Silver Investors See Palladium as the "Canary in the Coal Mine" / Commodities / Gold and Silver 2018

The precious metals sector has just one standoutperformer this year, and that is palladium. Lately the market for that metalhas gotten more than just hot. Developments there could have implications forthe LBMA and the rickety fractional reserve system of inventory underpinning allof the physical precious metals markets.

Craig Hemke of the TF Metals Report was MoneyMetals’ podcast guest this past Friday. He has been watching the developments inpalladium closely and gave an excellent summary of what's involved.

Craig Hemke of the TF Metals Report was MoneyMetals’ podcast guest this past Friday. He has been watching the developments inpalladium closely and gave an excellent summary of what's involved.

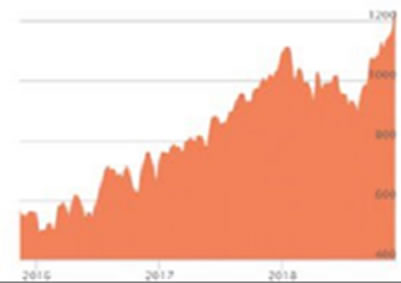

Palladiumprices went parabolic once before. The price went fromunder $400 per ounce to $1,100/oz from late 1999 to early 2001. Then, just asquickly, the price crashed back below $400.

Palladium's move higher in recent months isreminiscent. It remains to be seen whether or not a price collapse will follow.Some of the underlying drivers are the same, some are not.

Russia May Not Save the PalladiumMarketing This Time

Today, as in 2001, Russia is the world’s largest producer of the metal. Mines therecontribute about 40% of the world supply.

The shortage 17 years ago was driven by demand.Automobile and truck manufacturers began using more of the metal in catalyticconverters. It was a lower cost alternative to platinum.

When the market ran into shortage, Russians,under President Boris Yeltsin, rode to the rescue. They were willing and ableto bring more physical metal to market.

The added supply turned the market around justin the nick of time. The LBMA and bullion banks got away with selling way morepaper palladium than they could actually deliver.

Today, palladium inventory is once again inshort supply. This time around, however, the paper sellers in London and in theCOMEX may find themselves at the mercy of Vladimir Putin.

Russian relations aren't what they were in 2001.Palladium users may not get the same rescue as before, assuming Russian minershave stockpiles to deliver.

The bullion banks’ problem is starting to look serious.

For one thing, the lease rates for palladiumhave gone berserk. Bullion bankers and other short sellers often lease metal tohand over to counterparties standing for delivery on a contract. Until veryrecently, they could get that metal for less than one percent cost. Last week,that rate spiked to 22%.

That is extraordinarily expensive, and it reflectsthe scarcity of physical palladium. The only reason a banker might pay such arate is because he is over the barrel and has zero options outside ofdefaulting on his obligation.

Severe Shortages Lead to High LeaseRates, Backwardation

In conjunction with the surge in lease rates,the palladium market has moved into backwardation. It costs significantly moreto buy metal on contracts offering delivery in the near future than it does tobuy contracts with a longer maturation.

Normally the opposite is true when it comes tothe precious metals. Investors buying a contract normally pay a premium to havethe certainty of a fixed price today for metal to be delivered sometime welldown the road.

Investors are paying big premiums (about $100/ozcurrently) to get contacts with offering metal for delivery now. The near-termprice reflects a concern over whether promises to deliver palladium months fromnow can even be met.

Is the Palladium Situation a DressRehearsal for Gold & Silver?

Gold and silver bugs have long expected thebullion bankers will eventually put themselves in this kind of bind with themonetary metals. They have sold contracts representing something on the orderof 100 ounces for every ounce of actual gold or silver sitting in exchange vaults.

That much leverage is bound to end incatastrophe, someday. All it will take is a collapse in confidence – the suspicion that paper will not and cannot be convertible for actualmetal.

A failure to deliver in the relatively tinypalladium market could be the “canary in the coal mine” – a warning to investors in other precious metals. If there is a failureto deliver in LBMA palladium, it could shake confidence in the much largermarkets for gold and silver.

The developing shortage in the silver marketsuggests that silver could be the next situation, followed by gold.

By Clint Siegner

Clint Siegner is a Director at MoneyMetals Exchange,perhaps the nation's fastest-growing dealer of low-premium precious metalscoins, rounds, and bars. Siegner, a graduate of Linfield College in Oregon,puts his experience in business management along with his passion for personalliberty, limited government, and honest money into the development of MoneyMetals' brand and reach. This includes writing extensively on the bullionmarkets and their intersection with policy and world affairs.

© 2018 Clint Siegner - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2018 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.