Rates Continue To Defy \

Authored by Lance Roberts via RealInvestmentAdvice.com,

The "Bond Bears" just can't seem to catch a break.

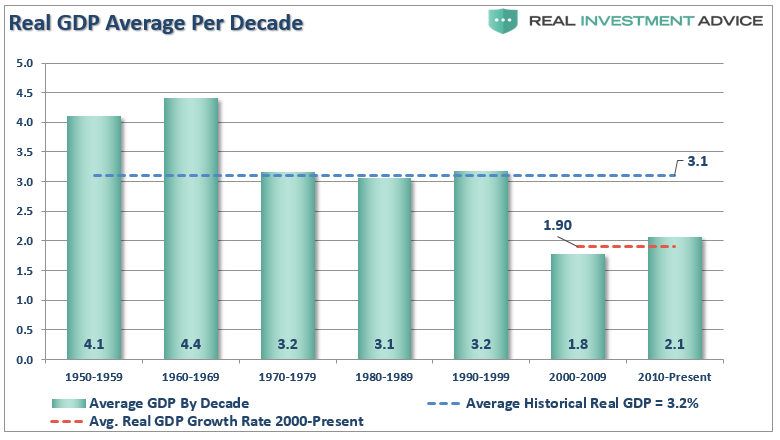

Beginning in mid-2013, there have been numerous calls the 30-year bond bull market was dead. The reasoning was simplistic enough - economic growth was set to return pushing inflation, and ultimately interest rates, higher. Unfortunately, as each year has come and gone, economic growth has failed to return with real economic growth averaging just 1.9% since the turn of the century.

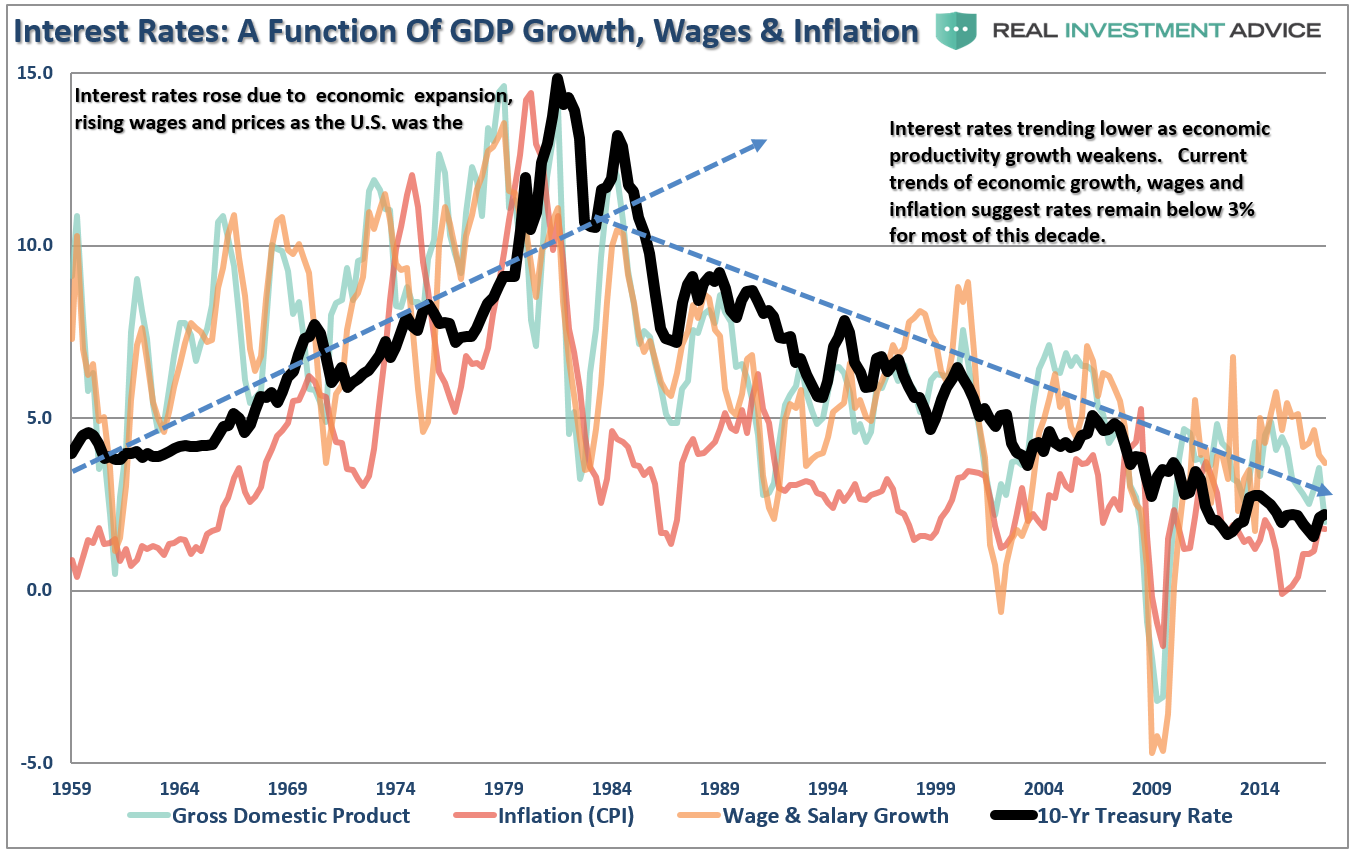

As I have discussed many times in the past, interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be clearly seen in the chart below.

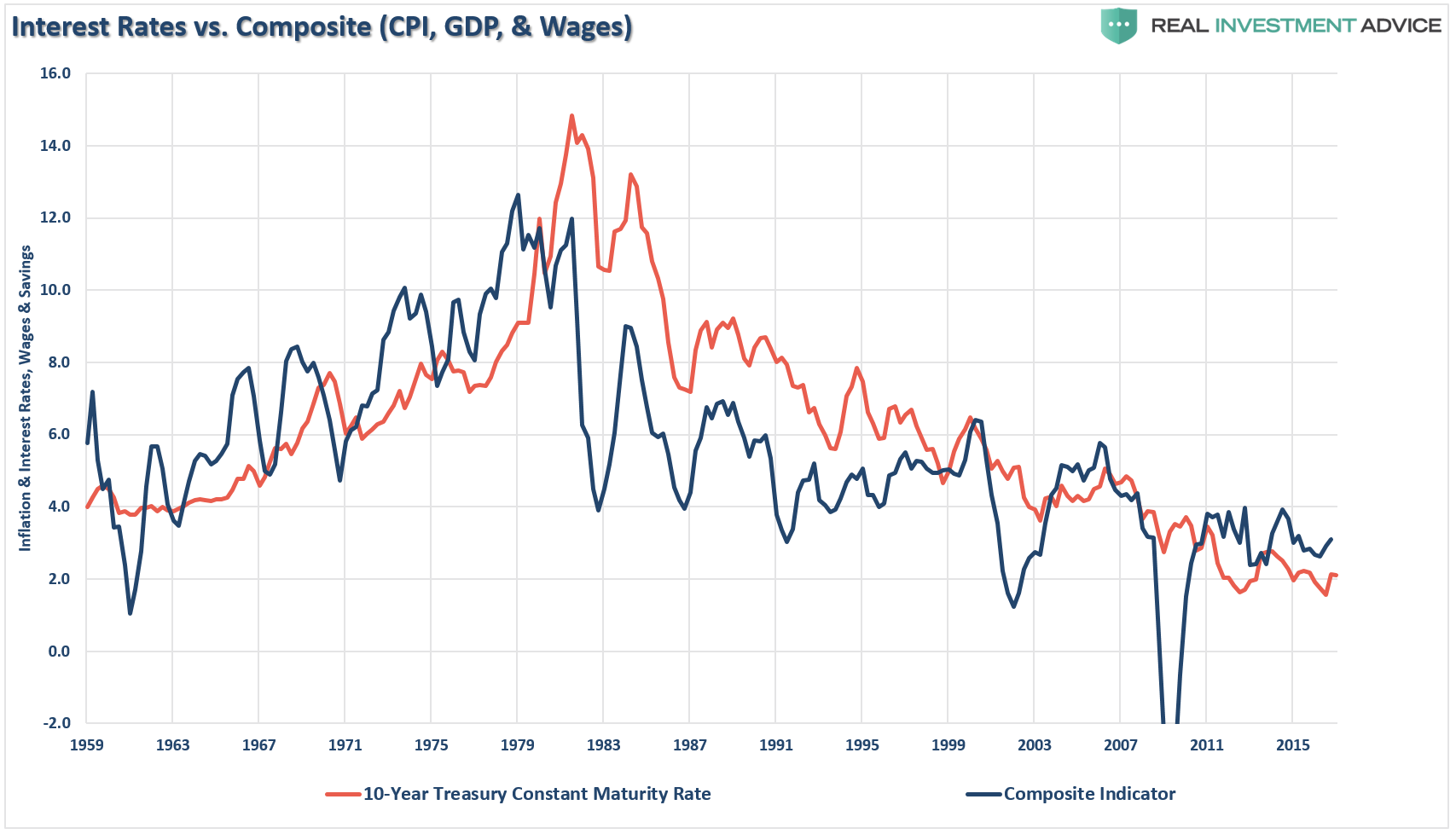

Okay...maybe not so clearly. Let me clean this up by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.

As you can see, the level of interest rates is directly tied to the strength of economic growth, wages and inflation. With roughly 70% of economic growth derived from consumption, the trend of wage growth should not be readily dismissed.

Ed Harrison at Credit Writedowns noted:

"What I can say is that the credit markets have been right all along the way. At important points in time when the Fed signaled policy changes, credit markets have correctly interpreted how likely those changes were going to be. The perfect example is the initial rate hike path set out in December 2015. This was totally wrong and the credit markets were telling us so, right from the start."

He is absolutely correct.

It was the analysis of the credit markets that has kept me on the right side of the interest rate argument in repeated posts since 2013.

However, Ed nails what Wall Street continues to deny in one sentence:

"What credit markets are saying right now screams secular stagnation."

Since 2009, asset prices have been lofted higher by artificially suppressed interest rates, ongoing liquidity injections, wage and employment suppression, productivity-enhanced operating margins, and continued share buybacks have expanded operating earnings well beyond revenue growth.

The Fed has mistakenly believed the artificially supported backdrop they created was actually the reality of a bright economic future. Unfortunately, the Fed and Wall Street still have not recognized the symptoms of the current liquidity trap where short-term interest rates remain near zero and fluctuations in the monetary base fail to translate into higher inflation.

Combine that with an aging demographic, which will further strain the financial system, increasing levels of indebtedness, and lack of fiscal policy, it is unlikely the Fed will be successful in sparking economic growth in excess of 2%. However, by mistakenly hiking interest rates and tightening monetary policy at a very late stage of the current economic cycle, they will likely be successful at creating the next bust in financial assets.

Furthermore, as Ed noted:

"And if this share price actually did indicate higher economic growth, not just higher profits, then US government bond yields would be rising due to future rate hike expectations as nominal GDP would be boosted by full employment and increased inflation. But that's not what's happening at all.

Instead, the US 10-year bond is pretty close to 2% and the yield curve is flattening. So, what I see the bond markets saying is that future rate hikes by the Fed will be limited due to low nominal GDP growth aka secular stagnation."

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds.

However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter.

Since interest rates affect "payments," increases in rates quickly have negative impacts on consumption, housing, and investment which ultimately deters economic growth.

Given the current demographic, debt, pension and valuation headwinds, the future rates of growth are going to be low over the next couple of decades - approaching ZERO.

While there is little left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Therefore, bond investors are going to have to adopt a "trading" strategy in portfolios as rates start to go flat-line over the next decade.

Of course, you don't have to look much further than Japan for a clear example of what I mean.

But, for now, Wall Street continues to ignore the giant "secular stagnation" sign staring them in the face.