Mining sector unloved as investors find it hard to trust

Investors are shunning the mining sector, data from Thomson Reuters shows, as they struggle to forget the string of multi-billion dollar takeovers and expensive development projects that left them empty handed.

A decade-long commodity boom coincided with years of economic growth when China took off, but when the global economy slowed, so did the market for commodities from oil to copper.

Data shows that two years after the worst of the raw materials slump is over, investors are still not ready to pour in fresh funds despite a price rally.

The mining sector led the FTSE higher in 2016 as it rebounded from the previous year's deep price crash, but it is still well below levels seen in 2011.

Thomson Reuters data shows mining funds shrank slightly last year after a surge in 2016.

Returns of 16 UK-domiciled natural resources funds fell 2 percent last year after a 74 percent increase in 2016. Assets under management fell to 3.78 billion pounds ($5.3 billion) last year from 3.81 billion in 2016.

"It seems that investment in mining companies has gone from sector-specific funds to generalist and more diversified funds. After the good bounce in 2016 people may have decided to take their money out of sector specific funds," Investec Asset Management portfolio manager Hanr?(C) Rossouw said.

Rossouw said there was a general lack of trust in mining management because of lingering concerns they "will just do the same as they've done in the previous supercycle in not returning cash to shareholders and making poor capital allocation decisions".

Mining more than other sectors is prone to boom and bust because of its exposure to commodity price movements and its need to spend large amounts of capital developing assets over long periods before they generate returns.

In boom years, miners have notoriously overpaid by billions to acquire assets in bidding wars.

A Bank of America-Merrill Lynch survey of fund managers published in February found European investors were more overweight on cyclical sectors such as autos, construction and oil and gas but were 24 percent underweight on basic resources, including mining.

Portfolio managers usually make investments underweight when they believe they will underperform compared to the other sectors in which they invest.

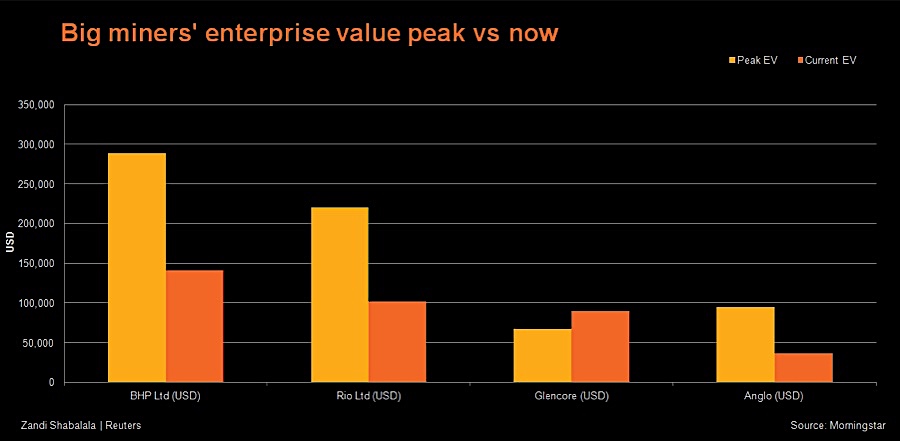

The market capitalisation and enterprise value of the big miners is far below the peaks of 2012 when M&A deals were done at unsustainably high prices.

The correction now reflects wariness that another boom will lead to bust, as well as concerns about sustainability as miners continue to see profits in carbon-intensive coal and operate in countries of high risk.

Jonathan Miller, head of UK manager research at Morningstar, said the miners had attracted attention in the early 2000s in line with interest in emerging market growth, but were now stuck in the "unloved camp" as investors bearing the memory of the financial markets crash avoided the most highly cyclical stocks.

"The sector has been in outflow mode for six out of the last seven years, with the only positive in this period being 1.1 billion euros ($1.4 billion) of net inflows in 2016," he said.

SHARE BUYBACKS

Miners, which will continue reporting results next week, have started to reward their long-suffering shareholders.

Rio Tinto has carried out buybacks and last week announced record dividends, while BHP Billiton has not carried out a buyback since 2011, but last August announced a record dividend.

Anglo American and Glencore, which scrapped dividends at the height of the crash, have reinstated them.

For the risk-averse there are warning signs the dividends may not endure.

As Glencore regained confidence last year, it embarked on a bidding war to buy coal assets and has its eye on expanding its agriculture assets.

Glencore and all the other big miners, however, promise they will not get carried away.

Rio Tinto's Chief Financial Officer Chris Lynch told Reuters the company was delivering "a great shareholder return story".

"I don't think you're going to find many people in my position who are going to say we are overvalued," he added. "We are delivering through the cycle." ($1 = 0.8015 euros) ($1 = 0.7127 pounds)

(Reporting by Barbara Lewis and Clara Denina; Additional reporting by Helen Reid and Zandi Shabalala; Editing by Susan Fenton)