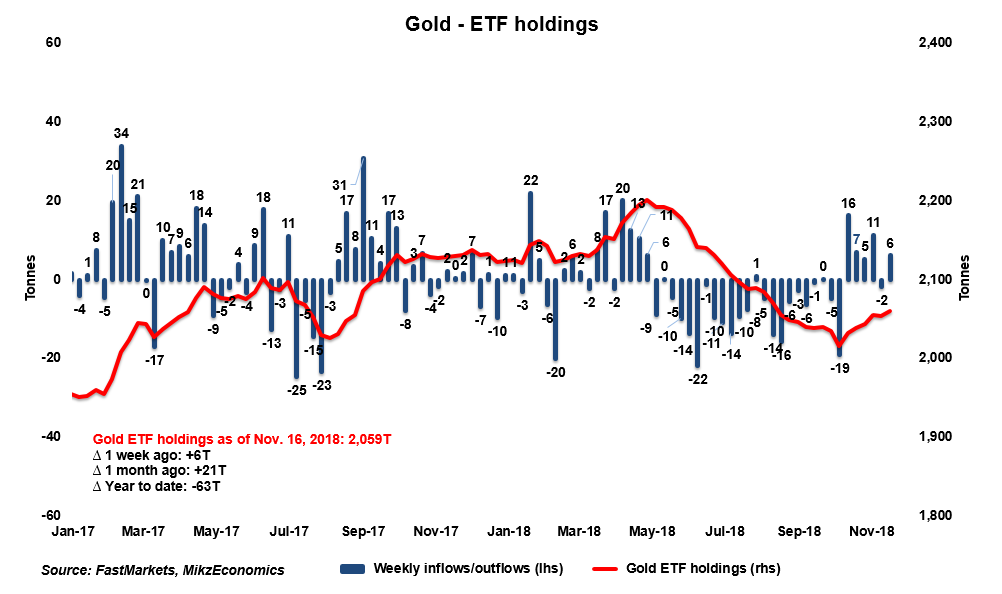

Source: FastMarkets

ETF investors resumed their gold buying in the week to November 16, according to FastMarkets.

Gold ETF holdings rose around 6 tonnes over November 9-16, marking a 5th time of inflows over the past 6 weeks.

ETF investors have bought around 21 tonnes of gold over the past month, mainly because the macro environment has resulted in a pick-up in demand for haven assets.

With the volatility in risk assets continuing its move higher, macro investors are likely to boost further their gold holdings to balance their portfolios.

While the resilience in the dollar has contained inflows into gold ETFs, the narrative could change after the Fed delivers its expected rate increase of 25 bps during its last meeting of the year. Indeed, the December rate hike is likely to mark the start of a pause in the tightening process due to clearer evidence that 1) investors are struggling to adapt in the face of a rising yield environment and 2) downside risks to the US economy are growing.

Against this, the dollar is likely to come under renewed downward pressure, which could boost gold ETF inflows and ergo, push Comex gold prices higher.

Bottom line: ETF inflows into gold have been undermined by the resiliency of the dollar. This could change after the December FOMC meeting when the Fed is due to deliver its final rate hike of the year. A renewed weakening of the dollar will lift gold ETF demand.

Trading positioning

To assert upside exposure to gold prices, I have a long position in the GraniteShares Gold Trust ETF.

Source: Seeking Alpha

The technical picture has improved recently, with BAR attempting to reconquer its 20 DMA and the momentum indicator flirting with the neutral level.

A daily close above the 20 DMA is necessary to make sure the 2018 low is behind us.

Although I continue to work under the hypothesis that the worst is over, the renewed wave of speculative selling challenges my prevailing view.

In any case, I see the room for downward pressure limited from here with a reward-to-risk ratio heavily skewed in favour of bulls over the long term.

Accordingly, I remain long BAR. For the sake of transparency, I will update my trading activity on my Twitter account.

BAR - GraniteShares - Review

BAR is directly impacted by the vagaries of gold spot prices because the Fund physically holds gold bars in a London vault and is custodied by ICBC Standard Bank. The investment objective of the Fund is to replicate the performance of the price of gold, less trust expenses (0.20%), according to BAR's prospectus.

The physically-backed methodology prevents investors from getting hurt by the contango structure of the gold market, contrary to ETFs using futures contracts.

Also, the structure of a grantor trust protects investors since trustees cannot lend the gold bars.

BAR provides exposure which is identical to established competitors like GLD and IAU, which are nevertheless much more costly to hold over a long period of time. Indeed, BAR offers an expense ratio of just 0.20% while GLD and IAU have an expense ratio of 0.25% and 0.50%, respectively.

As of November 16, BAR traded at a slight premium of $0.25 per share to its net asset value, vs. a discount of $0.13 per share a week ago. I expect any deviation from the net asset value to narrow on the back of arbitrage opportunities.

BAR's average spread (over the past 60 trading days) is 0.02%, which is lower than that of its competitor IAU, at 0.09%, or SPDR Gold MiniShares Trust (GLDM), at 0.08%.

As a result, BAR offers the lowest total cost of ownership (expense ratio + spread) among gold ETFs.

BAR's average daily volume (over the past 45 trading days) is ~$2 million, which is much lower than that of IAU, at ~$126 million.

As of November 16, 2018, BAR's assets under management totalled $303 million, with 2.5 million shares. BAR's gold holdings were at 7.8 tonnes. In contrast, IAU's assets under management amounted to $10.3 billion, with 983.5 million shares. IAU's gold holdings were at around 272 tonnes.

Final note

Dear friends, if you enjoy reading my research, thank you for showing your support by clicking the "Follow" orange button beside my name on the top of the page and sharing/liking this article. I look forward to reading your comments below.

![]()

ETFs: GLD, GDX, NUGT, GDXJ, JNUG, GGN, DUST, IAU, PHYS, JDST, SGOL, JJC, GOEX, UGLD, SGDM, UGL, DGP, GLL, ASA, GTU, GLDI, OUNZ, RING, DZZ, SGDJ, DGL, DGLD, TGLDX, DGZ, CPER, PSAU, GOAU, GDXX, GYEN, BAR, GEUR, GDXS, GLDW, GHS, CUPM, UBG, QGLDX, GHE, MELT, IAUF

Disclosure: I am/we are long BAR.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Follow Boris Mikanikrezai and get email alerts