Why cobalt (not lithium) could be the battery boom's big winner

Figure 1: Pure (99.9 %) cobalt chips, electrolytically refined. Source: Wikipedia image commons

By Sam Broom

You've probably given little thought to a perennially overlooked metal called cobalt, even though chances are you're reading this very article on a device powered by a battery containing a significant proportion of the metal.

I'm going to spend most of this article outlining an emerging narrative that argues that we could be in the early stages of a significant revaluation in the cobalt space. But before I do, I want you to cast your mind back a couple of years to a time before the recent speculative mania that overtook a previously obscure commodity called lithium.

The Lithium Boom - A Case Study For What Could Be Ahead For Cobalt

Before joining Sprott, I worked as an engineering geologist in Australia, and back in 2014 I was involved on a project for a struggling hard rock lithium miner. Among a host of issues, the mine was struggling with low prices of the resources with which it produced, primarily lithium. Even though the "battery revolution" was well underway and other battery related commodities, namely graphite, had been booming, lithium prices remained stubbornly low.

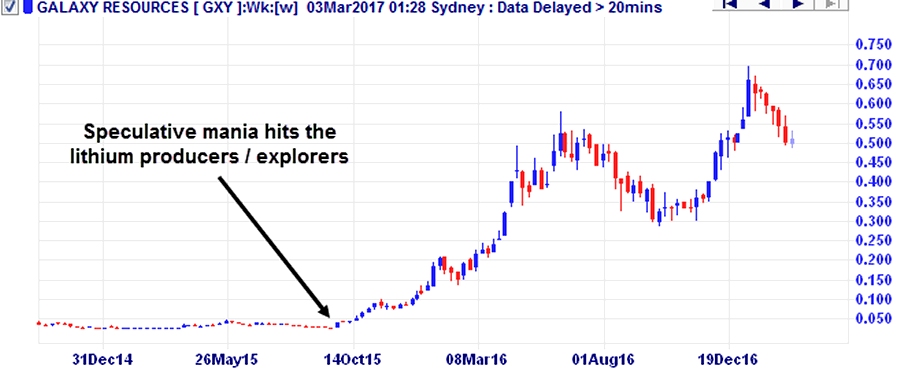

That all changed toward the end of 2015 as fears about a looming supply shortage caused the price of lithium to embark on the rather dramatic rise that we've seen over the past 18 months. To cut a long story short, the result has been a significant re-rate across the industry as the bulk of lithium exposed miners and explorers experienced sometimes staggering share price appreciations - the chart below showing the greater than 2,000% rise of ASX listed lithium miner Galaxy Resources being one of the more spectacular examples.

Figure 2: Stock chart of Galaxy Resources, a lithium producer listed on the ASX. The company's share price has risen over 2,000% since the end of 2015. Source - Incredible Charts

The move in lithium prices has largely been driven by "new age" companies such as Tesla and its aggressive CEO, Elon Musk, cultivating a growing, mainstream belief in the narrative that electrification and thus batteries are going to act as the "new oil" in powering our cars, devices, homes and businesses. Even legendary natural resource investors such as Robert Friedland have been getting in on scene, taking strategic positions in the sector.

This has led many analysts to call for compounding annual growth rates for the Li-ion battery industry of between 10% and 12%1 over the next 5 to 10 years which, if realized, would see the market grow from US$30 billion to over US$70 billion by 20241. The biggest growth is expected to be in the automotive and grid/renewable energy storage subsectors3.

Lithium, being a key raw material in the manufacture of the current crop of battery technologies (typically lithium-ion), has been the main benefactor, thus far.

The Demand Side Of The Cobalt Equation - The Battery Revolution

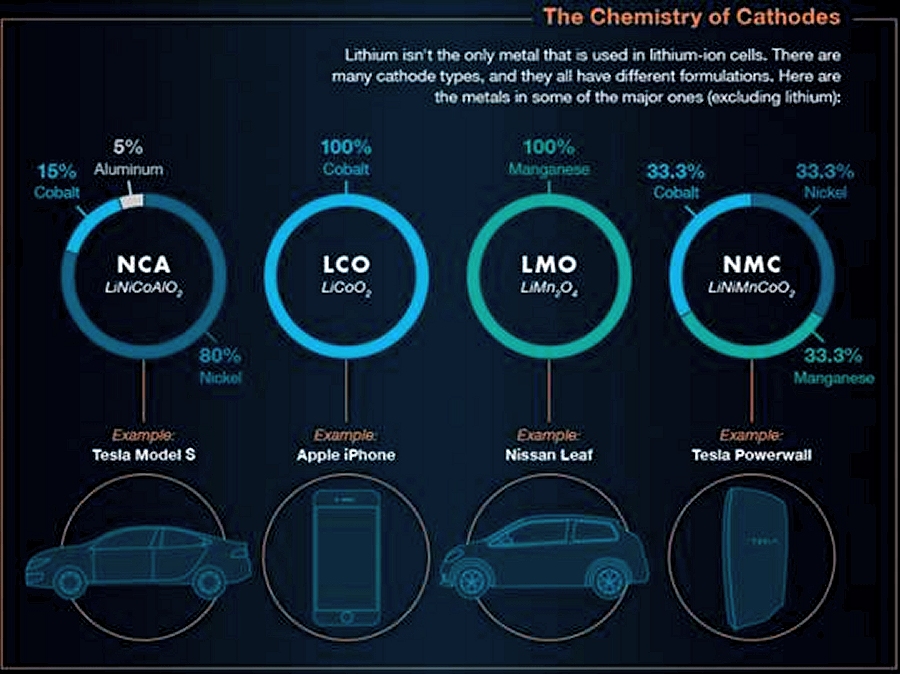

However, taking a deeper dive into what raw materials actually go into Li-ion batteries shows that lithium typically makes up a much smaller percentage of the overall raw material inputs than people think (as low as 2% by weight in some batteries, according to Elon Musk in this recent interview). In comparison, cobalt is used in significant quantities in the cathode component of batteries, which make up approximately 35% to 40% of the total material costs of a lithium ion battery cell2.

Depending on the type of battery, cobalt can comprise between 0% to 100% of the non-lithium material that goes into a cathode, something explained visually in this infographic. The pertinent figure from the infographic is presented below - note the significant percentage of nickel and cobalt in three of four main lithium ion cell types.

Figure 3: Typical non-lithium material inputs required in the construction of the cathode of various modern battery technologies. Source: VisualCapitalist.com

Figure 3: Typical non-lithium material inputs required in the construction of the cathode of various modern battery technologies. Source: VisualCapitalist.com

Given the amount of nickel in electric batteries, it's worth asking the question, "should we be looking at nickel too?" There's certainly a bullish case to be made for nickel as well (an article for another day), but the primary reason to be more interested in cobalt over nickel from a speculative investment viewpoint has everything to do with where the vast majority of cobalt production comes from.

The Supply Side - The Potential DRC "Black Swan"

Staggeringly, over 60% of global cobalt production comes out of a single country, the Democratic Republic of Congo (DRC) where it occurs as a byproduct in the huge copper deposits that the country is endowed with. This is hugely important because whilst the DRC has been relatively stable for the past 10 to 15 years, in the medium to long term the country has been the antithesis of stability and has a long and checkered history tarnished by internal conflict and civil wars.

So when the current president, Joseph Kabila, failed to step down after his two terms as president late last year (and even tried to amend the country's constitution to allow him a third term in office), all eyes have been on the country in anticipation of escalating tensions and a potential return to violence.

Congo's President Is Refusing to Step Down, Raising Fears of Bloodshed

There was an initial wave of minor unrest which hinted at the discontent that simmers below the surface, and Kabila's current approval rating has fallen in a catastrophic fashion to just 7.8%4 as of the end of 2016.

Discontent has somewhat abated following promises that the current administration will take the required measures to step down and hold democratic elections by the end of 2017. However, recent history suggests that one should be extremely skeptical regarding any promises made by Kabila.

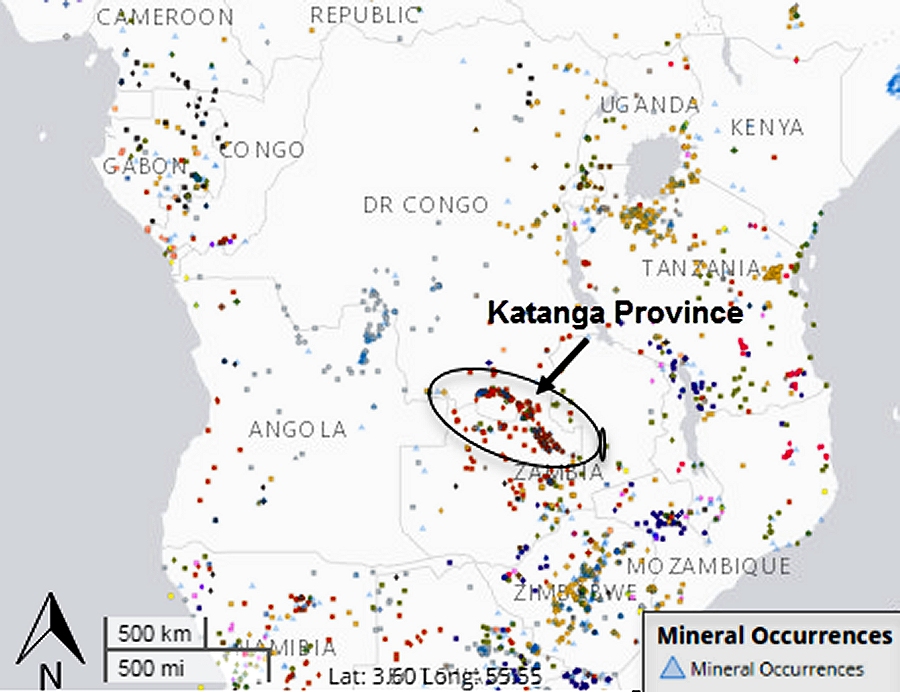

So why does this matter for cobalt? The vast majority of the DRC's cobalt resources occur in the very south of the country in the Katanga province, which happens to be the country's richest. That's largely because Katanga plays host to an extraordinary level of mineral resources - it's estimated to contain an incredible 5% of the world's copper resources and nearly half its cobalt. It's therefore a pretty safe bet to assume that whoever ends up in power in the DRC is going to want to retain control over Katanga.

Figure 4: Map of the DRC, showing the location of both the Katanga province and it's mineral abundance. Source: SNL Metals & Mining, an offering of S&P Global Market Intelligence.

Furthermore, a man named Moise Katumbi has emerged as Kabila's strongest opponent and happens to be the former governor of the Katanga Province. He is deeply popular in both Katanga and broadly throughout the country (he's currently the country's most popular politician). So not only do we have almost the entire supply of cobalt concentrated in a single, highly sought-after region of the country, but this region also looks set to play a central role in any resistance effort that's likely to mobilize should Kabila attempt to stay in power.

When any country (let alone one that's inherently unstable) controls over 60% of global supply of a commodity that's forecast to experience rapid near term demand growth, you better watch developments in that country very closely. Given we know that there are near term geopolitical storm clouds on the horizon that have a strong possibility of causing a material disruption to operations in the country's prime cobalt producing region, there's a cocktail for a serious cobalt supply squeeze brewing.

How to Invest To Gain Exposure To Cobalt

Given the current backdrop of expected strong demand growth coupled with a real possibility of significant, near term supply destruction, the risk to reward in the cobalt space looks enticing for investors with a speculative risk tolerance. This leads us to the question, "how does one gain exposure to cobalt?"

Unfortunately for investors, pure-play cobalt investment options are rare - there's no diversified "cobalt miners ETF", nor are there any large cap mining companies that are highly leveraged to the metal (remembering cobalt is typically a minor byproduct of copper and, to a lesser degree, nickel production). This means investors have to look further down the food chain, that is to the junior exploration and optionality companies.

Even within the junior space, both the quantity and quality of cobalt exposed companies is limited, however there are a few standout names if you know what to look for, but you've got to be selective. It's thus extremely important to speak with a qualified investment professional before jumping into the sector.

Lastly, most of these companies are located outside the U.S (typically in Canada and Australia) and trade on foreign exchanges, thus investors will need access to a broker with trading capabilities in these foreign markets.

In Summary

To sum things up, there are two main forces that may provide positive tailwinds to the cobalt space:

First, the growth of the Li-ion battery industry, which has already contributed to booms in both the graphite and lithium space, is likely to result in growing demand for cobalt given it's a key material input in most Li-Ion battery cells. Cobalt prices have already started rising, but are still a long way from their pre-financial crisis highs that were seen without the current fundamental drivers we see in the cobalt market.

Second, there is a serious geopolitical situation brewing in the DRC, the country responsible for over 60% of annual global primary cobalt production. If those developments turn sour and the current president Joseph Kabila once again fails to step down at the end of 2017, then there is the real possibility of an outbreak of unrest in the country. That could lead to significant disruption to cobalt output from the country, the likely result of which would be a serious global cobalt supply squeeze.

There are very few (if any) larger capitalization mining companies that have significant leverage to the cobalt price, therefore the main way to gain exposure to the sector is by investing in smaller capitalization junior exploration and development companies. Given the risk involved at that end of the market, picking the right companies is paramount.

If you are interested in investing in the cobalt space or have questions about the topics raised in this article, please contact the article author here or call your Sprott Global investment advisor at 800-477-7853.

1 Transparency Market Research (2016)

2 Roland Berger (2012) - PDF download

3 Statista.com (2016) - subscription required

Sprott U.S. Media, Inc. is a wholly owned subsidiary of Sprott Inc., which is a public company listed on the Toronto Stock Exchange and operates through its wholly-owned direct and indirect subsidiaries: Sprott Asset Management LP, an adviser registered with the Ontario Securities Commission; Sprott Private Wealth LP, an investment dealer and member of the Investment Industry Regulatory Organization of Canada; Sprott Global Resource Investments Ltd., a US full service broker-dealer and member FINRA/SIPC; Sprott Asset Management USA Inc., an SEC Registered Investment Advisor; and Resource Capital Investment Corp., also an SEC Registered Investment Advisor. We refer to the above entities collectively as "Sprott".

The information contained herein does not constitute an offer or solicitation by anyone in any jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation.

Forward-Looking Statement

This report contains forward-looking statements which reflect the current expectations of management regarding future growth, results of operations, performance and business prospects and opportunities. Wherever possible, words such as "may", "would", "could", "will", "anticipate", "believe", "plan", "expect", "intend", "estimate", and similar expressions have been used to identify these forward-looking statements. These statements reflect management's current beliefs with respect to future events and are based on information currently available to management. Forward-looking statements involve significant known and unknown risks, uncertainties and assumptions. Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking statements prove incorrect, actual results, performance or achievements could vary materially from those expressed or implied by the forward-looking statements contained in this document. These factors should be considered carefully and undue reliance should not be placed on these forward-looking statements. Although the forward-looking statements contained in this document are based upon what management currently believes to be reasonable assumptions, there is no assurance that actual results, performance or achievements will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this presentation and Sprott does not assume any obligation to update or revise.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any fund or account managed by Sprott. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any fund or account managed by Sprott will be invested.