Tocqueville's John Hathaway: Stick to your guns-hold on to those mining shares

Do you have wealth insurance? Tocqueville Gold Fund Portfolio Manager John Hathaway has studied the past and he sees a bright future for those who have taken the precaution of protecting themselves from the downside of a general bear market by buying resource mining stocks when they are at historic low prices. In this interview with The Gold Report, Hathaway shares the names the fund is holding as ammunition for a better gold market.

Do you have wealth insurance? Tocqueville Gold Fund Portfolio Manager John Hathaway has studied the past and he sees a bright future for those who have taken the precaution of protecting themselves from the downside of a general bear market by buying resource mining stocks when they are at historic low prices. In this interview with The Gold Report, Hathaway shares the names the fund is holding as ammunition for a better gold market.

The Gold Report: John, you have studied the fundamentals of gold through history. What is behind the current market prices, and what will it take to move prices higher again?

John Hathaway: Adversity in the financial markets is the trigger that will force the general investment world to become interested in gold again. That is a nice way of saying it will take a bear market to push investors to gold. Monetary policy has forced investors into riskier assets-including junk bonds and overvalued NASDAQ stocks. When the tables turn and people start experiencing losses, there will be finger pointing, starting with the Federal Reserve's nominal interest rates. That whole spectacle could balloon and cause conventional investors to throw up their hands and run for liquidity.

TGR: We've talked to some people, including Brien Lundin, who think that a Federal Reserve interest rate increase will be good for gold because it will remove the question mark that's been overhanging the gold price since it is pretty much already priced in. Do you agree?

JH: I agree that it has been baked in for years, but I think the bigger story is going to be loss of confidence in the Fed and a general downturn in financial markets, which is long overdue. That is when investors will look at safe places to go. Gold has always acted as wealth insurance. Whenever we have had extreme financial events throughout history, gold has always been the last man standing. Gold's purchasing power lasted through the crisis in 2008 and every crisis before that. It's impeccably liquid. You can buy or sell it on a very thin bid/asked spread 24 hours a day. There's almost no other market you can say that about.

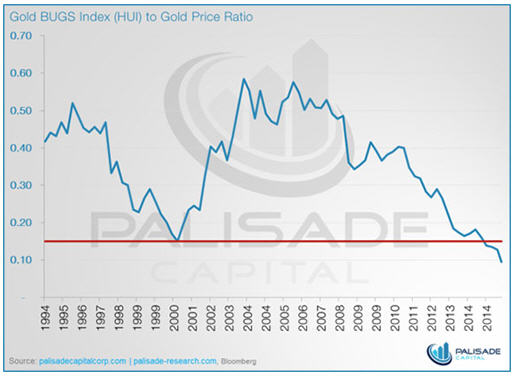

TGR: Why did you recently compare today's gold market to the London Gold Pool of the 1960s when eight central banks worked together to try to maintain a gold price of $35 per ounce before the scheme collapsed?

JH: It has been in the interest of public policy and the financial establishment to operate in an environment of zero or nearly zero interest rates, interbank lending rates and LIBOR. That is not unlike the manipulation that occurred in the 1960s. Gold rocketing to new highs would upset that whole scenario designed to force capital out on the risk spectrum.

An indication of this artificial market is the fact that the synthetic market for gold-the COMEX, options, over-the-counter and LBMA-is traded hundreds of times more than the actual metal. Investors actually short gold by posting margin on the COMEX. That eventually drives the price of gold down without any physical gold changing hands. It manipulates the psychological market environment and then the high-frequency and algorithmic traders push the price smashing to the extreme and it all happens with no gold actually being sold.

TGR: What's the role of China in this retro-market scenario?

JH: It is playing a cat-and-mouse game. A huge amount of gold is heading from Western financial centers to the East as demonstrated by the withdrawals from the Shanghai Gold Exchange on top of the usual strong flows into India and Turkey. Physical gold's shift to China is a big part of this story as Asians buy on weakness.

However, the synthetic instruments-call options, short interest on COMEX and over-the-counter deals-could be the precursor to a scramble to get physical. That would be enhanced by a loss of confidence in counterparties by a bear market in stocks. You have already seen sovereigns' call for physical gold to be repaid. Germany was the highest profile, but many other countries have asked for earmarked gold in London and New York to be repatriated. That's a sign of a loss of confidence. That could affect the price in a very big way. And the Chinese will have it.

TGR: I'm looking at your portfolio and you have quite a few royalties. What is the benefit of holding royalties in the market scenario you have described?

JH: It's a good business model. It's a way to get participation in many more mines through one equity than you could get owning a large-cap company, such as Newmont Mining Corp. (NEM:NYSE) or Barrick Gold Corp. (ABX:TSX; ABX:NYSE). That's because the royalty business model makes investments in numerous different mines. It's basically a financing tool for companies that need to get capital to complete a project. Because we have been through such a nuclear winter for financing large and small companies, the royalties have very powerful deal flow, and they're able to set very attractive terms. Investors have gone through a difficult period in the gold equities market, but it has been advantageous for the royalty companies. That's why we have such a strong representation in those names.

TGR: What are some of the ones you like the best?

JH: There are only four of them that are of any consequence. The three big names are Franco-Nevada Corp. (FNV:TSX; FNV:NYSE), Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX) and Silver Wheaton Corp. (SLW:TSX; SLW:NYSE). Osisko Gold Royalties Ltd. (OR:TSX) has done some very interesting transactions lately. I think it's a real player. They're all run by smart people. They have a very lean business model. They're like the merchant bankers of the precious metals sector.

TGR: You seem to be largely in the mid-cap and small-cap mining companies. How do you manage the risk with the possible upside leverage?

JH: With the mid and smaller caps, there's more value creation for mine building and discovery of new reserves. It moves the needle more than you could get in a large-cap company. Those are very identifiable events. That is where our research can really pay off, more so than with big-cap companies where you have so many more moving parts and significant developments are often obscured in the mix of assets around the world. More important, with the larger-cap companies, a discovery isn't going to change the outlook. It's just what they have to do to sustain the model. But with the mid- and small-cap companies, a big discovery is value creating. When it gets recognized, I think you get much more of a return than you would in a large-cap name.

TGR: Let's look at some in your portfolio. You hold NOVAGOLD (NG:TSX; NG:NYSE.MKT), which has announced it will be releasing a draft environmental impact statement (EIS) on the Donlin Gold project in Alaska by the end of the year. Is permitting going to be a major milestone or are there other catalysts you're watching?

JH: Permitting is taking place. It's definitely a sign of progress. It is not a market-moving kind of event, but it's necessary. I look at NOVAGOLD as an option on the gold price. We know it has the ability to produce half a million ounces a year. That's enormous. If you went to UBS or Morgan Stanley and tried to get a 10-year call on gold prices, first of all, they'd laugh at you, but if they did actually give you a quote, it would be very expensive. If you compare that to what you get with NOVAGOLD, it's a perpetual call on the gold price with what could be a world-class gold mining asset, but it won't get built until the gold price is right.

TGR: Another company that you've had in the portfolio for a while is Torex Gold Resources Inc. (TXG:TSX). It just released its NI 43-101 on the Minera Media Luna project in Mexico, and the market seemed to react quite positively. Were you pleased with the new Inferred resource estimate?

JH: Yes, we're pleased but not surprised because this is a great asset. There's a lot of discovery that still could be made there. We're getting very close to launch for this company. It should be producing gold by the end of this year and may declare commercial production soon thereafter. That is a value-liberating sequence of events.

TGR: Are you worried about security risk?

JH: The market is. I think it's a risk you have with Torex, but that's generally the case anywhere in the gold mining world. Some companies have more of a problem than others. But this is going to be a huge tax generator for Mexico, so the government has an interest in seeing this move ahead securely. If the company hasn't already worked something out with the feds, it will. It's what mining companies have to do. They're challenged in a lot of ways, and one of the challenges is security. The better companies deal with it successfully. Other companies don't do it as well.

TGR: You've also held MAG Silver Corp. (MAG:TSX; MVG:NYSE) for a while. Where is the most immediate upside for that basket of projects?

JH: MAG Silver has a tremendous suite of silver-rich assets in Mexico, one of which is a joint venture with Fresnillo Plc (FRES:LSE), the world's largest silver producer. It's hard to imagine that at some point Fresnillo doesn't want to take over MAG for that asset. However, MAG's strong shareholder base, including Tocqueville, won't let that happen at too low a price. The dice are loaded for a deal and for a big move in the silver price, which could come on the heels of a big move in the gold price. I think MAG is one of the best pure silver stories out there.

TGR: Any other companies you want to mention?

JH: We have noticed that as the larger, over-indebted companies have had to sell assets to reduce balance sheet risk and lower debt, opportunistic buyers are stepping forward. B2Gold Corp. (BTG:NYSE; BTO:TSX; B2G:NSX), Premier Gold Mines Ltd. (PG:TSX) and the Australian company Evolution Mining Ltd. (EVN:ASX) are three examples of companies taking advantage of the distress among some of the larger-cap companies and buying quality assets at very attractive prices.

TGR: Any other parting words of wisdom for veteran investors trying to retain their wealth as they prepare for 2016?

JH: I think we are nearing the end of the pain. Stick to your guns if you own gold mining stocks, certainly if you own physical gold or if you own the Tocqueville Gold Fund, and think about adding more. I think the financial markets are turning. We may be at the dawn of a recognition that Fed policy and central bank policy worldwide is hollow, ineffectual and maybe worse. It could lead us into greater problems than we saw in 2008. So be prepared.

TGR: Thank you for the advice.

John Hathaway, senior portfolio manager of Tocqueville Asset Management (toqueville.com), manages all gold equity products and strategies at Tocqueville Asset Management. He holds a bachelor's degree from Harvard University, a Master of Business Administration from the University of Virginia and is a chartered financial analyst. He began his career in 1970 as an equity analyst with Spencer Trask & Co. In 1976, he joined investment advisory firm David J. Greene & Co., where he became a partner. In 1986, he founded Hudson Capital Advisors and in 1988, he became chief investment officer of Oak Hall Advisors.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.2) The following companies mentioned in the interview are sponsors of Streetwise Reports: MAG Silver Corp., Silver Wheaton Corp. and NOVAGOLD. Franco-Nevada Corp. is not affiliated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.3) John Hathaway: I own, or my family owns, shares of the following companies mentioned in this interview: Only as part of Tocqueville Funds. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. Tocqueville Funds own all of the companies mentioned. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise - The Gold Report is Copyright (C) 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

Source: JT Long of The Gold Report (10/26/15)