RAB's Philip Richards: Why a gradual bull market in metals is on its way

After five trying years, RAB Capital Founder and President Philip Richards sees the light at the end of the tunnel. In this interview with The Gold Report, he argues that a continued zero-interest-rate policy from the Fed will be good for gold and silver, while continued quantitative easing will be good for base metals. Many fine mining companies now trade at deep discounts relative to their NPVs, and Richards suggests a half-dozen poised to take off once the new bull market finds its legs.

After five trying years, RAB Capital Founder and President Philip Richards sees the light at the end of the tunnel. In this interview with The Gold Report, he argues that a continued zero-interest-rate policy from the Fed will be good for gold and silver, while continued quantitative easing will be good for base metals. Many fine mining companies now trade at deep discounts relative to their NPVs, and Richards suggests a half-dozen poised to take off once the new bull market finds its legs.

The Gold Report: For five years experts have confidently yet incorrectly predicted higher interest rates and an end to the Federal Reserve's zero-interest-rate policy (ZIRP). Janet Yellen announced Oct. 28 that the Fed would not raise rates now, but might do so in December. Even so, some analysts believe the Fed might follow Europe into negative interest rate territory. What do you think?

Philip Richards: The U.S. economy has maintained a reasonable rate of growth. Globally, however, growth has been disappointing, with the emerging markets being particular stragglers. One reason for this is the tapering of quantitative easing (QE) that the Fed announced three years ago. The U.S. dollar has gotten stronger ever since. This has undermined commodity markets and also created something of a debt crisis in the emerging markets, a crisis that has not yet come home to roost. Many emerging market companies have debt in U.S. dollars, and their local currencies have crashed, so servicing those dollar debts has become rather difficult.

Despite this sluggish global growth, total global debt is now higher than it was in the 2008 crisis. Given the fragile state of the world economy, I believe the Fed simply cannot afford to raise rates. I don't believe that negative rates will be necessary; an announcement by the Fed that ZIRP will continue for the foreseeable future should suffice to retain market confidence.

TGR: There's a school of thought that holds that higher interest rates are impossible, not only because they would kill the recovery, but also because they would cause U.S. deficits to balloon due to skyrocketing interest rate payments on the debt. What's your opinion?

PR: The International Monetary Fund (IMF) has considerable influence on this question. I've been told that IMF Managing Director Christine Lagarde has asked the U.S. not to raise rates for fear this would trigger a global debt default crisis that would devastate Europe and then reverberate back to the U.S.

TGR: Should American economic growth remain nominal, is another round of QE possible?

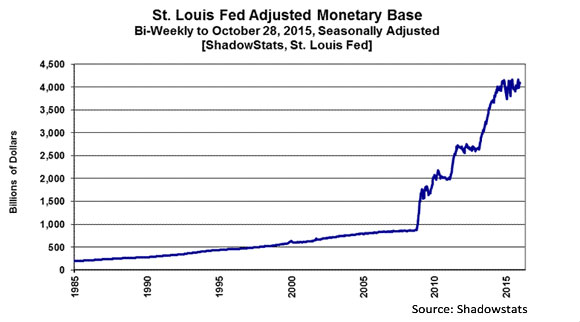

PR: Yes. Given the aggressive QE pursued by both Europe and Japan, the Fed could argue that U.S. QE worked in the past, and now that the dollar is too strong, it's time for the U.S. to jump back in. [Editor's note: See chart above.]

TGR: QE served initially as a catalyst for a big upswing in the price of gold. Subsequent rounds from the Fed and from Europe and Japan have not had the same effect. Why not?

PR: One reason could be the increase in primary gold production, up to 95 million ounces (95 Moz) in 2015. Another reason could be that China and India are not buying as much gold as they have in the recent past.

Technically, it looks to me as if gold has found a bit of a base. The continuation of ZIRP should allow gold to make progress.

TGR: What effect will the ongoing currency wars have on the prices of metals?

PR: The currency wars have essentially followed QE. The Fed began QE in 2008, which led to a weaker U.S. dollar and a stronger euro and yen. When the Fed began tapering, the dollar recovered, and the euro and yen got weaker.

Printing money should be good for precious metals. Greater economic activity is good for non-precious metals and all commodities really, but of course that's on the demand side. On the supply side, many big iron ore and copper projects have come on line since 2008 and driven prices down. In addition, the financial crisis in China has flushed out hidden stocks of metals, so it appears demand was probably weaker than supposed.

TGR: Some pundits predict that rising all-in sustaining costs (AISC) will mean a decline in gold production. Do you agree?

PR: I think 2015 will be a peak year for gold production, and, as you know, it takes a long time to ramp up production. As for AISC, this is hard to calculate when so much gold production is in countries outside the U.S.: Canada, Australia, Brazil, Africa. Kinross Gold Corp. (K:TSX; KGC:NYSE) has definitely benefitted by the strong U.S. dollar because it has mines in Russia.

TGR: What are your metals price forecasts?

PR: I expect gold and silver to be higher in a year's time. Zinc will be moving into supply deficit, due to the closure of MMG Ltd.'s (1208:HK) Century mine in Australia, the largest in the world; the closure of Glencore International Plc's (GLEN:LSE) Brunswick and Perseverance mines in Canada; and the possible shutdown of its McArthur mine in Australia.

But I don't know whether there will be a zinc squeeze sufficient to raise the price of zinc to its old high of $2 per pound ($2/lb). I expect a new high closer to $1.20-1.30/lb.

I'm cautiously optimistic on commodities. We could see higher copper and nickel prices in the next year or so. Regardless of whether the U.S. restarts QE, Europe will continue to print money, and that will be reasonably supportive of commodity prices.

TGR: Which companies are best placed to profit from a zinc deficit?

PR: Our favorite in this space is Trevali Mining Corp. (TV:TSX; TV:BVL; TREVF:OTCQX). On Oct. 8, the company announced record Q3/15 production at its Santander mine in Peru. And it is successfully commissioning a second mine in New Brunswick, which will surpass Santander as its leading producer. Trevali has got a pretty low cost base overall. We expect the shares can at least double from here.

TGR: Is a takeout of Trevali possible?

PR: That's not the reason we own the stock. That said, nobody wants to buy high-cost production after what we've been through, and Trevali has assets in the right place on the supply curve: the top quartile. On that basis, it is a potential takeover candidate.

TGR: Back in March, you told The Gold Report that HudBay Minerals Inc. (HBM:TSX; HBM:NYSE) was a possible suitor. Do you still believe that?

PR: I do, although the environment for metals was happier then than now. The appetite for acquisitions is somewhat diminished at the moment.

TGR: This unhappy environment has resulted in several companies sitting tight on their projects. Could you talk about one such gold project?

PR: We own Victoria Gold Corp. (VIT:TSX.V), which owns the 6.3 Moz gold Indicated and Inferred Eagle project in the Yukon. It is quite difficult to finance that project to production with gold around $1,100/ounce ($1,100/oz). So I believe that Victoria's strategy of waiting until the stars are in alignment has made sense. If, however, gold has bottomed out and is heading higher, Eagle will be much more likely to attract financing. Eagle has got reasonably robust economics but not in the top quartile.

We are one of Victoria's largest shareholders, and we do believe in Eagle. But the price of gold will need to reach $1,300-1,400/oz-as we believe it will-for Eagle to be financed on good terms.

TGR: You also hold a position in a similarly becalmed gold project just over the border in Alaska, correct?

PR: Yes, we do. Northern Dynasty Minerals Ltd.'s (NDM:TSX; NAK:NYSE.MKT) Pebble project. This is a world-class project with Measured, Indicated and Inferred resources of 81.5 billion pounds (81.5 Blb) copper, 107 Moz gold, 5.6 Blb molybdenum and 514 Moz silver. I believe that Pebble has turned the corner and will be developed. The company has amassed evidence of unfair treatment by the Environmental Protection Agency, and it should now begin to move forward on permitting.

TGR: What do you make of the business combination of Northern Dynasty with Mission Gold Ltd. (MGL:TSX.V)?

PR: It brings Northern Dynasty some money and some well-placed shareholders. Other investors are coming to the same conclusion about Pebble that we have made. Based on the size of its resource, this company should be worth 10 times what it is now.

TGR: Which gold producer do you like?

PR: Endeavour Mining Corp. (EDV:TSX; EVR:ASX) has mines in Burkina Faso, C??te d'Ivoire, Ghana and Mali producing 500 Koz annually. This is a company highly leveraged to an increase in the price of gold. In addition, it has some highly successful exploration results at Agbaou: 6.71 grams per ton (6.71 g/t) over 7.4 meters (7.4m), 7.73 g/t over 7.4m and 3.18 g/t over 6.8m. We believe that this exploration can rapidly be brought into resource and then into reserves. I would expect this company to move up significantly from here.

TGR: Endeavour has entered into an alliance with La Mancha, a private gold producer controlled by the family of billionaire Naguib Sawiris. How significant is this development?

PR: The takeover of La Mancha brings $63M of cash. The Ity mine, in which Endeavor will have 55% interest, will boost production from 2016, and by more than 100 Koz for Endeavor's share by 2019. The family has committed to be long-term shareholders. So this seems a very positive acquisition both by bringing more cash to the balance sheet and more gold production and growth.

TGR: You said in March that you were "very disappointed in nickel." Are you more bullish now?

PR: Not yet, but I am hopeful for a recovery in 2016. Nickel is another metal affected negatively by the financial crisis in China, which revealed previously unknown stocks that were flushed out, bringing the price down. I think the additional supply has been nearly exhausted, and we are seeing the beginning of the establishment of a technical base. This could bring the price back up to $6.50/lb or so in the next year.

TGR: How is the export ban from Indonesia playing out?

PR: It's still holding firm at the moment. The Philippines has stepped in and exported some nickel pig iron, but that production appears to have plateaued. Indonesia is not likely to become a major world supplier for another two to three years.

TGR: Which big nickel project would benefit most from a price rise?

PR: Well, we are the largest shareholder of Royal Nickel Corp. (RNX:TSX), so we have a vested interest there. Its Dumont project in Quebec would be the fifth-largest nickel sulfide operation in the world with a Proven and Probable reserve of 6.9 Blb, and the Royal Nickel has benefited from some provincial government support. The company is working hard to reduce the nickel price it needs to make Dumont viable. It received federal permitting in July.

At $6.50/lb nickel, Dumont is financeable. Royal shares are deeply oversold right now. Dumont's story is similar to Victoria's Eagle: a world-class project in a safe political jurisdiction. Situated in Quebec, Dumont benefits from cheap power and a provincial government that could assist with financing.

TGR: Can you give us updates on some of the companies we talked about last time?

PR: In the past we have talked about Largo Resources Ltd. (LGO:TSX.V); its shares haven't been performing well. However, I'm encouraged that it continues to ramp up production successfully at its Maracas vanadium mine in Brazil.

Also, Detour Gold Corp. (DGC:TSX) has just produced its first 1 Moz of gold at Detour Lake in Ontario, and NOVAGOLD (NG:TSX; NG:NYSE.MKT) has $130 million in cash to advance its Donlin gold project in Alaska. We quite like Detour and NOVAGOLD. We don't own Kinross, but I quite like that company as well.

TGR: We are now close to five years of a bear market in precious metals and mining stocks. Is there an end in sight?

PR: I'm fairly bullish across most metals. Gold should lead silver higher. What we're heading into might not feel like a bull market because prices will still not be very high, nor will mining companies be particularly profitable. Nevertheless, every bull market starts from the bottom of a bear market. The past five years have been painful for many, including us. In any event, I believe that a slow and steady buildup will be much better than something more dramatic.

TGR: During the previous bull market in precious metals, gold and silver miners performed poorly compared to the rise in the price of bullion. How well will the miners do this time around?

PR: The erosion of the traditional premium was brought about partly by the arrival of the gold ETFs, which obviated the need of investors to buy miners in order to leverage higher prices. As a result, mining companies have gone down and down and down. Investors can now buy good-quality companies at prices quite low relative to their net present values. Those are the ones that we would like to buy. There are quite a few names out there that can be bought pretty cheaply relative to the price of gold. That's a big turnaround. The short answer is that the overvaluation of gold companies relative to gold was destroyed over the last few years. This time around it will be different.

TGR: Philip, thank you for your time and your insights.

Philip Richards is the founder and president of RAB Capital Limited, having cofounded the company with Michael Alen-Buckley in 1999. He is the investment manager for the RAB Special Situations Fund. Prior to joining RAB, Richards was a managing director of European research and later managing director of investment banking at Merrill Lynch. Richards holds a Bachelor of Arts Honours from Oxford University (Corpus Christi College) in philosophy, politics and economics.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Interviews page.

Source: Kevin Michael Grace of The Gold Report

DISCLOSURE:1) Kevin Michael Grace conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Trevali Mining Corp., Victoria Gold Corp., Largo Resources Ltd. and NOVAGOLD. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.3) Philip Richards: I, my family and/or RAB Capital has ownership positions in Detour Gold Corp., Endeavour Mining Corp., Largo Resources Ltd., NOVAGOLD, Northern Dynasty Minerals Ltd., Royal Nickel Corp., Trevali Mining Corp. and Victoria Gold Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise - The Gold Report is Copyright (C) 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

Source: Kevin Michael Grace of The Gold Report