Weak metal prices to hit miners through 2016 - Moody's

Slowing growth in China and Brazil, muted conditions in Europe and a weak recovery in the US will continue to pressure global base metal prices, says Moody's.

Prices for iron ore, copper, nickel, aluminum and other metals have been in a multiyear slump amid sluggish growth in advanced economies and weakening expansion in emerging markets.

Unfortunately, the trend won't be fading anytime soon, Moody's Investor Service says in its latest global base metals outlook report, published Monday.

"Slowing growth in China and Brazil, muted conditions in Europe and a weak recovery in the US will continue to pressure global base metal prices," the ratings agency warns.

Moody's expects the current situation to get worse next year, and says that uncertainty regarding growth in China is one of the primary factors underpinning its negative outlook. This, as the Asian giant still accounts for more than 40% of global demand for most key base metals.

Moody's also noted that steeper price declines will flow through to companies' earnings in 2015, resulting in a material decline in cash flow for many producers.

"Base metal prices won't materially change over the next 12 to 18 months in our view, and could face further downside risk.

"Prices [will] continue to trade at lower levels, given expectations for reduced demand and slower growth rates," it added.

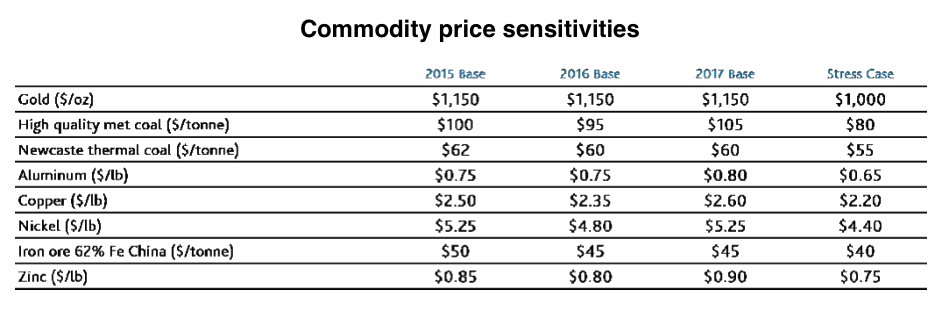

Moody's applies two pricing cases to help inform a forward view of potential credit metrics for the purpose of ratings consistency in the commodity sector. The base price is used to gauge near to mid-term operating performance, while the stress-case price is used to assess the company's financial and liquidity position in a more-stressed pricing environment. These are price assumptions and we do not rate to any single price, as we recognize the inherent volatility of the commodity markets. (Source: Moody's Investors Service)

And while the gloomy scenario may be a boon for economies that import metals, nations that rely heavily on such exports, such as Chile, DRC, Niger and Liberia, will likely have a rough ride ahead.

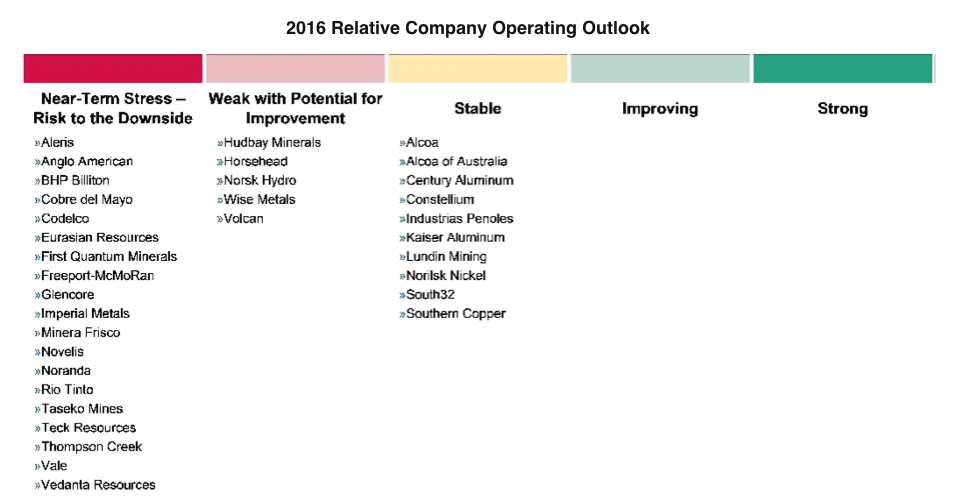

In terms on which companies are likely to downsize even further next year, Moody's says that well-capitalized, diversified producers with low cash costs, good liquidity and manageable debt-maturity profiles, such as Rio Tinto (LON:RIO) and BHP Billiton (ASX:BHP), will have a greater ability to negotiate a period of weakness. However, it adds that even they will not be immune to a protracted period of low prices.

Other diversified producers, like Vale (NYSE:VALE), Anglo American (LON:ANGLO) and Teck Resources (TSX:TCK.A, TCK.B), (NYSE: TCK), which have exposure beyond base metals to commodities such as metallurgical coal and iron ore, or ongoing, significant, strategic capital expenditures, also face further downward pressure.

Currently 35% of investment-grade companies in the global base-metals space have negative outlooks, compared with 54% of high-yield companies. For our perspective on the commodity sector and company positioning. (Source: Moody's Investors Service)

The firm said it may change its outlook for the industry if the purchasing managers' indexes (PMIs) in the large economies which are also huge consuming nations is consistently up.

"We could change our outlook for the industry to stable if purchasing managers' indexes (PMIs) in Europe, China and the U.S., the key consuming regions, track between 50 and 55 (above 50 indicates growth) for at least two consecutive months, and if Moody's global macro outlook is for GDP growth of between 3% and 4%.

A positive outlook would require PMIs in the US, Europe and China exceeding 55 for at least three consecutive months, and for Moody's global macro outlook for GDP growth to be greater than 4%," Moody's concludes.