Mining M&A jumps to 4-year high - expect more in 2018

The value of global mining and metals deals hit a four-year high in 2017, according to accountancy firm EY, boosted by a jump in money raised on stock exchanges to a six-year high.

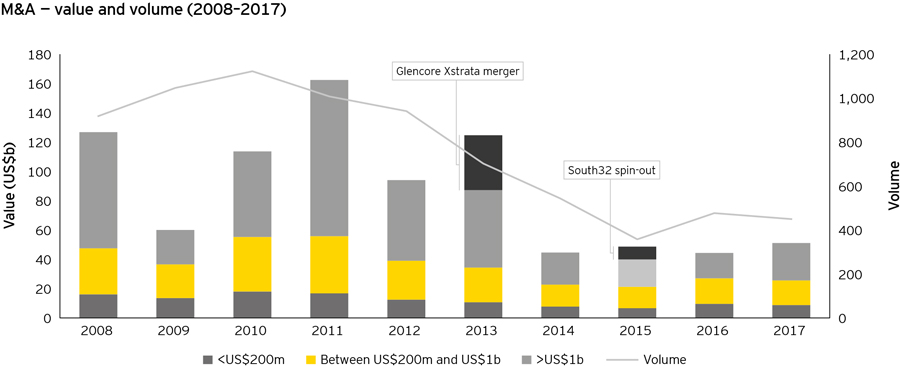

Mining and metals deals totalled $51 billion last year, up 15% from 2016. Activity was dominated by coal and steel transactions. However, the volume of deals fell 6% as M&A focus in the sector started shifting from divestment to strategic acquisitions.

"The focus for most of the sector in 2017 was consolidating balance sheet strength and maintaining capital discipline," EY said in a quarterly report on the sector, published on Monday.

Coal transactions surged 156 % to $8.5 billion as the world's move to renewables prompted miners to shift away from thermal coal.

With the buzz around new world critical minerals and battery technology, deals in lithium, copper and cobalt are expected to feature high on the agenda of management teams across the industryOne of the biggest coal deals last year was Rio Tinto's sale of its Coal and Allied mines to Australia's Yancoal for $2.7 billion.

Steel deals doubled to $13.3 billion, mainly comprising large Chinese mergers and divestments in Latin America. The report said overall China continued to be a key driver of activity, leading deals by value both as an acquirer ($18.7b, 36.5%) and as a target ($13.6b, 26.6%).

Gold transactions fell 34% to $7.3 billion as the volume of transactions fell 13% to 134 deals done. The number and value of deals in copper, nickel, potash all fell, while silver-lead-zinc and iron ore saw more activity.

Source: EY Mergers, acquisitions and capital raising in the mining and metals sector. Feb 2018.

Money raised by mining companies from IPOs and stock exchange listings rose to $2.8 billion, the highest in six years but still nowhere near the $17 billion raised in 2011 at the height of the commodities boom. Follow-on equity issues also rose to the highest since 2013 at $31 billion in 2017. Debt and loans together constituted $218 billion of the total money raised last year.

For 2018 EY expects deals to be fuelled by the industry's return to investment-led strategies aimed at building portfolios rather than the divestment-oriented deals that dominated in 2017. Companies' working capital requirements are also set to increase.

"Some of this activity will be to shape portfolios for future growth and sustain shareholder returns," said EY global mining and metals transactions leader Lee Downham, "but the return of transformational consolidation across the industry is unlikely as capital discipline is maintained":

Alongside this capital discipline, we began to see the emergence of investment strategies, with capital earmarked for organic projects and increasingly considered for acquisitions.

"With the buzz around new world critical minerals and battery technology, deals in lithium, copper and cobalt are expected to feature high on the agenda of management teams across the industry," according to the report.